Imagine a scenario when you lend money to someone, and instead of being given interest for it, you are charged one. This is what happens in case of a negative interest rate.

The interest rate offered by banks and other financial institutions on fixed deposits is supposed to grow your savings. But did you factor in inflation in it?

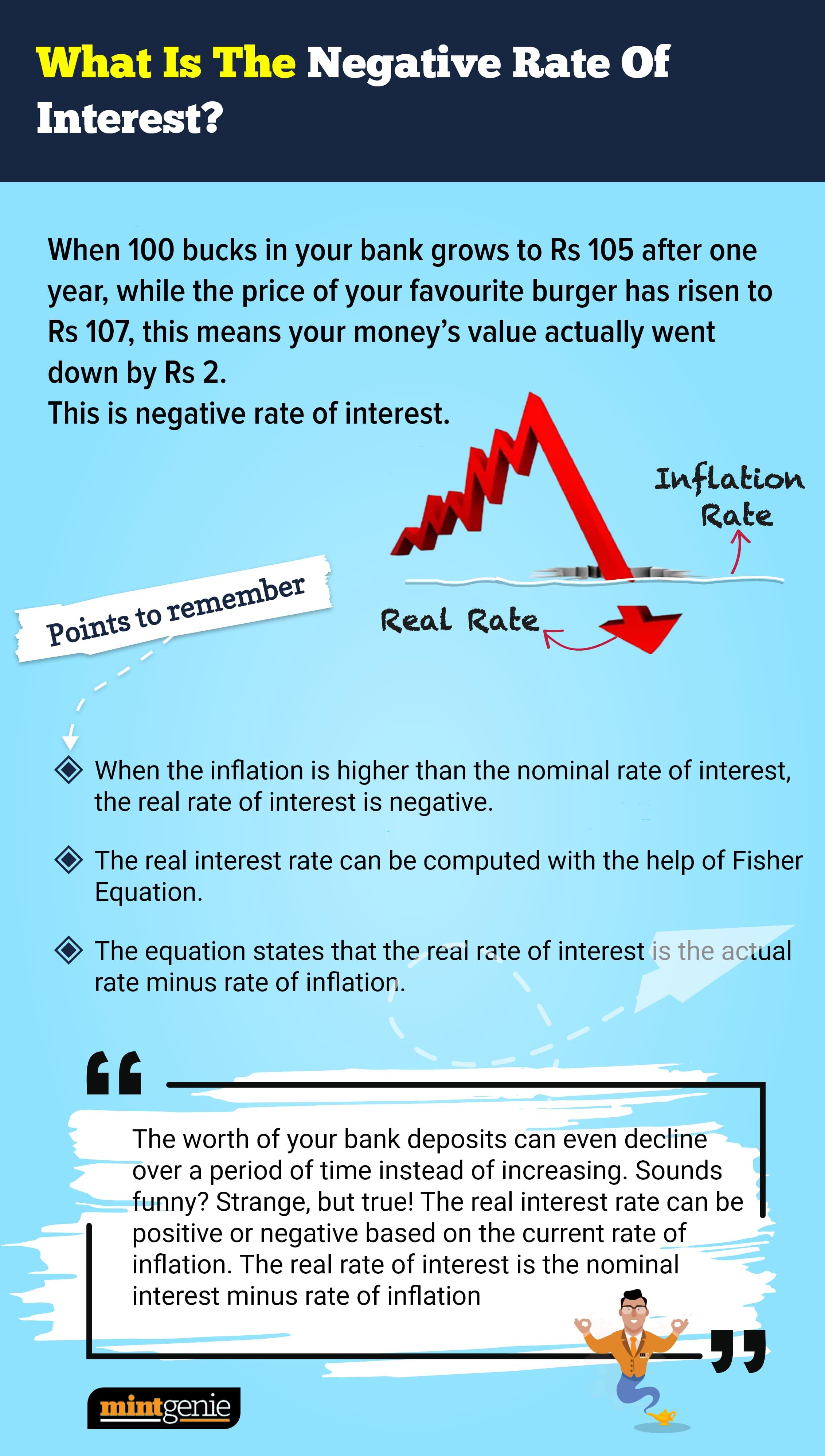

If you did, the remainder of interest after deducting inflation is known as the real interest rate.

The real interest rate can be positive or negative based on the prevailing rate of inflation. It is computed by Fisher Equation which states that the real interest rate is nominal interest minus inflation rate.

In other words, the real rate of interest is the actual rate minus prevailing rate of inflation.

When inflation is more than FD interest?

The Reserve Bank of India (RBI) on October 8 projected the rate of inflation in FY 2022 to be 5.3 percent. And as we know that the FD interest rates by most commercial banks are less than this.

For instance, HDFC Bank is currently offering 4.9 percent interest per annum on its one-year fixed deposits (FDs) while SBI offers 5 percent. In both the cases, the depositors would earn a negative rate of interest.

This means, those who have made a one-year deposit in HDFC Bank would get a negative rate of interest of 0.4 percent. Since the interest paid on FD is taxable, this real rate of interest would turn out to be even lower than 0.4 percent.

Let us understand this with the help of another illustration.

For example, Mr A gives a loan of ₹10,000 to Mr B for one year at a rate of 10 percent. At the end of one year, he stands to receive ₹11,000.

On the face of it, it appears that ‘A’ earned 10 percent from the loan he gave to ‘B’. But the real interest rate can be lower based on the prevailing inflation. Let us suppose the rate of inflation was 18 percent during this year, then A actually suffered a loss of 8 percent in his purchasing power.

How does it impact depositors?

It is advised that unless the real interest is positive, it is not rational to postpone a purchase. For instance, when a microwave costs ₹10,000 and inflation is 10 percent then the same microwave would be available for ₹11,000 a year later, while the same amount in bank would not grow to become ₹11,000.

The negative rate of interest effectively reduces your purchasing power.

Since interest rates currently are at record low, and importantly, they are lower than the projected inflation -- the interest rates are negative.

To battle with inflation and to earn a positive interest rate, one can explore inflation-indexed bonds wherein the coupon and principal rises in alignment with the rate of inflation. This means the interest rate is similar to the real rate of interest.

So, we can highlight that interest rate is the cost of borrowing which means borrowers pay lenders a cost for the loan. When the interest rate is negative, this means the cost of borrowing is negative. In other words, borrowers are being given an interest for borrowing money, instead of lenders.