There is a lot of heat surrounding passive investments such as Index Funds & ETFs. All prominent fund houses have been on overdrive with new index fund and ETF launches based on various indices ranging from broad market indices to factor-based ones and each one claiming how it is better than the existing options. This along with a lack of proper knowledge has added to the confusion regarding which index fund or ETF to choose, how to choose and why to opt for one over the other. Rahul Agarwal, Proprietor, Advent Financial in an interview with Abeer Ray of MintGenie regarding this burgeoning category of investment products.

Edited excerpts:

Q. Both ETFs and mutual funds are market-linked. Why should then people invest in ETFs when they can benefit from the fund manager’s experience by parking their money in diversified MFs?

Your question pertains to the active versus passive debate that has been going on for several years now and in my humble opinion will continue to, in the years ahead.

I think at the end of the day, it comes down to the conviction of the investor in the ability of the fund manager to deliver superior performance relative to the benchmark. Great if it works in the investor’s favour; not so great if it doesn't.

I am a staunch proponent of evidence-based investing and if one simply looks at the historical evidence that is out there, it would tilt the scales in favour of index investing via (ETFs) and Index Funds.

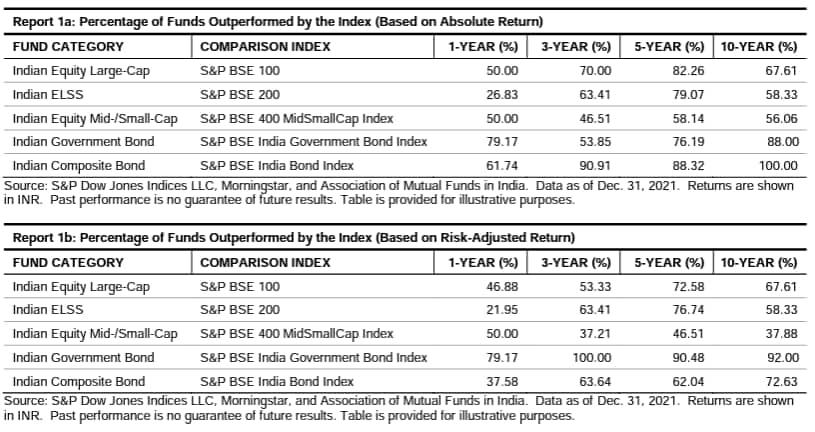

There is this report known as the SPIVA® scorecard which is published by S&P Global bi-annually, that measures the performance of actively managed funds against their corresponding benchmarks. I have been tracking this for more than five years and have been noticing a gradual yet steady decline in the number of actively managed funds which have done better than their corresponding index. The following table shows an extract from the last published SPIVA Scorecard which shows a very high percentage of actively managed funds that have failed to match up to the returns delivered by the index. Full report available here.

While in hindsight it is easy to understand who the winners were, i.e., the funds which delivered higher relative returns than their benchmark index but how does one know this is advance for sure especially considering the broad spread in fund returns between the first and third quartiles; this poses challenges and risks with fund selection. To use a cricketing analogy, it is similar to assuming that one knows which batsman is going to score a century and which one is not.

Therefore, the risk of fund selection from among a small percentage of funds that could potentially deliver index beating returns coupled with the higher management expenses typically associated with the actively managed funds, make a compelling case for investment in favour of investing via ETFs and Index Funds.

Q. Buying small amounts of ETFs on a continuous basis can incur charges including transaction charges, 18 per cent GST on transaction charges, SEBI charges and stamp duty. These charges are in addition to the expense ratio of the ETFs that you pay for. Is it worth the investment you make?

Unless the amounts are extremely small, say something like ₹500, I agree that the transaction charges could work out costly since most brokers typically charge a minimum brokerage of ₹10-20.

In such cases smaller investors could replicate the same underlying exposure offered by the ETF through index fund or a Fund of Funds (FOF) investing in the same ETF.

