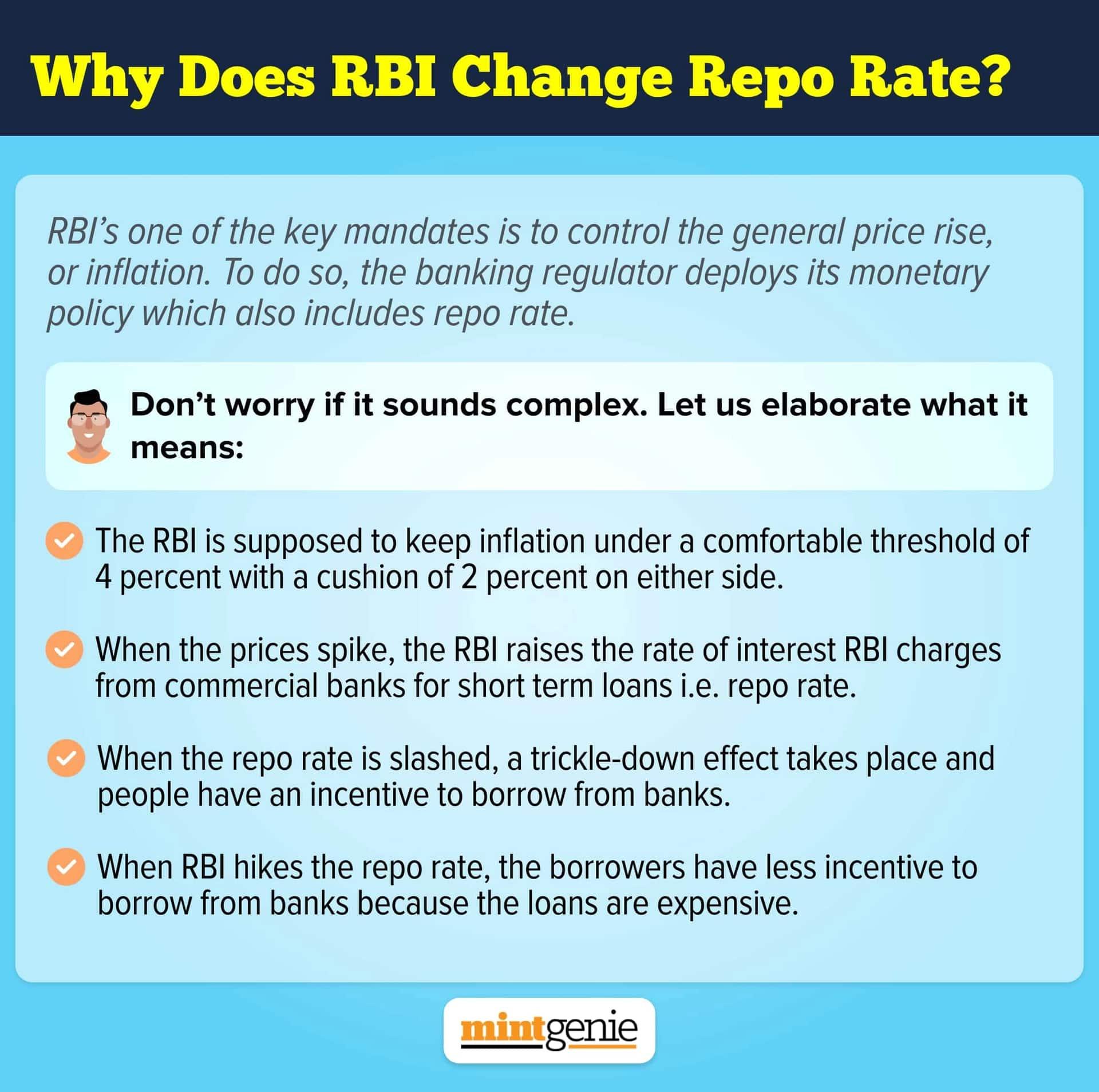

The Reserve Bank of India’s recent decision to keep the repo rates unchanged has come as a relief for many, especially, borrowers who had to bear the brunt of the increased interest component in their loans. The RBI's consecutive repo rate hikes, aimed at managing inflation and maintaining a steady flow of liquidity in the economy, led to the interest rates nearing their peak.

