There has been a significant rise in the demand for short-term loans, specifically driven by the growing gap between income and expense coupled with the rising aspirations among people, especially the millennials. The disruptions of the pandemic having affected the normalcy of business operations, resulting in mass-scale job losses, have further bolstered the popularity of short-term loans.

Catering to the increasing requirements of people, lending institutions like banks and non-banking financial companies (NBFCs) have redrafted their strategies to enable borrowers to avail of easily accessible loans.

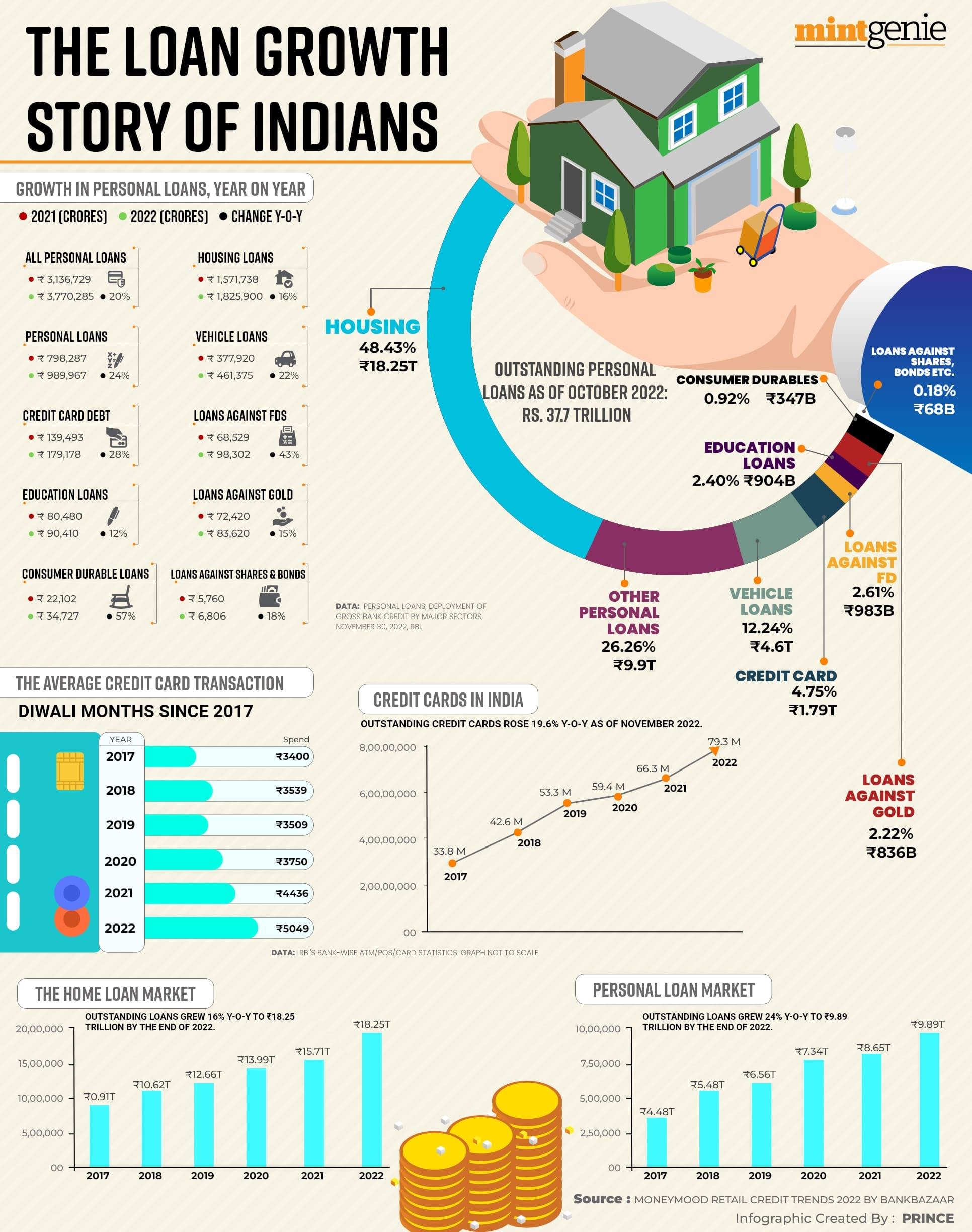

As of March 2022, the lending market in the country was valued at ₹174.3 lakh crore, up by 11.1 per cent on an annual basis, as compared to the same period last year. The commercial, retail, and microfinance lending portfolios contributed 49.5 per cent, 48.9 percent, and 1.6 per cent, respectively, till March 2022.

Short term loan

The short-term loans are small financial transactions between the borrowers and the lenders like banks and non-banking financial companies (NBFCs), based on the immediate requirements of the borrowers. The primary difference between the short-term personal loans and conventional loans is that the waiting time for the loan to get approved is significantly less in short-term loans, which also involves less paperwork or verification formalities.

