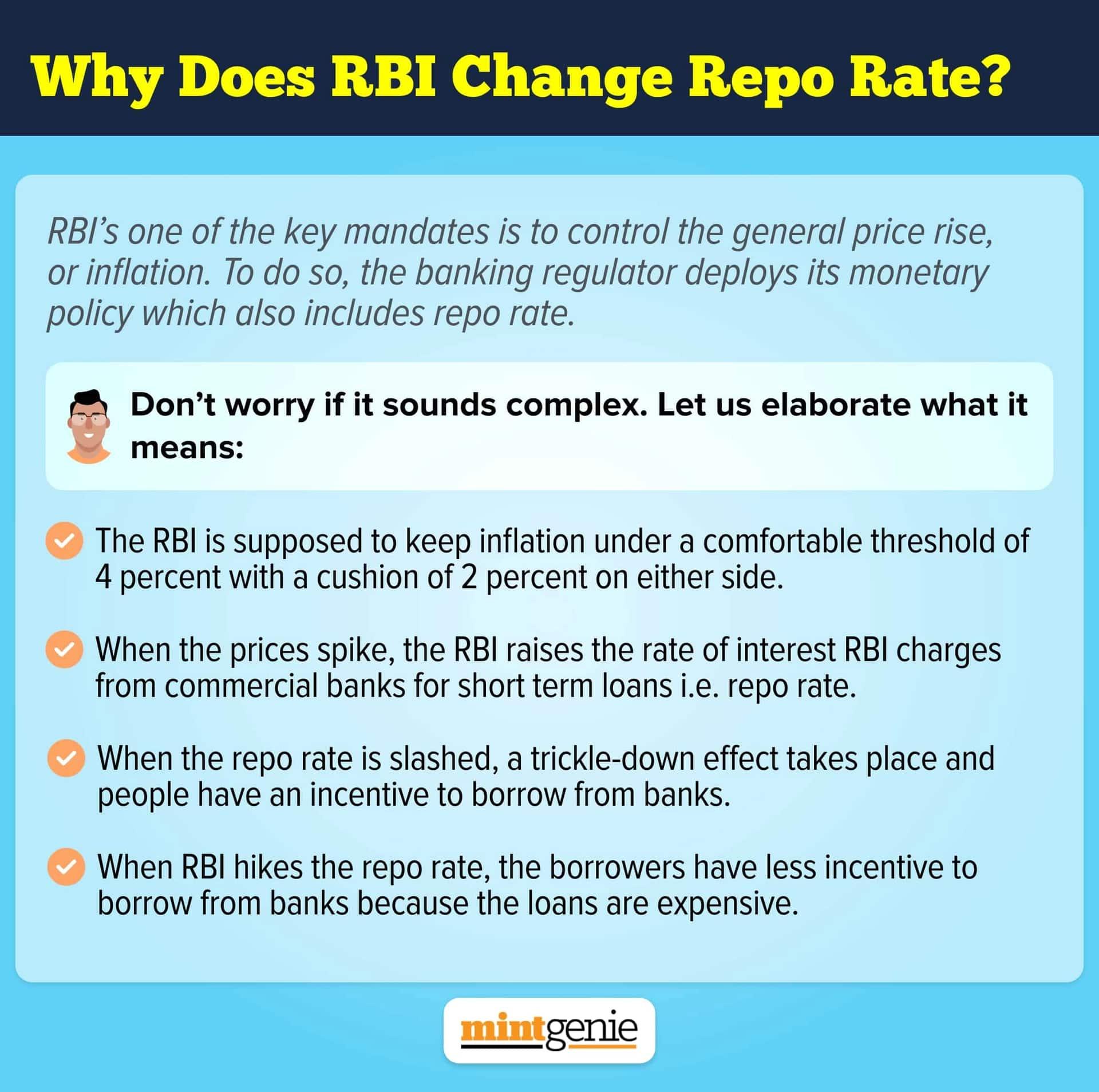

In a major announcement, the Reserve Bank of India (RBI) made the decision to keep the repo rate unchanged at 6.5 percent in the June policy for the second consecutive meeting. This decision was influenced by the notable correction in the Consumer Price Index (CPI) inflation trajectory.

