During volatile times when markets have been falling with every passing day, one of the safe investment options is to put money in fixed deposits. And when it comes to a fixed deposit, there are some new options are available to choose from.

One of the most popular alternatives is to invest in a large commercial bank such as HDFC Bank, ICICI Bank, State Bank of India (SBI), Canara Bank, among others. Recently, most big banks raised interest rates on their deposits by 15-20 basis points. SBI increased its rates with effect from February 15 and new rates for HDFC bank became effective from February 14 this year.

The banks usually offer different kinds of FD options such as callable, non-callable and tax saving FDs. As the name suggests, callable FDs are the ones which can be withdrawn before maturity by forgoing some of the interest. At the same time, non-callable FDs can’t be withdrawn during the deposit’s tenure.

There are multiple ways to earn higher return on a fixed deposit.

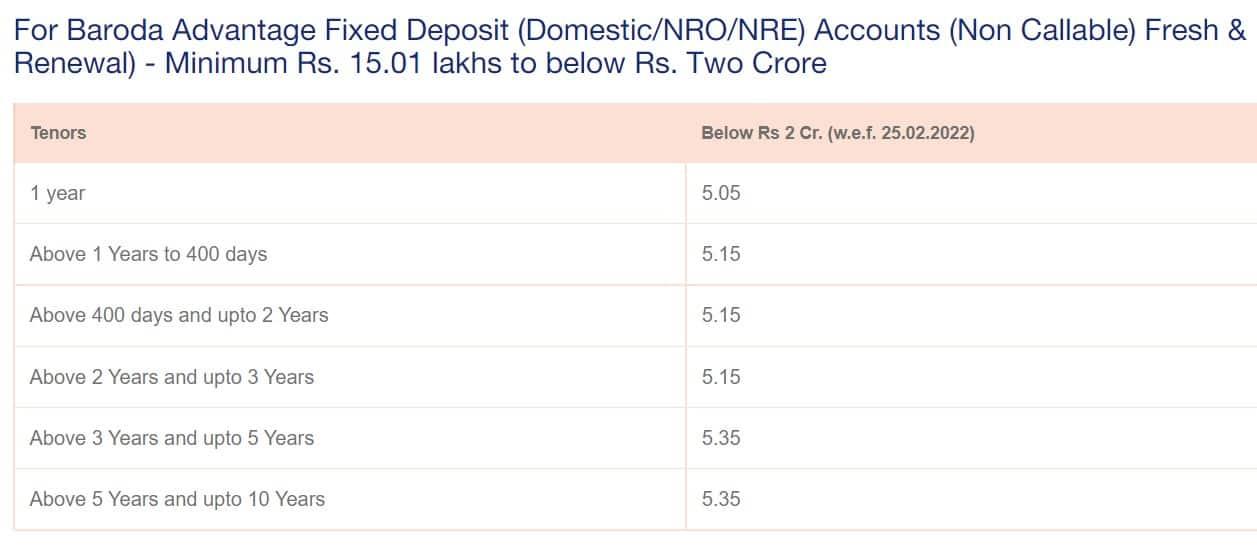

1 When FDs are non-callable: When fixed deposits can’t be withdrawn during the tenure, they offer a high rate of return. However, the minimum threshold is very high. Axis bank offers fixed deposit plus where the minimum threshold is ₹5 crore. Union Bank of India also offers slightly higher interest on its non-callable term deposits but the minimum amount to invest in ₹2 crore. For Bank of Baroda, this limit is ₹15 lakh.

This is what Bank of Baroda offers on non callable deposits:

2. When FDs are maintained by senior citizens: Every bank usually offers an extra 50 basis point return to senior citizens over those to others. For instance, when a bank offers 6 percent for its one-year FD to an adult Indian, the senior citizens will stand to receive 6.5 percent for the same.

3. FDs offered by NBFCs: Some non-banking financial corporations offer higher returns on their fixed deposits than by the large commercial banks. These NBFCs include Mahindra Finance, Bajaj Finance and Shriram Finance. Since corporate FDs are not as safe as bank FDs, depositors are expected to check the ratings of these deposits before investing money into it. The safety of corporate FDs is accredited by the ratings agencies such as CRISIL and ICRA.

Rates offered by some NBFCs

| NBFC | Return (in % on deposits for 24 months) |

| Mahindra finance | 6.2 |

| Bajaj Finance | 6.22 |

| Shriram T Finance | 6.75 |

(Note: Mahindra Finance’s return is for 30 months)

4. Fixed Deposits offered by Small Finance Banks: Even most small finance banks offer better returns on their fixed deposits in comparison to the rates offered by large banks. These include Jana, Ujjivan, Equitas and Suryoday.

| Bank | Percentage return on 1-year FD |

| Jana Small Finance Bank | 6.75 |

| Ujjivan Small Finance Bank | 6.5 |

| Equitas Small Finance Bank | 6 |