Q. I am a 25-year-old working woman. My annual income is around ₹7 lakhs, and my current investment value is around ₹9 lakhs. How will the latest union budget help me save tax?

For personal income tax there are many changes that the Finance minister has proposed.

On salary or income tax

All changes proposed in the Union budget are under the new tax regime. Old tax regime remains as is with no changes. Following are the changes proposed in new tax regime:

- The new tax regime under section 115 BAC is declared as the “Default Tax Regime”, however, you can still opt for the old regime.

- Tax exemption limit is increased from Rs. 2.5 Lakhs to Rs. 3 Lakhs in new tax regime.

- The threshold limit of the tax rebate is increased from maximum income limit of Rs. 5 Lakhs to Rs. 7 Lakhs.

- Standard deduction of Rs. 50,000 is also being introduced in the New Tax Regime.

- Highest rate of surcharge is reduced from 37% to 25%.

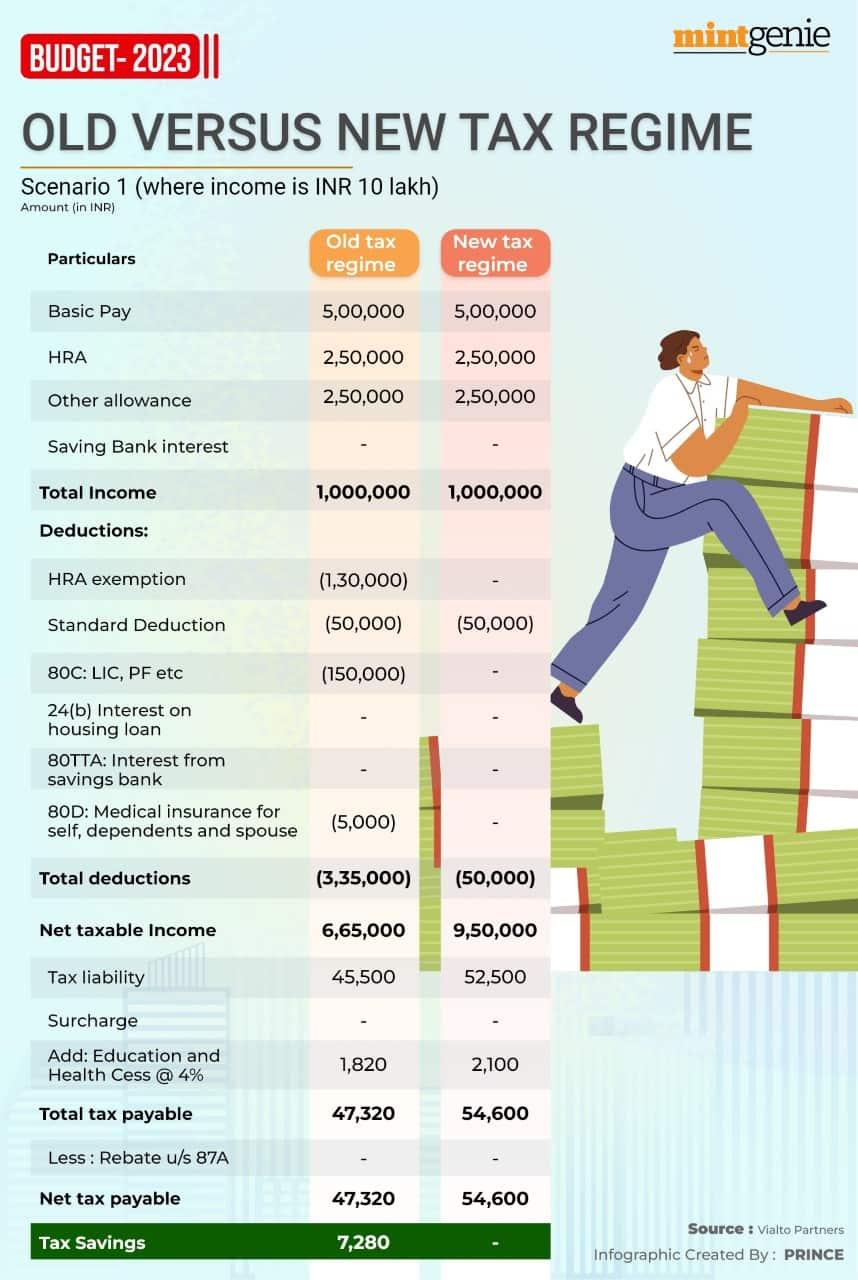

Following are the different tax slabs for old and new tax regime:

