"Credits are like seeds. If planted wisely, they bear fruit in abundance. If sowed recklessly, they result in weeds of debt." - Unknown

The Diners' Club, Inc., introduced the first universal credit card in 1950. Since then, credit cards have undergone various facelifts and added several attractive features. That is why, even after 73 years, credit cards remain relevant and an integral part of modern-day transactions. Those who understand how to use this versatile tool would vouch for its functionality, convenience, and security.

For others, there is something to learn from this article as we discuss the correct ways of using credit cards for maximum gains.

Responsible credit card usage

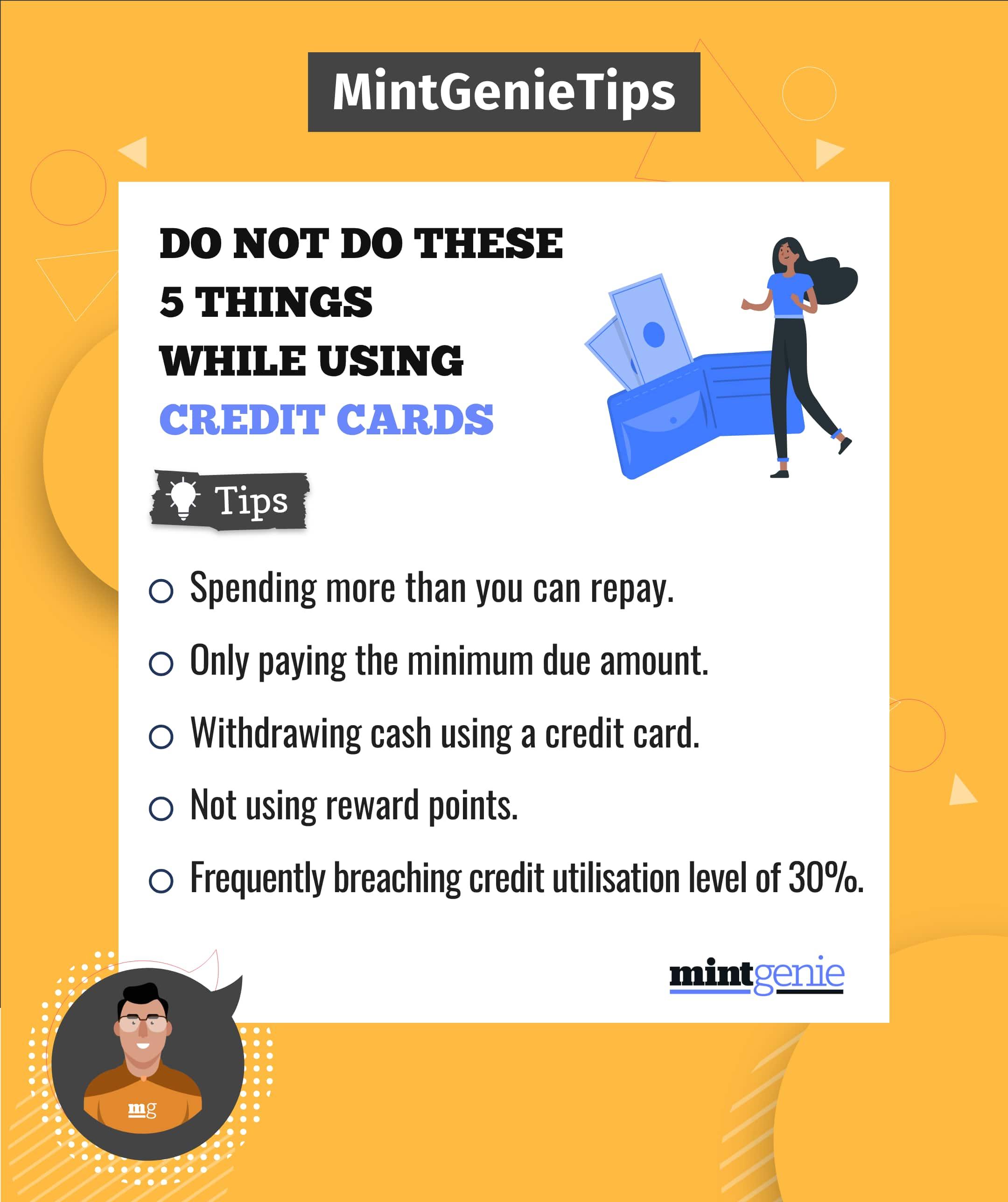

Using credit cards wisely is crucial for a strong financial future. Responsibly managing your credit cards involves three key principles: Spending within your means, paying the balance in full and on time, and keeping your credit utilisation in check.

