Credit card debt is for real. This is evident from recent data shared by the Reserve Bank of India (RBI) that revealed a whopping outstanding credit card debt of more than ₹2 lakh crores in April this year. Though lending companies are not too concerned about this humongous debt, the country’s Central Bank has raised concerns about the growing nature of “unsecured debt” and its possible effect on investors’ portfolios in the long run.

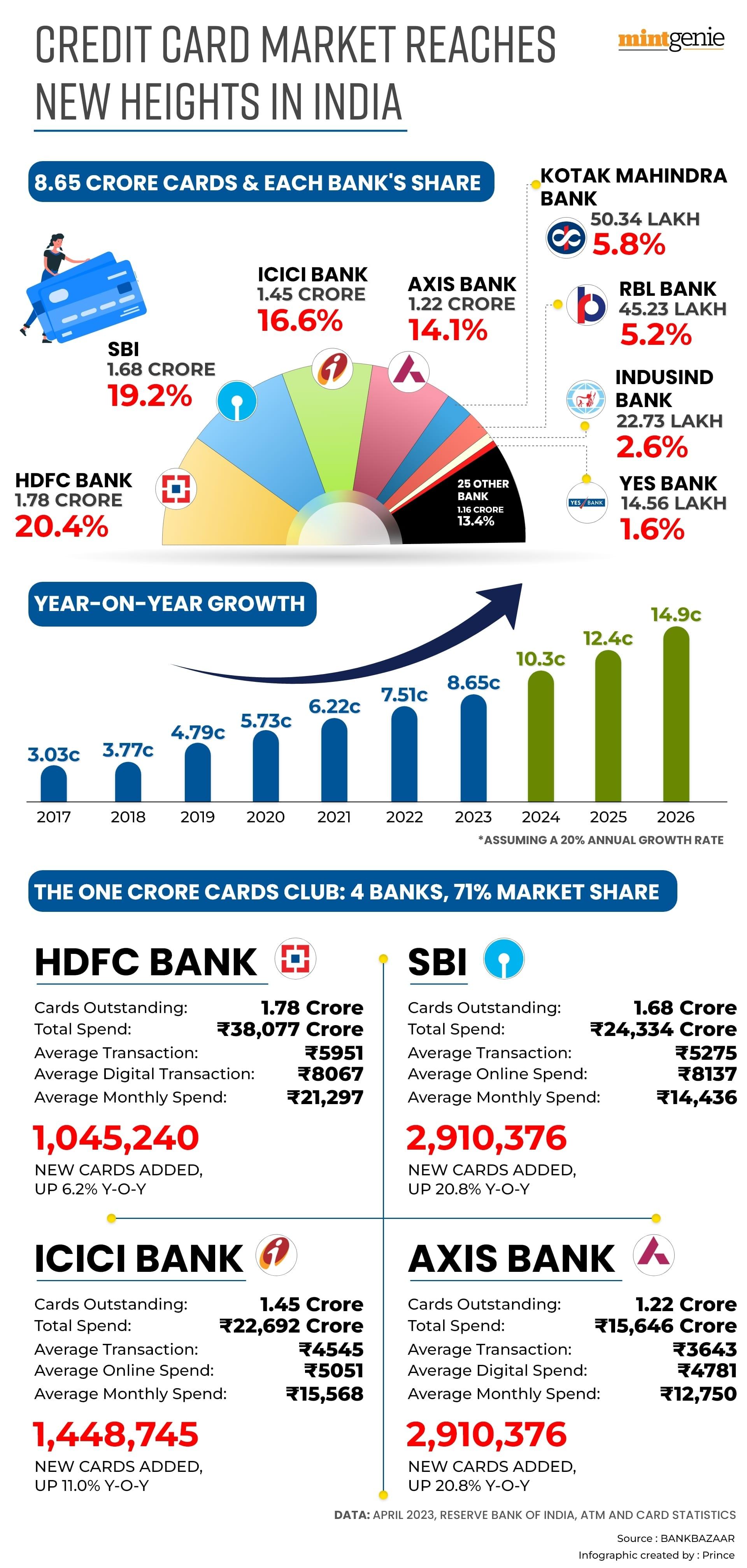

According to data released by the Reserve Bank of India, the number of credit cards in circulation surpassed 86 million in April 2023. This figure represents a significant increase of approximately 15 per cent compared to April 2022, when the total stood at 75 million credit cards. It would not take too long for us to reach the 100 million cards mark.