| Old Tax Regime | New Tax Regime | ||

| Income Slabs | Tax Rates | Income Slabs | Tax Rates |

| 0 to 2,50,000 | Nil | 0 to 3,00,000 | Nil |

| 2,50,001 to 5,00,000 | 5% | 3,00,001 to 6,00,000 | 5% |

| 5,00,001 to 10,00,000 | 20% | 6,00,001 to 9,00,000 | 10% |

| 10,00,001 & Above | 30% | 9,00,001 to 12,00,000 | 15% |

| 12,00,001 to 15,00,000 | 20% | ||

| 15,00,000 & Above | 30% | ||

Now since your total annual income is Rs. 7 Lakhs, assuming this to be your total taxable income, this is how your tax would be calculated under new regime:

| Particulars | Amount | Amount |

| Gross Income | 7,00,000 | |

| Standard Deduction | 50,000 | |

| Net taxable income | 6,50,000 | |

| 0 to 3 Lakhs | Nil | |

| 3 Lakhs to 6 Lakhs (5%) | 15,000 | |

| 6 Lakhs to 6.50 Lakhs (10%) | 5,000 | 20,000 |

| Rebate | 20,000 | |

| Total tax Payable | Nil |

Old Regime

| Particulars | Amount | Amount |

| Gross Income | 7,00,000 | |

| Standard Deduction | 50,000 | |

| Net taxable income | 6,50,000 | |

| 0 to 2.5 Lakhs | Nil | |

| 2.5 Lakhs to 5 Lakhs (5%) | 12,500 | |

| 5 Lakhs to 6.5 Lakhs (20%) | 30,000 | 42,500 |

| Total tax Payable | 42,500 |

No Tax Rebate will be eligible under the old tax regime if the Total Income is more than Rs. 5 Lakhs.

If we assume that you are availing the benefits of following deductions and exemptions:

- You have a life insurance policy for which you are paying the premium, you invest in Employee Provident Fund through your employer, and you invest in Public Provident Fund and Equity Linked Savings Schemes (ELSS) of Mutual Funds total of which approximately is Rs. 1.5 Lakhs, you get the benefit of deduction under Section 80C unto Rs. 1.5 Lakhs. Means that amount gets deducted from your Gross total income.

- You invest in the National Pension Scheme annually Rs. 50,000, you can get the deduction up to Rs. 50,000 under Section 80CCD.

- You have a health insurance towards which you are paying the premium of approximately Rs. 25,000, you get the benefit of deduction under Section 80D up to Rs. 25,000.

Then your income tax calculation under old regime will be as below:

| Particulars | Amount | Amount |

| Gross Income | 7,00,000 | |

| Standard Deduction | 50,000 | |

| 6,50,000 | ||

| (-) Deduction under Sec 80 C | 1,50,000 | |

| (-) Deduction under Sec 80 CCD | 50,000 | |

| (-) Deduction under Sec 80 D | 25,000 | 2,25,000 |

| Net Taxable Income | 4,25,000 | |

| 0 to 2.5 Lakhs | Nil | |

| 2.5 Lakhs to 4.25 Lakhs (5%) | 8,750 | 8,750 |

| Rebate | 8,750 | |

| Total tax Payable | NIL |

Note - *Cess of 4% to be added.

So to conclude, we can say that the new tax regime is better if you do not have any investments under 80C or 80D, no House Rent Allowance or any other exemptions, no loan home loan (list is not exhaustive). But in case you have the above investments or exemptions, the old tax regime can help you save on tax better.

Taxes on Investments

For your investment of Rs. 9 Lakhs, there is no change on capital gains from selling of equity or debt investments in the new tax regime, so whenever you sell the investment, following would be the effect:

If you hold equity investments

- You sell it within a year: If you sell your equity investments within a year, you will incur short term capital gains tax, which is taxed at 15% plus cess and surcharge.

- You sell it after a year: If you sell your equity investments after completion of a year, you will incur long term capital gains tax, which is exempt upto Rs. 1 Lakhs and beyond Rs. 1 Lakhs it would be taxed at 10% plus cess and surcharge. In long term capital gains tax, you also have a benefit of indexation, which means the cost of purchase is increased with the rate of Inflation (CII) which leads to decrease in gains calculated and hence less tax.

If you hold debt investments

- You sell it within 3 years: If you sell your debt investments within 3 years than you incur short term capital gains tax, which will be taxed as per your tax slab rates depending on which regime you would have chosen (old or new regime)

- You sell it after 3 years: If you sell your debt investments after 3 years then you incur long term capital gains tax, which will be taxed at 20% plus cess and surcharge with indexation benefit.

International Money Matters Pvt Ltd is a 20-year-old SEBI registered financial planning-cum-investment advisory boutique. Please click here to find out more.