It is pertinent to note that all the above charges would be applicable to the fund as well as and when they transact. The only difference is that investors of the scheme incur these indirectly. Therefore, in both cases, i.e., in the case of an ETF and a fund, the charges mentioned by you are incurred directly or indirectly by the investor.

Q. ETFs are preferred for their diversification. Does it mean that they are not subject to volatility?

I don’t think diversification is the primary “preferred” benefit offered by ETFs because even within ETFs, there are Sector ETFs.

Regarding the second part of your question, volatility can be reduced through diversification of investment across different asset classes, i.e. debt, equity, gold, etc. But a portfolio made up entirely of equity stocks would be subject to price volatility depending on the prevailing market scenario and sentiment.

Q. ETFs are most often linked to a benchmarking index, which means that they are designed not to outperform that index. Is this not a big setback for investors looking to beat index returns in the long run?

I think I have answered this in the detailed answer to the first question.

As you rightly pointed out, ETFs typically track an underlying index and everything else remaining constant, they should mirror both the risk and return of the said underlying index.

Regarding your point about setback; it goes back to the point made earlier about one’s ability to pick the top quartile funds and the conviction to hold it undeterred by interim short-term underperformance and noise.

We have already seen earlier the low percentage of actively managed funds which have fared better than their benchmark index. Therefore, by including index funds and ETFs as a core part of one’s long term portfolio you are virtually ensuring yourself the market return.

Q. Not many investors are aware of how to avoid ETFs with high tracking errors. How would you advise your clients to check the tracking errors of ETFs before putting their money in them?

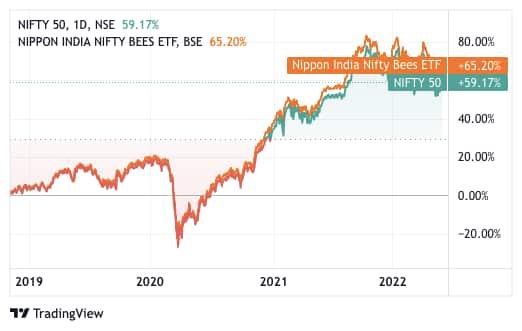

I think for an average investor, the easiest and simplest way to check would be to compare the returns of the benchmark index with the ETF returns based on the traded price. Almost all market-related websites and newspapers such as yourselves provide such tools. In the following example created using the MintGenie portal, I have compared the five-year returns of the NIFTY 50 Index with the Nippon India Niftybees ETF which tracks NIFTY 50. A limitation of this is that the available index is a price return index and not a total return index and therefore the dividend component is not included. If one were to approximate a dividend yield of ~1.25 per cent of Nifty for five years to the Nifty 50 return of 59.17 per cent, the resultant difference is not significant.

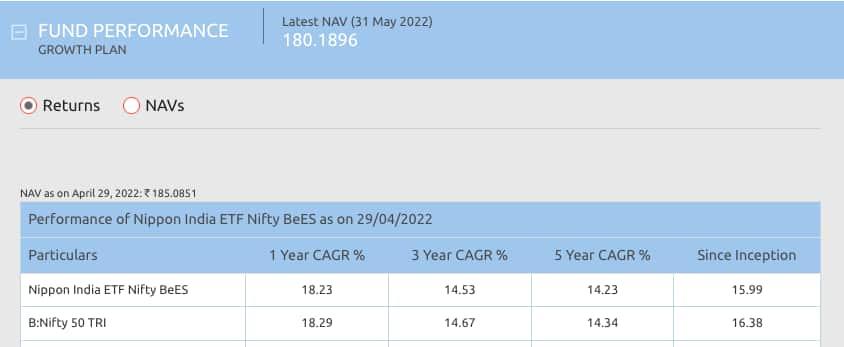

Another way to quickly compare the historical returns relative to the underlying index would be on the ETF website page itself. For instance, given below is a snapshot of the historical performance of Nippon India NIFTYBEES ETF which tracks NIFTY 50 from their website -link here

Without getting into the jargon and nitty-gritty, anyone can easily conclude that there isn't a significant difference in the ETF Returns from the benchmark returns.