Borrowers with high EMIs may find it challenging to manage their monthly finances, says Shreyans Nahar, CEO & Co-Founder, Finsire.

In an interview with MintGenie, Nahar said personal loans are popular among borrowers who need funds for various purposes.

Edited Excerpts:

Q. How can high net-worth NRIs leverage loans against the assets they hold in India?

High net-worth Non-Resident Indians (NRIs) can leverage loans against the assets they hold in India by utilizing various financial products and services available to them. Some of the ways in which they can obtain loans against their assets are:

Loan against property (LAP): High net-worth NRIs can avail of loans against their residential or commercial properties in India. Many banks and non-banking financial companies (NBFCs) offer these loans at competitive interest rates. An advantage here is that the loan tenure can be for a long duration ranging from five to 20 years.

Loan against securities (LAS): NRIs can also avail of loans against their investment in financial instruments like stocks, bonds, mutual funds, or fixed deposits held in India. Dematerialization of securities and digital Infratech of asset holding depositories have paved a way for a more interoperable LAS. An advantage here is that the lender can digitally fetch all the securities held by the user, who can pledge their assets for a loan at comparative ease.

It is essential to approach multiple lenders and compare the options to find the best loan product that meets all requirements. Consulting a financial advisor can also help in making an informed decision.

Q. Which kinds of loans among personal loans, gold loans and loans against securities do most people opt for?

The choice of loans among personal loans, gold loans, and loans against securities depends on various factors like an individual's financial needs, preferences, and the assets they possess. Each type of loan has its benefits and drawbacks, which determine its popularity among borrowers. Here's an overview of the three loan types and when they are typically preferred:

Personal loans: Personal loans are unsecured loans, which means they do not require any collateral usually. They are popular among borrowers who need funds for various purposes like medical emergencies, home renovations, vacations, or debt consolidation. Personal loans are often preferred due to minimal documentation, and the flexibility to use the funds as needed. However, personal loans come with higher interest rates compared to secured loans such as LAS.

Gold loans: Gold loans are secured loans where the borrower pledges gold as collateral. They are popular among borrowers who need immediate funds and own gold assets. Gold loans typically offer lower interest rates compared to personal loans, have minimal documentation requirements, and provide faster processing times. However, the loan amount depends on the value of the gold pledged, and the borrower risks losing the gold if they default on the loan repayment.

Loans against securities: These loans are secured against financial instruments like stocks, bonds, or mutual funds, which the borrower owns. Loans against securities are often preferred by borrowers who have invested in such assets and need funds without liquidating their investments. These loans typically have lower interest rates than personal loans and offer flexibility in repayment. However, the loan amount depends on the value and type of the security pledged, and the borrower may be required to maintain a specific margin or risk liquidation.

In general, personal loans are quite popular among borrowers who don't want to pledge collateral or don't own significant assets. Gold loans and loans against securities are more popular among those who possess such assets and seek lower interest rates. Ultimately, the choice of a loan depends on the borrower's individual circumstances, financial needs, and risk appetite.

Q. Amidst rising interest rates, many borrowers are finding it difficult to pay off their high EMIs. How do you advise them to get rid of this unforeseen added liability?

Amidst rising interest rates, borrowers with high EMIs may find it challenging to manage their monthly finances. Here are some strategies they can adopt to mitigate the impact of rising interest rates and reduce their liability:

Refinancing the loan: Consider refinancing the loan with another lender that offers a lower interest rate. This strategy can help in reducing the overall interest cost and EMI burden. However, it's essential to account for any prepayment charges or processing fees involved in refinancing.

Increase the loan tenure: Approach the current lender and request an extension of the loan tenure. This would help lower the EMI amount, making payouts more affordable every month. However, keep in mind that increasing the loan tenure will also increase the total interest paid over the life of the loan.

Prepay or make part payments: If the borrower has some surplus funds, they can consider prepaying a part or the entire loan amount. This step will help in reducing the outstanding principal and, consequently, the interest cost. Before doing this, verify if there are any prepayment charges associated with the loan.

Opt for a fixed interest rate: If the borrower has a floating interest rate loan, they can consider switching to a fixed interest rate loan to protect themselves from further rate hikes. However, fixed interest rates are generally higher than floating interest rates, so this option should be considered carefully.

