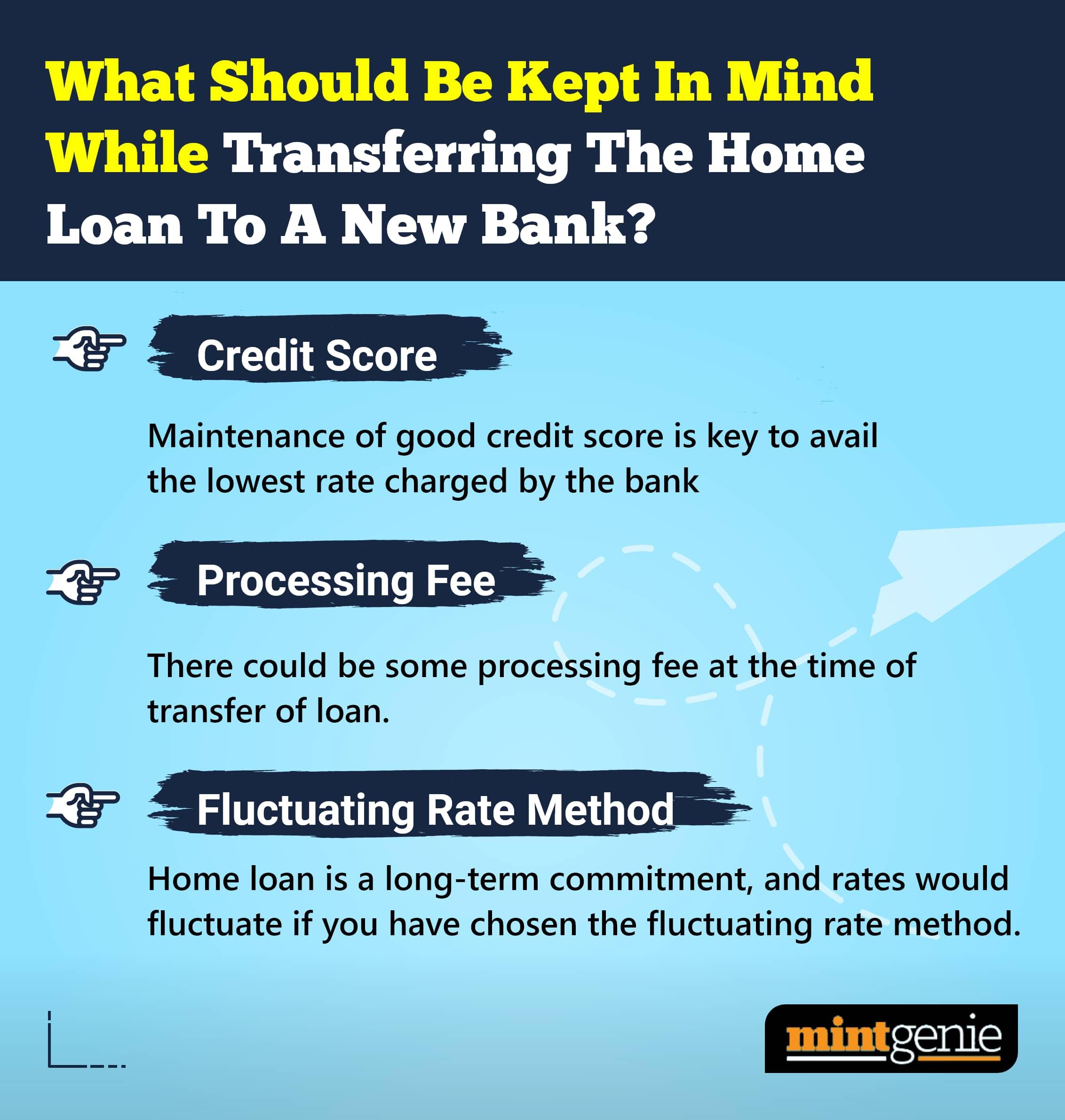

Q. I am 40, working as an engineer. I have a wife and 2 children. My wife and I earn around ₹4 lakhs a month. I have savings of about ₹50 lakhs sitting idle in my account. I have a mortgage with variable interest rate on my house with ₹80 lakhs to be repaid over the next 10 years. I have no other debt. Should I use my savings to prepay my loan? Or should I invest that amount somewhere else?

The 50 lakhs saved in the bank account is neither earning any tax-efficient returns nor beating inflation in the long run. It is best to redeploy the idle money in investments as per your requirements.

First, identify all your short-term goals for the next 3 to 5 years. Evaluate if you have enough corpus available to take care of these requirements .

Once you have planned how to fund these near-term requirements and other critical goals such as children’s education and your retirement, then you can decide on using your idle savings to either foreclose your loan or to build a well-diversified investment portfolio. Please consider the following factors to help you decide.

Compare interest rates: Compare the current interest rate on your home loan with expected returns on your investment portfolio. If the interest rate on the loan is higher than the returns from your investments, it makes sense to pay off your home loan first.

Clear other liabilities: If you have other high-interest debts, such as credit card debt or a personal loan with an interest rate higher than that charged by the home loan, you should clear those loans before investing.

Consider tax benefits: A home loan gives you tax benefits. Presently, under section 80C of the Income-tax Act, you can claim principal amount paid up to a limit of ₹1.5 lakhs per annum and interest paid (under Sec 24) up to ₹2 lakhs per annum. If it is a joint property, then each owner can claim these amounts. So, foreclosing the home loan may increase your tax liability. You must factor this in before you decide on prepaying the loan.

Create emergency fund: It is important to have an emergency fund in place before investing. Ideally, you should set aside an amount sufficient to meet your current expenses for 3 to 6 months. If you don't have enough savings to cover unexpected expenses, you should prioritise creating an emergency fund before you invest.

Know your risk tolerance: Investing always carries some level of risk. If you are risk-averse, you may prefer to pay off your home loan and be debt-free.

Step up EMI: If the loan interest is likely to go up, you can increase your equated monthly instalment (EMI) amount. You may also make partial lump sum repayments. This will reduce the interest cost and the tenure of the loan.

Consult a financial advisor who can provide personalised advice based on your specific circumstances and preferences.

International Money Matters Pvt Ltd is a 20-year-old SEBI registered financial planning-cum-investment advisory boutique. Please click here to find out more.