The personal loan market grew from ₹75,088 crore in Financial Year 2019 to 147,236 crore in FY 2022 – a steep four times growth, with loans being disbursed to 158.1 lakh accounts in FY 2022 as compared to 39.9 lakh accounts in FY 2019. The average ticket size of instant personal loans has also gone down significantly – reducing by 40 per cent from ₹2.4 lakh in FY17 to ₹1.5 lakh in FY21.

Major non-banking financial institutions have been aggressively chalking out plans to give a thrust towards making short-term, unsecured loans easily available for young consumers, bringing the rise in personal loans in the range of ₹2,000 to ₹50,000.

Within the personal loan pie, the short-ticket loans have grown with an increase of over 11 per cent in the number of loans disbursed per year from 2017 to 2022. Among this, sachet loans below ₹10,000 have grown over 20 times in just four years. The steady and steep growth has been mostly facilitated by the NBFCs, who came up with out-of-the-box schemes like buy-now-pay-later (BNPL) and no-cost EMI on all kinds of consumer durables.

Types of short term loan

Trade Credit: One of the most affordable sources of obtaining interest-free funds, the trade credits can be availed when a lender gives the time to pay for a purchase without incurring any additional cost. Though trade credits are generally extended for 30 days, borrowers can consider asking for a longer tenor in accordance with their plans.

Bridge loans: Bridge loans are availed to tide over until one can avail another loan of a bigger value. The bridge loans are usually relevant for transactions relating to property. While there can be a significant waiting time to get approval for big amounts of loans like housing loans, a bridge loan can be availed easily during the waiting period to get the time and funds to manage expenses.

Demand loans: Demand loans are available to meet urgent financial obligation and insurance policies and other financial instruments can be kept as collateral to avail such instant loans. The percentage of the maturity value of such financial instruments determines whether a borrower is eligible to avail a demand loan.

Bank overdraft: Bank overdraft can be availed easily based on the current account and with the facility one can withdraw money despite not having sufficient cash on his / her account.

Personal loan: Personal loans are one of the most popular forms of financial instruments that borrowers avail to meet basic expenses like home renovation, wedding, higher education, travel cost, medical emergencies, etc. The personal loans are usually offered based on income level, employment, credit history and perceived repayment capacity.

NBFCs and Fintechs dominating short ticket loan segment

According to official data, on providing the small-term instant loans, the NBFCs have dominated the market on both volume and value metrics. Till 2017 and late 2018 the public sector banks were the biggest players in the small-ticket loan domain with their share being around 57 per cent in both volume and value in 2017, while the NBFCs stood at a mere 20.6 percent in the same fiscal year.

The strategic modifications and increasing trust among people catapulted the share of the NBFCs, making it 90.3 per cent of the total short-term loans in terms of volume and 68.2 per cent in terms of total loan value.

Interestingly, the requirement for the instant loans has been mostly prevalent among young individuals under the age of 35, who accounted for 54 per cent of total borrowers in financial year 2021. Furthermore, 22.8% of loans with ticket size less than ₹10,000 and 15% of loans with ticket size ₹10,000 - 25,000 were availed by individuals aged below 25 years.

Shift in demand towards smaller ticket loans, ease of access to credit, increased usage of digital platforms and entry of non–traditional lenders in the ecosystem have been some of the few reasons which prompted the popularity of the instant loans among the youths across the country.

Key advantages of short ticket loans

Shorter time for incurring interest: Usually repayments to a short term loan are done within a year; thereby, involving lower total interest payments. In other words, the amount of interest paid is significantly less as compared to conventional long term loans.

Quick funding time: The short term loans are less risky than the ones for a longer tenor, primarily because the borrower’s ability to repay a loan is less likely to change significantly over a short frame of time. Hence, the time taken by a lender to approve the small ticket loans is considerably less and borrowers can obtain the required funds almost instantly.

Easy to acquire: Since the requirements for the short term loans are generally easier to meet, such financing tools are of phenomenal help for businesses or individuals who suffer from less than stellar credit scores.

Less documentation involved: Since the loan amounts are significantly less and the time for repayment is also short, in case of short term loans the lenders need not to undergo an extensive check on the borrower’s credibility to pay back; thereby significantly reducing the paperwork and formal verification procedures.

Risk associated with short term loans

The primary disadvantage of the short term loans is that the loan amount is significantly less. Also, while availing a short term loan there might be variations in the interest rates depending on the lender and the process might also involve hidden clauses.

Hence, borrowers need to carefully go through all the terms and conditions and extensively check a lender’s credibility based on market research before applying for a short term loan.

Overall, the short term loans can be beneficial as it involves small amounts, so that the borrower won’t be burdened with large monthly payments. The personal loan sector in the country witnessed two-fold growth in financial year 2022 – a whooping four times growth from FY 2019.

While the public sector banks witnessed a significant decline in originations share by both value and volume, the non-banking financial players dominated the market with lucrative schemes and offers for easy financing.

Mahesh Shukla is the Founder & CEO of PayMe