Review the household budget: Reassess the household budget and identify areas where expenses can be reduced. Redirecting these savings towards loan repayment can help in easing the EMI burden and reduce the outstanding loan amount.

Consolidate debt: If the borrower has multiple loans with varying interest rates, they can consider consolidating these debts into a single loan with a lower interest rate. This approach can simplify the repayment process and reduce the overall interest cost.

Increase income: Explore ways to increase income, such as taking up part-time work, freelancing, or investing in income-generating assets. An increase in income will help in managing the EMI burden more effectively.

Seek professional advice: Consult a financial advisor for personalized advice based on the borrower's financial situation and goals. They can recommend appropriate strategies for managing the increased EMI burden.

It’s crucial for borrowers to be proactive in managing their loan repayments amidst rising interest rates. By employing these strategies, users can reduce their financial burden and manage their debt better.

Q. Rising number of lending companies in India allows more people to live on credit. Do you think this will turn the coming generation credit hungry compared to millennials?

The growing number of lending companies and the ease of access to credit in India do create an environment where people may be more inclined to rely on credit for their needs. This trend has the potential to make the coming generation more credit hungry compared to millennials. However, it is important to consider a few factors:

Financial awareness: The rise of financial education and awareness, along with easy access to information on personal finance, can help the coming generation make informed decisions regarding credit. If younger generations are equipped with financial literacy, they can responsibly manage credit and use it as a tool to achieve financial goals.

Cultural shifts: As society evolves, there might be a shift in attitude towards credit usage. The coming generation might be more comfortable using credit products compared to the previous generations, who may have been more conservative when it came to borrowing.

Consumerism: With an increase in consumerism and the desire for instant gratification, younger generations might be more inclined to use credit for purchasing products and services they desire. This tendency could potentially result in higher levels of debt.

Economic factors: The overall economic situation and job market also play a significant role in credit usage. If the coming generation faces challenges such as income inequality, job insecurity, or inflation, they might be more inclined to rely on credit to meet their financial needs.

Access to digital platforms: The rise of digital lending platforms and fintech companies has made it easier for individuals to access credit quickly and conveniently. This increased access to credit could encourage the coming generation to rely on loans and credit cards more frequently.

While it is possible that the coming generation might become more credit hungry compared to millennials, responsible credit usage ultimately depends on an individual's financial education, discipline, and awareness. Encouraging financial literacy and promoting responsible credit behavior from an early age can help prevent excessive debt and create a financially stable future for the next generation.

Q. April is known as Financial Literacy Month. Do you think as a nation we are still way behind when it comes to educating people on how to deal with their finances?

It is accurate to say that many countries still have room for improvement when it comes to financial literacy. Financial education is an essential aspect of building a healthy financial future, yet gaps in understanding and knowledge persist across different demographics and regions.

Several factors contribute to the varying levels of financial literacy:

Education system: In many countries, personal finance is not a mandatory part of the curriculum in schools, resulting in a lack of basic financial knowledge among the population. Integrating financial education into the curriculum can help improve financial literacy from an early age.

Socioeconomic factors: Access to financial services and products varies across different socioeconomic groups, and those from lower-income backgrounds may have limited exposure to banking, credit, and investment options. This lack of exposure can contribute to lower levels of financial literacy.

Cultural attitudes: Cultural factors may influence attitudes towards money management and savings. In some societies, discussing money and personal finance is considered taboo, which may limit opportunities to learn from family members or peers.

Digital divide: The digital divide can also contribute to disparities in financial literacy, as those without access to the internet may have limited opportunities to access online financial education resources.

Complexity of financial products: The ever-evolving financial landscape, with new products and services being introduced, can make it challenging for individuals to keep up with the latest financial tools and strategies.

Efforts to promote financial literacy can take various forms, including government initiatives, non-profit organizations, financial institutions, and public awareness campaigns. Celebrating events like Financial Literacy Month is an opportunity to emphasize the importance of financial education and encourage individuals to take charge of their financial well-being.

