Many people are cheering this year’s Budget suggesting how reducing the income tax slabs will mitigate the complications in the tax assessment process. But did the Budget deliver on the personal finance front entirely?

Navneet Munot, MD & CEO, HDFC Asset Management Co Ltd, says, “Balancing the expectations of an aspirational country like ours with fiscal prudence is no mean task. The first budget of ‘Amritkaal’ did a fine job of balancing the two, especially against a challenging global backdrop. This budget builds upon the reforms initiated over the past few years with a focus on improving India’s growth potential and quality of life. Continued focus on capex, job creation and special mention of financial sector reforms are encouraging. Now with the event behind us, markets’ focus shifts back to global cues, monetary policy and incoming data points.”

Like the previous budgets, there surely have been some hits as well as misses that people are now talking about. Some people are fawning over the new schemes introduced while lauding the government for simplifying the income tax rules. Others, however, mention what more could have been done to ease the financial woes of the common man.

Lower taxes, more savings

Does the Budget really serve India’s “Aam Aadmi” or is there more to it than meets the eye? Elaborating on what grounds the Budget will encourage people to save more, Dev Ashish, Founder, Stable Investor, says, “The Budget has some good news for senior citizens. The doubling of the SCSS limit to ₹30 lakh and that of the POMIS to ₹9 lakh ( ₹15 lakh for joint accounts) is a welcome move. More so because there is still no announcement for the extension of the PMVVY scheme beyond March 2023. So, with the current increase in limits, a retired couple together now has the option of parking a total of ₹75 lakh ( ₹60 lakh in SCSS & ₹15 lakh in POMIS) if they want to stick to sovereign-backed schemes for their income needs.”

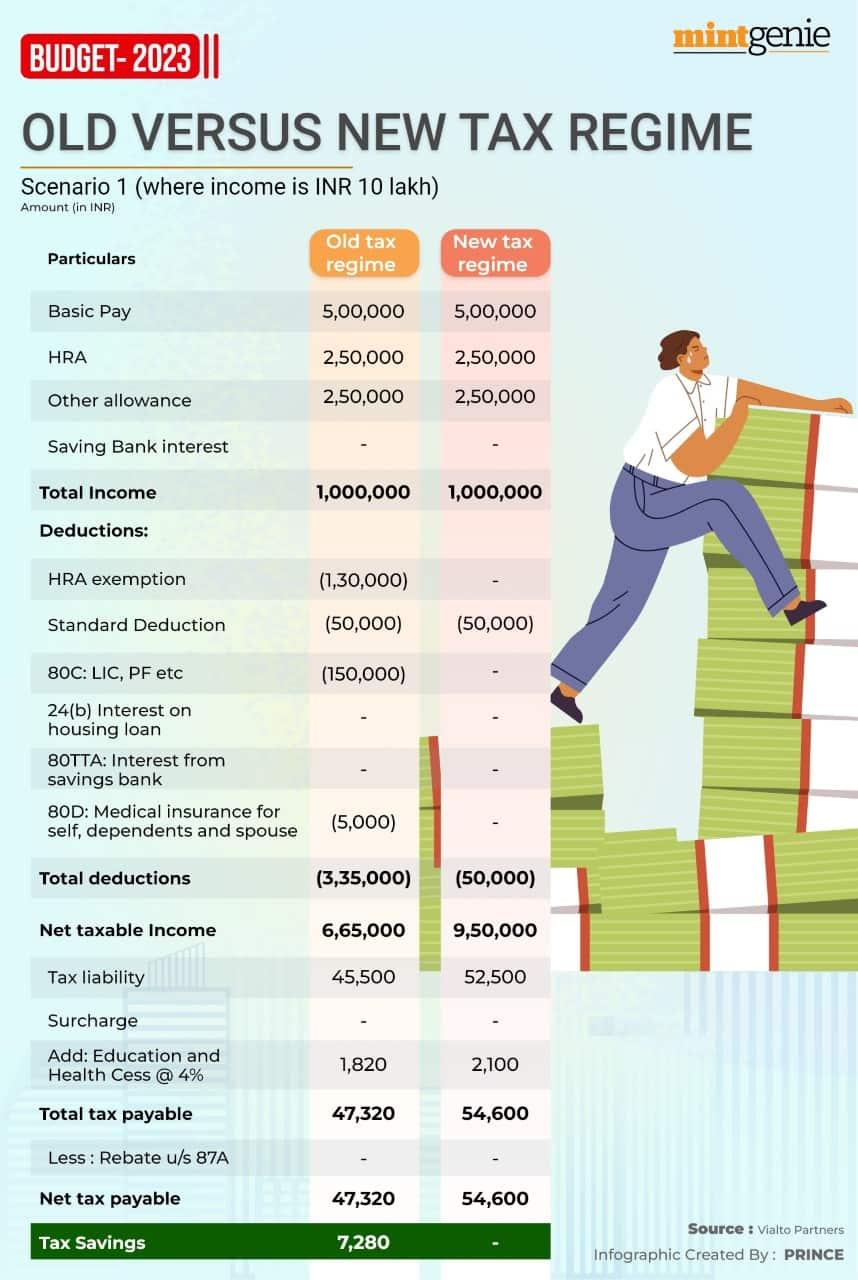

This year’s budget took the first step in simplifying income tax rules. The income tax slabs have been reduced to six. The exemption limit has gone up, leaving more money in the hands of taxpayers. The decision to not tax income up to ₹7 lakh (under this year’s tax regime) means taxpayers will now find more money in their hands. The middle-income taxpayers have a lot to look forward to considering how their earnings were earlier taxed under both the old and new tax regimes.

