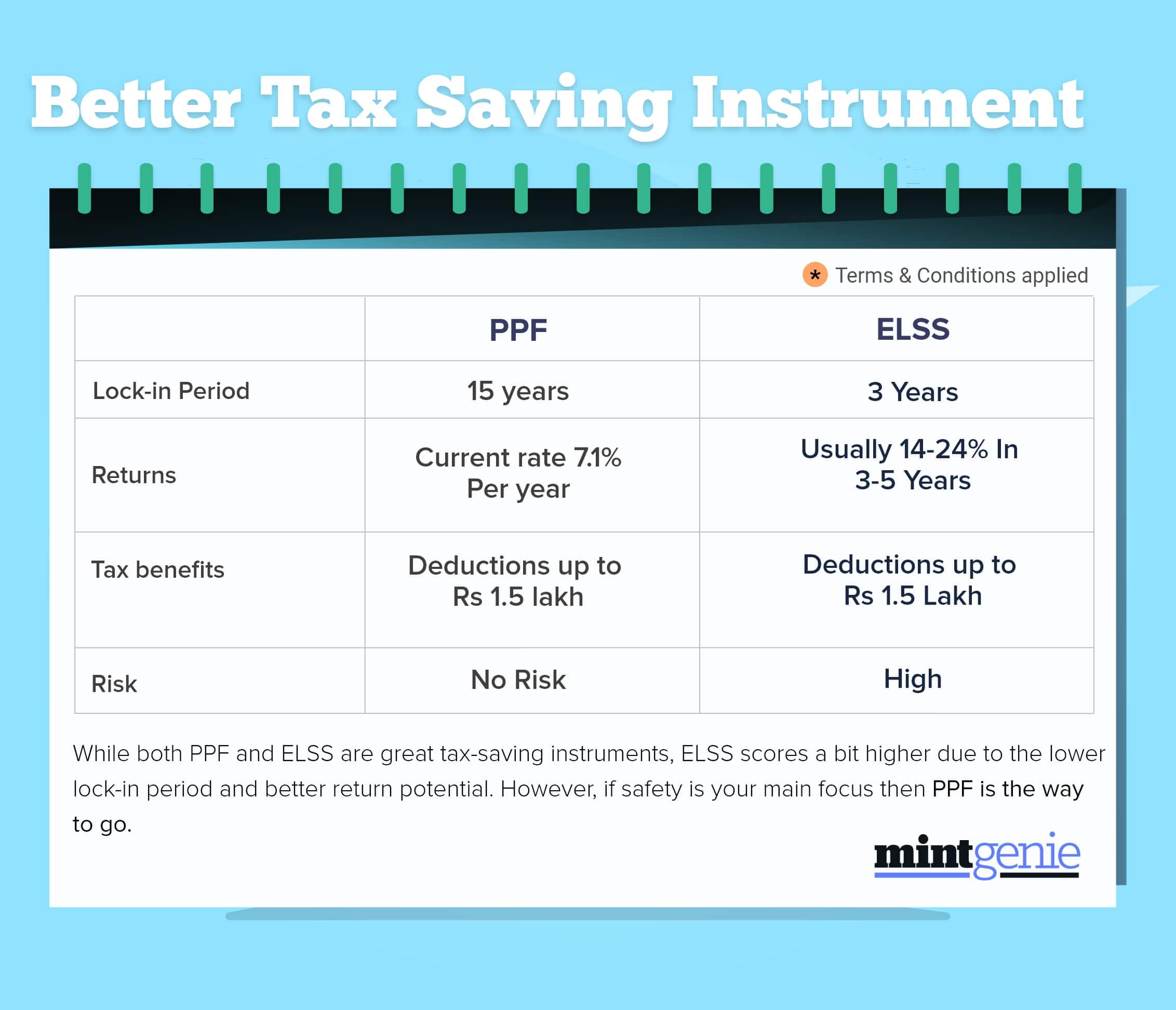

Better returns are always welcome, which is why investors look for ways to earn more on their investments. Salaried employees looking for risk-averse investment options to grow their money prefer government-sponsored schemes such as the Employees’ Provident Fund (EPF), Public Provident Fund (PPF), special savings schemes, and more. While the PPF lends exempt-exempt-exempt (EEE) benefits, the tax liability exists for only EPF investors belonging to a higher income group.

Benefiting from higher interest rate

While both are good, one may contribute a notch higher to Voluntary Provident Fund (VPF) for added benefits. Salaried employees can contribute more than 12 per cent of their Basic Pay + Dearness Allowance (DA) to their EPF accounts via VPF. There is no limit to the contribution employees can make. This means that employees may contribute the entire amount equivalent to their Basic Salary + DA. The interest rate on VPF contributions is the same as the interest rate on EPF contributions, which is 8.15 per cent, a lot higher than the 7.1 per cent promised to PPF investors.

The debate about investing in VPF versus PPF is not new, especially, as salaried employees also invest in tax-saving schemes such as PPF. Considering the stagnant 7.1 per cent interest rate, these investors find it difficult to decide whether to increase their VPF contribution or invest in schemes like PPF for tax savings and retirement planning.

A careful assessment of both investments reveals how the decision between increased VPF contributions and investing in PPF must be based on one’s financial goals and existing financial condition. This is because increasing your VPF payment may result in liquidity concerns, thus, affecting your budget as your monthly take-home pay would be considerably lower. Employees who invest in PPF for tax savings can consider increasing their VPF contributions than relying on PPF alone considering the higher interest rates in the former.

Assessing tax liability

Investors are concerned about tax liabilities, which is why they evaluate the validity of every investment accordingly. Contributions made to a VPF are tax deductible under Section 80C of the Income Tax Act, 1961. So, if your current EPF contribution is less than ₹1.5 lakhs per year and you are investing in PPF to make up the difference, you may benefit more from increasing your EPF contribution through the VPF route.

Is there a limit on VPF investment?

Contributions to a VPF account look good, though this does not mean that you can continue to put money into it, sans any limit on the investments made. Like most other government-sponsored schemes, there is a limit on the money you can put in your VPF account.

Investment in VPF means that you can invest only up to ₹2.5 lakhs every year without incurring any additional tax. Section 80C allows for a deduction of ₹1.5 lakh from this amount. However, before increasing your VPF contribution, you should review your current EPF and VPF contributions to ensure you are not exceeding the statutory limit of ₹2.5 lakhs per year.

There is no compulsion for anyone to invest in VPF. Since the tax benefits on both VPF and PPF are the same, you must decide how much money you would like to allocate to either any of these investment options or both of them depending on how you view your financial independence in the long run.