In conclusion, while progress has been made in some areas, there is still significant work to be done to improve financial literacy across nations. This ongoing challenge requires a multi-faceted approach involving government, educational institutions, and private and public organizations to promote financial education and awareness.

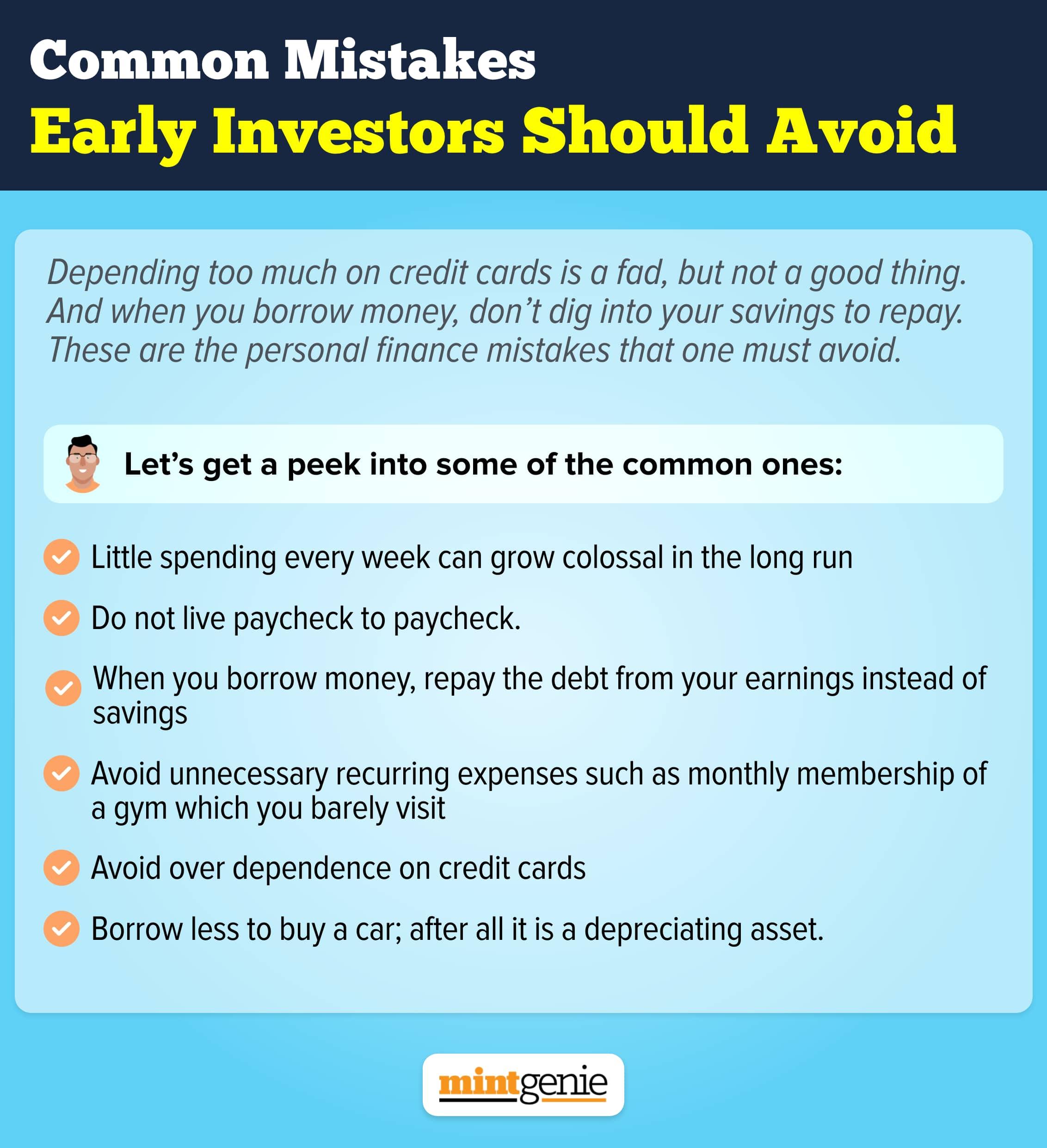

Q. What is your advice to new-age investors planning their investments?

New-age investors should consider the following advice when planning their investments:

Set clear financial goals: Identify short-term, medium-term, and long-term financial goals, and determine the required investment amount, time horizon, and risk tolerance for each goal.