The Budget has also decreased the maximum surcharge rate applicable to HNIs from 37 per cent to 25 per cent, thus, bringing the overall effective tax rate from 42 per cent to 39 per cent.

Ashish describes it as a well-intended move to encourage people to now calculate their taxes under the new regime. He adds, “With the new change to make the new tax system more attractive and also that no changes have been announced for the old one and no increase in Section 80C deductions, it is very clear that over the next few years, the government intends to make the switch to the new tax scheme without exemptions.”

However, CA Kanan Bahl, a Finance Educator and Growth Consultant, warns taxpayers from jumping the gun without accounting for what would serve them better. There is more to tax assessment than the mere income tax slab rates, deductions and exemptions. Bahl emphasizes, “The new tax regime should not be a blind choice. You might end up paying higher taxes. The new vs old choice should be well thought out and calculated. You may choose for professional help also as the provisions are not so simple to understand.”

One good thing that the budget did is to ensure that more money remains in the hands of taxpayers. Take, for example, leave encashment that was exempt only up to ₹3 lakh to date. The limit has now gone up to ₹25 lakhs which would benefit the retirees who till now had to pay tax on a major chunk of the leave encashment payout. The new rule citing a greater exemption limit will help soon-to-retire employees get more dispensable income in their hands and compensate for the current high inflation rate to some extent.

While a higher cash exemption limit translates to more money in the salaried people’s bank accounts, the greed to have more may take a toll on one's mental health. After all, what use is money if it destroys your health?

Like Ashish says, “While govt. employees may be tempted to continue accumulating leaves in the hope of getting higher encashments (due to an increase in the tax-free limit to ₹25 lakh from earlier ₹3 lakh), people also need to think about balancing work with life. Taking leaves is good and the decision should not just be governed by money-maximization factors. Balancing work and life by taking periodic leaves to enjoy time out, during earlier years (when younger) is better than just focusing on trying to have more money later in life (when older) when you would have decades in front of you post-retirement but maybe not the health and energy to use those times.”

Saurrav Sood, Practice Leader – International Tax & Transfer Pricing, SW India shares, “With such proposed amendments, it can be said that bringing liquidity back to the market is a prime focus of the Government which they want to achieve through this Budget and one can say that it does not take the money from the individuals by way of any additional taxes but is aiming to give some easiness through increase disposable income.”

This year’s Budget also took another step towards financially empowering women by announcing the new Mahila Samman Savings Certificate that allows women to earn 7.5 per cent interest on a deposit of ₹2 lakh for two years.

Missing out on capital gains’ definition and taxation

The disparity in the tax treatment of the sale of debt mutual funds and equity mutual funds continues. While LTCG on equity is subject to a 10 percent tax when held for more than 12 months, in the case of debt mutual funds units’ sale, LTCG tax is levied at 20 per cent when the units are sold after more than 36 months.

No respite on LTCG tax

Those putting their money in stocks and mutual funds rue how the country’s finance minister ignored their pleas concerning capital gains definition and rationalising the long-term capital gains (LTCG) tax on equities to make it homogenous across asset classes including debt and property.

Ashish adds, “The Budget this time was silent on taxation of LTCG and STCG from equities and in general on the existing clutter of different capital gains definitions for different assets. While people wished for reduction/removal of LTCG, it might not be wrong to say that no news is still good news (for the time being) as the government may eventually decide to tweak the capital gains structure in the coming years.”

Gaurav Rastogi, CEO & Founder, Kuvera.in, says, “The big miss in this budget is the standardisation of short-term and long-term capital gains across all asset classes. Just like the Finance Minister understands that income tax saving should not be the driving reason to mobilise investment accounts, similarly capital gains arbitrage should not be the reason for people to choose one asset over the other. All risk assets should have the same capital gains obligation.”

Big life insurance proceeds to be taxed

Relying on high-value insurance policies as a tax planning measure will not help as this year’s budget prunes down the huge life insurance proceeds by subjecting them to tax. The budget clearly states that only the income from life insurance policies with an aggregate premium of up to ₹5 lakh will be exempt from taxation. The proposal to limit the income tax exemption comes as many people are fooled into buying innumerable insurance policies after being lured into tax benefits. While it may cause a temporary slump in the sales of life insurance plans, investors will feel more encouraged to invest their money into diverse investment opportunities that allow them to earn high returns while helping them save on the tax component too.

Tarun Chugh, MD & CEO, Bajaj Allianz Life Insurance, says, “The budget announced that for non-ULIP (traditional) insurance policies issued from the new fiscal year, income from only those policies with aggregate premium up to ₹5 lakh shall be exempt. This is a bit of a dampener for the insurance industry and for increasing the penetration of insurance and household financial savings in India. India still has quite low insurance penetration and there is a need to provide measures and incentives to boost that in the coming years. Also, household financial savings have been falling in India and insurance is a critical component of that. Household financial savings (as a percentage of GDP) has fallen from 8.1 per cent in FY20 to ~6.5 per cent in FY23 (as per estimates). Discontinuing incentives on insurance plans should put further pressure on household financial savings to some extent."

No budget can ever satisfy all. “To each, his own” is the adage that aptly describes people’s views on this year’s budget as taxpayers list its positives and negatives hoping that the hits delivered this year would continue while the misses would be taken care of in the coming year.