The repo rate is the interest rate at which the RBI lends funds to commercial banks. When there is a high level of inflation in the economy, the RBI tends to increase the repo rate. This discourages commercial banks from borrowing money from the RBI, thereby reducing liquidity in the market and helping to control inflation.

The relationship between the repo rate and home loans is significant. Home loans in India often come with floating interest rates that are linked to external benchmarks, including the repo rate. Consequently, any changes in the repo rate directly impact the interest rates on floating-rate home loans. Let us understand it in detail.

How does the repo rate affect home loan EMIs?

The repo rate serves as a benchmark for interest rates in the banking sector. For borrowers with floating-rate home loans, any change in the repo rate will lead to a corresponding change in their home loan interest rates and subsequently impact their EMIs.

When the RBI decreases the repo rate, it becomes cheaper for commercial banks to borrow funds from the central bank. As a result, banks may lower their lending rates, including home loan interest rates. This reduction in interest rates translates into lower EMIs for borrowers.

Conversely, when the RBI increases the repo rate, banks' borrowing costs go up. To maintain their profitability, banks may increase their lending rates, including the interest rates on floating-rate home loans. This results in higher EMIs for borrowers, increasing the overall cost of their home loan.

Some borrowers opt for fixed-interest rate home loans, where the interest rate remains constant throughout the loan tenure. In such cases, changes in the repo rate do not immediately impact the EMIs during the fixed rate period.

As RBI keeps the rates unchanged; how will it impact the borrowers?

Commenting on the repo rate announcement, Anuj Puri, Chairman of ANAROCK Group said, “As was anticipated, the RBI has decided to keep the repo rates unchanged at 6.5%. This gives some respite to prospective homebuyers looking to avail of home loans in the near future. The unchanged repo rate can help maintain the momentum in housing sales, which has so far been firing on all cylinders in 2023. Given the current unchanged rates, the outlook for those looking to buy their first home via a home loan soon remains favourable.”

Adding his views, Adhil Shetty, CEO of Bankbazaar said, “The worst seems to be over. Interest rates are stabilizing. Inflation permitting, we may see rates drop before the end of 2023. If you’re on a repo-linked loan, your rate should automatically reset after any repo rate change within a quarter. The lowest rates being offered in the home loan market today are in the range of 8.40 to 8.50 for eligible borrowers. If you’re paying a significantly higher rate, consider a refinance. If you’re able to shave off 50 basis points or more off your rate, it could lead to significant savings over the long term.”

Ramani Sastri, Chairman & MD, Sterling Developers added, “The decision to keep the repo rate unchanged is a positive development for home buyers and investors, as it provides them with some stability and reduces uncertainty and volatility associated with interest rate fluctuations. India’s housing sector is witnessing a strong rebound in the recent past driven by various factors such as affordability, lifestyle upgradation and aspiration of customers to own homes and we see this up-cycle continuing in 2023 fuelled by both end-user and investor interest.”

Speaking on the same, Lincoln Bennet Rodrigues, Chairman & Founder, The Bennet and Bernard Company mentioned, “We welcome this move by RBI as it helps in holding the interest rates and sustaining the growth momentum in the real estate sector. With the growing economy and an increasing number of high-net-worth individuals and aspirational middle-class millennials and Gen-Z, the demand for luxury properties has seen an exponential rise.”

“Thus, a reduction in the key rates going forward would be widely celebrated as low-interest rates have been a crucial factor in the revival of overall real estate demand and improvement in the liquidity situation which is vital for the sector,” he added.

The repo rate plays a crucial role in shaping the interest rates on financial products in India, including home loans. To make informed decisions about buying a home, it is essential to grasp the concept of the repo rate and its implications for home loan borrowers.