This Diwali season, banks and credit card companies are busy dishing out new cashback credit cards to entice customers looking for instant gratification. For example, Standard Chartered Bank’s famous Standard Chartered Super Value Titanium Credit Card offers five per cent cashback on fuel spending up to Rs. 2000 per month, Axis Bank has partnered with Samsung and Amazon.in and has announced an added five per cent cashback on all grab offers this festive season. The lure of cashback offers has encouraged many customers, especially, the new generation to rush for these cards.

While cashback offers do help to save money on online purchases, are they worth your consideration? You must know certain facts if you are looking forward to adding a cashback credit card to your wallet this Diwali season.

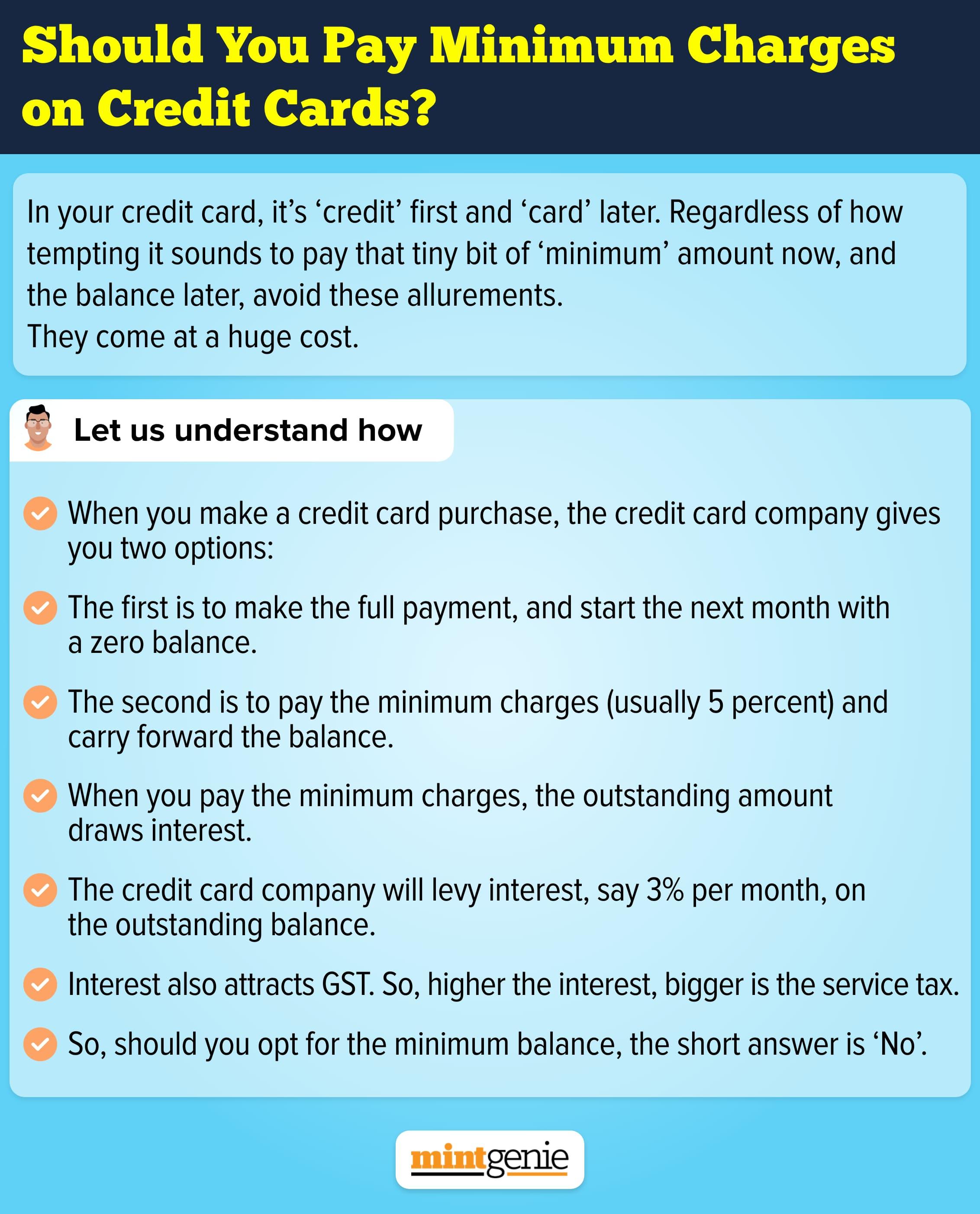

Do you really need to buy?

There is a thin line of difference between needs and wants. The unfortunate part during every purchase is that cashback offers encourage many people to buy things they can do without. The greed of receiving cashback offers causes many to transcend their budget without checking if the rewards on offer befit their needs. Offers score over utility causing many to overspend using their credit cards, thus, adding to their debt.

Ignoring regular credit card offers

All that glitters may not be gold, which means that you must check if these cashback credit cards are offering anything different from the regular ones. Some banks declare more festive offers on their regular credit cards instead of issuing new cashback cards.

There is no harm in applying for these cards. The problem is when you do not know why you are applying for them or succumbing to the glittery ads on these cards.

Tejas Ghongadi, a credit card enthusiast says, “Cashback cards as a type of credit cards are one of the easiest cards to use. You swipe your card, get a percentage back as cashback (either on card account or in some wallet) that can be used in subsequent transactions. The most important thing to check when applying for a cashback card is the usability of cashback:

- Cashbacks that come on the card account get offset against transactions in next billing cycle.

- Cashback that comes as credit in some wallet may have restrictions attached in utilisation.

- Cashback cards are a great way to start credit card usage journey for individuals with a stable income.” If you are not sure of how reward programmes work, it would serve you best to avoid taking these cards.

Also, look at the offers on the cards. Big banks and fintech companies offer big rewards that you may use to make necessary purchases. Small rewards mean that you have to spend more from your pocket to avail of some minuscule cashback, which may not serve your purpose.

Comparing credit card options

Many people reel under credit card debt. The quantum of credit card debt exceeds that of all other loans sought. This is because most people do not compare credit card options before applying. They forget to look into costs including joining fees, annual fees, late payment penalty, interest charges on late debt repayment, balance transfer fee, return payment fees and more.

There is no free lunch in this world stands true, especially, for credit card customers not willing to realize the hidden costs behind every reward they avail of. Before applying for a credit card, customers must go through a multitude of options that would help them identify the right card in sync with their needs and buying behaviour.

Where is the cashback credited?

Many people assume that the cashback amount would be credited to their cards, not realizing that some banks credit the amount to their online wallets. This restricts them to buying from some specific merchants only. Also, since the cashback amount is credited to the bank’s or merchant wallet, you cannot use the money returned to you. Some people tend to buy only to utilize the cashback amount, thus, adding to their purchase list. Customers must apply for only those credit cards wherein the cashback amount is credited back to their accounts. After all, what is the use of rushing for cashback offers that may not benefit you in the long run?

Affordability matters

Don’t buy something just because all others have it. Check if you can afford to incur and repay credit card debt. Check how that unwanted debt may affect your finances in the long run. The tendency to wave and swipe your cards without realizing that you have to repay the amount within the stipulated period makes rampant credit card use a dangerous game, to begin with. Missing your credit card payments can have a damning effect on your credit score, thus, mandating the need to consider the necessary pros and cons before applying for one.