A recent survey titled “India Credit Card Report” by BankBazaar reveals the following key details.

- Just four banks account for 71 per cent of all credit cards.

- The average transaction in April was ₹5120.

- The industry average monthly spend per card was ₹15,388.

- CSB, South Indian Bank, and Federal Bank are the most frequently used cards on average, with around four spends per month per card.

- Karur Vysya, IndusInd, and CitiBank account for the highest monthly spending per card of over ₹27,000.

- CitiBank, Amex, and IndusInd account for the highest online spending as a percentage of their total spending, with over 70 per cent of all their transactions being online.

Does increasing credit card debt indicate consumer confidence?

The burgeoning credit card use reflects the changed lifestyle of today’s generation. As opposed to our elders who were wary of taking loans or incurring unwanted debt, today’s generation relies more on credit debt for almost everything. While the tendency to “Buy Now, Pay Later” can be handy in certain instances, especially, during emergencies, using credit cards to avail of reward points can be a cause of concern. More people are now using these cards to make “big-ticket” purchases, pay off their no-cost EMIs, and improve their lifestyle habits.

Naysayers claim that rising credit card debt is a sure-shot sign of potential indebtedness; the optimistic look at it as an opportunity to further India’s dream of relying only on digital payment. Depending on how one views it, credit card debt can be rewarding or damaging in the long run. However, more than the lingering and recurring debt, more concerning is how to repay it.

Not repaying credit card debt in time can wreak havoc on your credit score. It is crucial to avoid maxing out your credit card due to the potential consequences. Utilizing your entire credit limit can lead to a decrease in your credit score. Consequently, a lower credit score may result in higher interest rates for future credit cards or loans you apply for. Moreover, it can have a negative impact on your ability to secure loans (home loans or vehicle loans, or personal loans) or avail of a second card or other services.

Adhil Shetty, CEO, BankBazaar.com, said, “Credit cards often come with high-interest rates, especially for unpaid balances. Carrying a balance and accruing interest can lead to significant debt over time, making it harder to pay off the balance. Your credit card debt also directly affects your credit score. High levels of debt relative to your credit limit can negatively impact your credit utilization ratio. This, in turn, can affect your ability to secure loans or credit in the future and may result in higher interest rates for other financial products.”

“Ultimately, carrying significant credit card debt can strain your financial stability and hinder your ability to achieve financial goals by limiting your ability to save, invest, or make necessary purchases. This can create a cycle of dependency on credit and hinder your overall financial well-being. So, in all, being mindful of credit card debt helps maintain a healthier financial mindset and promotes peace of mind, allowing you to focus on long-term financial goals rather than being burdened by debt,” added Shetty.

Getting rid of debt in time

Many debtors complain about how increased rates caused their credit card debt to go up in the past few months. However, with unchanged repo rates as announced by the RBI, repaying credit card debt may be a lot easier than you think.

A lower repo rate translates to lower lending rates, thus, allowing borrowers to repay their debt quickly or opt for credit refinancing to repay the debt incurred. There is no way one can determine if repo rates would go up or further down in the near future, thus, prompting the idea to act quickly.

Debtors can either consolidate their current debt position on multiple credit cards and try to repay the amount at one source or attempt to repay at least 75 per cent of the loan amount. Apart, they must take care not to incur further debt unless the earlier one is repaid and done away with.

Given the stagnant repo rates for now, how do you advise credit card borrowers to repay their debt in time? Viral Bhatt, Founder, Money Mantra advised the following tips and tricks to get rid of credit card debt early.

Make a budget and stick to it: This will help you track your income and expenses so you can see where your money is going. Once you know where your money is going, you can start to make changes to free up more money to pay off your debt.

Pay more than the minimum payment: The minimum payment is just enough to keep your account in good standing, but it won't help you pay off your debt any faster. If you can afford to, try to pay more than the minimum payment each month. Even a small amount can make a big difference over time.

Consider a balance transfer: If you have high-interest credit card debt, you may be able to save money by transferring your balance to a card with a lower interest rate. Just be sure to read the terms and conditions carefully before you transfer your balance, and make sure you can make the payments on time.”

Credit card debt is a reality. It is like any other debt, which means that you cannot play around with it hoping that it would dissipate gradually. Irrespective of what it takes, credit card borrowers must prioritize repaying the accrued debt well before the due date.