Educate yourself: Learn the basics of personal finance and investing, including concepts such as diversification, asset allocation, and risk management. Stay informed about financial markets and investment options.

Start early and invest regularly: The sooner you start investing, the more time your investments have to grow and benefit from the power of compounding. Consider making regular investments through systematic investment plans (SIPs) or dollar-cost averaging to mitigate market volatility.

Diversify your investments: Diversify your portfolio across different asset classes such as equities, fixed income, real estate, and commodities. This approach helps to spread risk and potentially achieve more stable returns over time.

Understand your risk tolerance: Assess your risk appetite based on factors such as age, financial goals, income, and personal preferences. Allocate your assets accordingly to ensure that your portfolio aligns with your risk tolerance.

Keep emotions in check: Avoid making investment decisions based on emotions or market hype. Stay focused on your long-term financial goals and maintain a disciplined investment approach.

Monitor and rebalance your portfolio: Regularly review your portfolio's performance and rebalance it as needed to maintain your desired asset allocation. This process can help to manage risk and stay on track to achieve your financial goals.

Seek professional advice: If you are unsure about your investment strategy or require assistance in managing your portfolio, consider consulting a financial advisor who can provide personalized advice based on your unique financial situation and goals.

Plan for taxes: Be aware of the tax implications of your investments and utilize tax-efficient investment options and strategies to maximize your after-tax returns.

Keep costs in check: Be mindful of fees and expenses associated with your investments, such as brokerage fees, fund management fees, or transaction costs. High fees can eat into your returns over time.

By following these guidelines, new-age investors can create a well-rounded investment strategy to help them achieve their financial goals and build wealth over time. It's crucial to remain disciplined, stay informed, and adapt your investment plan as needed to navigate the ever-changing financial landscape.

Q. Deciding between loan repayment and continuing investments is difficult. How do you advise people to balance between the two?

Balancing between loan repayment and continuing investments can be challenging, as it requires careful consideration of various factors. Here are some steps to help individuals decide how to allocate their resources between these two financial priorities:

Assess interest rates: Compare the interest rates on your loans with the expected return on your investments. If the loan interest rate is significantly higher than the anticipated return on investments, it may be more cost-effective to prioritize repaying the debt. On the other hand, if the expected return on investments is higher, it might make more sense to continue investing while maintaining regular loan repayments.

Consider loan type: The type of loan can also influence your decision. High-interest loans, such as credit card debt or personal loans, should generally be prioritized for repayment, whereas low-interest loans, like mortgages or student loans, might allow for a more balanced approach.

Evaluate risk tolerance: Consider your risk tolerance and investment horizon. If you are risk-averse or have a shorter investment timeframe, you might prioritize loan repayment to reduce financial risk. However, if you have a longer investment horizon and higher risk tolerance, you might continue investing to potentially achieve higher returns.

Establish an emergency fund: Before focusing on loan repayment or investments, ensure that you have an emergency fund in place to cover unexpected expenses. A general rule of thumb is to maintain three to six months' worth of living expenses in a readily accessible savings account.

Prioritise financial goals: Assess your short-term and long-term financial goals, and allocate your resources accordingly. If paying off debt is a higher priority for you, focus on loan repayment. If building wealth and growing your investments is more important, maintain a balance between loan repayment and investing.

Maintain a balanced approach: Strive for a balance between loan repayment and investing by allocating a portion of your income towards both goals. You can adjust the allocation based on your financial priorities, risk tolerance, and investment horizon.

Revisit your budget: Regularly review your budget and identify areas where you can cut expenses or increase income. Redirect these savings towards debt repayment or investment, depending on your financial priorities.

Seek professional advice: Consult a financial advisor for personalized guidance based on your unique financial situation and goals. They can help you create a tailored plan to balance loan repayment and investments effectively.

Ultimately, the decision between loan repayment and continuing investments depends on your financial situation, risk tolerance, and long-term goals. A balanced approach that accounts for these factors can help you make the most of your resources and achieve financial stability.