“Innovation is taking two things that exist and putting them together in a new way.” – Tom Freston

In financial markets. We see new & innovative products coming up every now & then trying to replace the traditional products. These new products either offer better returns or lower risk. In the case of fixed income products, the most traditional & widely invested product is fixed deposit.

However, in the recent past, a lot of innovation has been coming along in fixed income avenues too. Some of these products are available only to institutional investors with large ticket sizes to invest in. In this post we are going to talk about securitized debt.

Securitizing refers to creating a debt product by pooling/collecting various types of loans under one bucket and issuing bonds/certificates against these loans.

These certificates have fixed income like features and risks.

Let us try to understand how they work:

There are 2 types of such products: Asset-Backed Securities (ABS) & Mortgage-Backed Securities (MBS). In case of ABS, the underlying assets are personal loans, auto loans, etc usually with a lower ticket size. With MBS, the underlying are home loans or commercial property loans.

Let’s simplify this with help of an example:

Suppose ABC bank has 20 home loan customers with an average ticket size of Rs. 20 lakhs each. This can be converted into a pool of Rs. 4 crores against which the certificates can be issued to investors.

The investors in our case are mutual funds that invest in such instruments. Suppose XYZ Mutual Fund bought the certificates of this pool by paying Rs. 4 crores along with a small fee to ABC Bank.

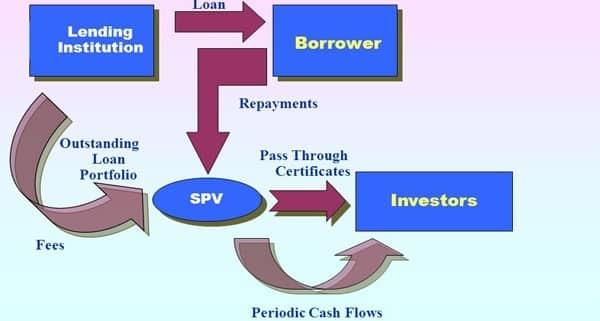

Once these certificates are purchased, all the interests and principal repayments collected by the Bank are transferred to the mutual fund. But this is not done directly. To make the process smooth, a separate entity is formed known as SPV (Special Purpose Vehicle) usually as a Trust.

So XYZ MF gives Rs. 4 crores to this SPV and then the SPV pays the same to ABC Bank. Once this transaction is done, all the proceeds from underlying loans are transferred by the bank to this SPV and SPV transfers the same to XYZ MF.

Here is a simplified diagram of the entire process

Looks simple right?

Well, wait!

There are risks involved in these instruments too.

Just like any other debt instrument, these PTC's also carry certain risks.

Let’s understand the risks involved:

Prepayment Risk: If the borrower makes early payment then it could be a challenge for XYZ MF to reinvest the same at similar or higher interest rates.

Interest Rate Risk: Especially in the case of home loans, if the interest rates go down, the borrower might refinance the loan at a lower rate and this could lead to lower interest income for XYZ MF.

Credit Risk: The risk of the borrower defaulting on repayment of principal and interest could lead to loss and therefore fall in the NAV of the scheme ultimately leading to the loss for investors.

However, these risks are mitigated by XYZ MF by using a feature called Credit Enhancement.

Credit enhancement can be provided by the originator (ABC Bank) in the following ways:

Overcollateralization: Issuing the certificates of lesser value than the value of underlying loans. Eg: Issuing PTC's worth Rs. 3 crores against the above underlying amount of Rs. 4 crores (This automatically gives a cushion against small defaults)

Subordinate/Senior tranche: Issuing PTC of a different class eg: Senior PTC's (Priority certificates) So that they can have priority in case of repayments and the remaining junior tranches (high risk) can get payment after senior PTC's are paid.

The issuance of securitized debt is governed by RBI. Few measures are proposed to enhance the safety of such debt:

- The originator (ABC Bank) has to hold such a pool of loans for at least 9 to 12 months before they can be securitized.

- The originator has to retain a certain minimum % of such a pool of loans with itself. This could be around 5-10% of the book value of loans.

A major component of the Indian debt market is Government Securities (G-Secs). Over the period of time, there have been new products & innovative products coming into debt markets like ZCB's, floating rate bonds, and corporate bonds.

In case of corporate bonds, they are backed by a single issuer & the bond becomes worthless if the issuer defaults. Securitized debt offers a basket of small ticket loans in a single package where the loans forming part of the package are scattered across products, geographies.

A default by a single auto loan out the entire basket won't make the bond/PTC worthless hence makes it better in terms of risk.

Most of the schemes of MF houses have the mandate to invest in securitized debt as per their scheme information documents. However, whether such instruments will gain the attraction of mutual funds in coming times is yet to be seen.

CA Rohit J. Gyanchandani is Managing Director, Nandi Nivesh Private Limited, A Pune based Wealth Management Company.

Follow the entire series here.