A higher interest amount translated to an increased loan tenure or higher equated monthly instalments (EMIs) for many borrowers with some even complaining how their intent to get rid of debt early in life failed as the loan period commensurated with continued repo rate hikes.

Homebuyers burdened with a huge debt are now heaving a sigh of relief. Basavaraj Tonagatti, a Certified Financial Planner (CFP), SEBI Registered Investment Adviser and a Finance Blogger at BasuNivesh said, “Homebuyers will undoubtedly feel relieved because the interest rate may possibly be held steady by the lenders. A rapid rate drop, though, might not be anticipated. But if we judge the 10-year G-Secs’ yield movement during the past six months, it is now a sign that inflation is slowing, therefore interest rates may either stay the same or even go down in the future.”

Many economists have welcomed the country’s Central Bank’s decision to keep the repo rates unchanged while expecting a rate cut in the coming quarter. Interest rates have not come down yet, though the rates seem to be stabilizing as a consequence of the dropping inflation rate. Since loan interest rates are not fixed and are linked to repo rates decided by the RBI each quarter, there is a high possibility of borrowers benefiting from lower loan rates by the end of this year.

The lowest home loan interest rates in the market range from 8.40 per cent to 8.50 per cent. However, if the current interest rate you are paying on your loans is higher, you may either opt for your lender to lower the rates or consolidate your debt in favour of a new lending organization like a bank or a fintech organization. Debt refinancing through debt consolidation is indeed a smart way of reducing your overall loan and interest burden while easing down on the extended loan tenure due to increased rates.

Now that the repo rates have stabilized and are expected to trim down in the next quarters, you may as well plan in advance how to ensure loan repayment in time or resort to loan prepayment to ensure that much of your finances are directed towards savings and investments than relieving yourself of the home loan sought.

Take, for example, you may have sought a home loan of ₹50 lakhs repayable over the next 30 years with the EMIs amounting to ₹38,446 every month. This loan tenure is huge considering how the total amount payable would be ₹1,38,40,443.

Principal Amount: ₹50 lakh

Interest Rate: 8.5%

Loan Tenure: 30 years

Monthly Home Loan EMI: ₹38,446

Interest Amount: ₹88,40,443

Total Amount Payable: ₹1,38,40,443

However, if you increase your EMIs to ₹40,261, you will find your loan tenure automatically lowered to 25 years. Simply increasing your EMIs by ₹1800 can allow you to be freed of your loan in 25 years instead of the long three decades that were decided at the time of borrowing.

Principal Amount: ₹50 lakh

Interest Rate: 8.5%

Loan Tenure: 25 years

Monthly Home Loan EMI: ₹40,261

Interest Amount: ₹70,78,406

Total Amount Payable: ₹1,20,78,406

With companies having doled out annual appraisals and bonuses, paying a monthly EMI of ₹43,391 does not look much difficult. However, this decision of enhanced EMIs will finish off your loan in 20 years instead of 30 years, thus, lending you enough reason to prepay your lingering loan amount.

Principal Amount: ₹50 lakh

Interest Rate: 8.5%

Loan Tenure: 20 years

Monthly Home Loan EMI: ₹43,391

Interest Amount: ₹54,13,879

Total Amount Payable: ₹1,04,13,879

Furthermore, when the repo rate decreases, it results in a reduction in borrowing costs. This presents an opportunity for existing homeowners to refinance their loans and benefit from the lower interest rates. Homeowners can choose to either decrease their EMIs or shorten the duration of their loan. In either scenario, the lowered rates allow homeowners to save more money.

Suresh Sadagopan, MD & Principal Officer, Ladder7 Wealth Planners said, “In a high-interest environment like now, it is either keeping the EMIs constant or increasing the tenure. As much as possible, I would suggest keeping the tenure constant and increasing the EMIs’ amount if feasible. If that is not, one may have to keep the EMIs constant which automatically will increase the tenure.”

Borrowers must understand that the changes in repo rates are not permanent. They may be hiked in the long run if the RBI feels the need to do so. The current geopolitical tensions and an escalating skirmish between various countries can result in full-fledged tension, thus, affecting inflation rates.

This can also cause the repo rates to go up, thus, impacting your loan interest rates. This also explains the imperative need to focus on your loan repayment or rather loan prepayment to not succumb to increasing repo rate hikes.