Firstly, it's important to spend only what you can comfortably repay. Overspending can lead to unmanageable debt. Secondly, paying off your credit card balance entirely and punctually each month is a surefire way to establish good credit. This demonstrates reliability to lenders.

Moreover, keeping your credit utilisation (the ratio of credit used to your limit) between 20-30% and ensuring that credit card bills and loan payments don't exceed 50%-60% of your income safeguards your financial stability.

Many fall into the trap of revolving balance, relying on credit to cover expenses. Instead, consider using a personal loan to settle credit card bills strategically. By adopting these responsible habits, you can wield the benefits of credit cards while staying financially empowered.

Maximising credit card rewards and benefits

To get the most out of your credit card rewards, you need a smart plan. Start by understanding the rewards they offer, like cashback, points, and special perks. Use your card wisely by matching purchases with the best rewards. Next, choose a card that fits your lifestyle.

If you travel a lot, pick a card that gives travel rewards. If you want cash back for everyday spending, go for a cashback card. Use your rewards wisely too. Save up points for better rewards, catch limited-time deals, or use rewards for things like travel or reducing your bill. Just be careful with flashy milestone rewards. If you can't pay your bill in full, high interest charges can erase those extra rewards.

Managing a high credit card balance

Managing a high credit card balance requires a smart approach. Sometimes, when your regular expenses exceed your income, or when you make a big unexpected purchase, you can end up with an unmanageable credit card bill.

Here's how to take control of your money situation step by step. First, see exactly how much you owe and make a detailed budget to keep track of what you earn and spend. Cut down on things you don't really need so you can use that money to pay off your debt. It's always best to pay your credit card bill in full since unpaid dues are charged interest rates between 3%-4.5% monthly and from the date of purchase. But if you can't, there are other options that can be more affordable and structured. Taking a personal loan with a lower interest rate is the best option.

However, this option must be exercised much before your bill is due. Unpaid dues on your report can result in loan rejections. You can also talk to your credit card company about lowering your interest rate or working out a plan to pay back what you owe. Avoid using your card for new purchases and focus on paying down your existing balance. If you're not sure what to do, getting advice from a financial expert can really help.

A great way to control your spending is to use your bank's mobile app. It lets you set limits for how much you can spend on your credit card. You can set different limits for different types of spending – online or in stores. Once you reach a limit you set, your card won't work for more purchases. This is a smart way to be responsible with your spending. While it's okay to raise the limit in emergencies, it's important to stay disciplined in regular times for good money management.

Finally, if you have a big one-time expense that's more than your monthly income, think about whether it's better to use an EMI arrangement on your credit card or a personal loan. Go for the option with the lower interest rate. This careful decision can help you control your finances and avoid getting trapped in growing debt.

How to save on interest?

One effective strategy is considering a lower-cost personal loan to pay off a high-interest credit card balance. Personal loans often come with lower interest rates compared to credit cards, making them an attractive option for debt consolidation. Individuals can reduce the overall interest burden by using a personal loan to pay off their credit card balance and simplify their debt repayment with fixed monthly instalments. Additionally, it can help improve credit scores by lowering credit utilisation and demonstrating responsible debt management.

However, it's essential to compare loan offers from various lenders and ensure that the interest rate, repayment terms, and fees of the personal loan are favourable before making a decision. Responsible financial planning and the right debt consolidation approach can pave the way toward a more secure and debt-free financial future.

Conclusion

Gaining expertise in credit card usage is pivotal in attaining financial stability. Taking charge of one's economic well-being involves adopting responsible practices and implementing effective strategies to manage credit card balances. Utilising lower-cost personal loans to address credit card dues can be a prudent move, leading to significant interest savings and paving the way to a financially secure future. Armed with knowledge and discipline, individuals can intelligently harness the potential of credit cards, steering them toward their desired financial goals.

Gaurav Chopra, Founder & CEO, IndiaLends-online marketplace for credit products