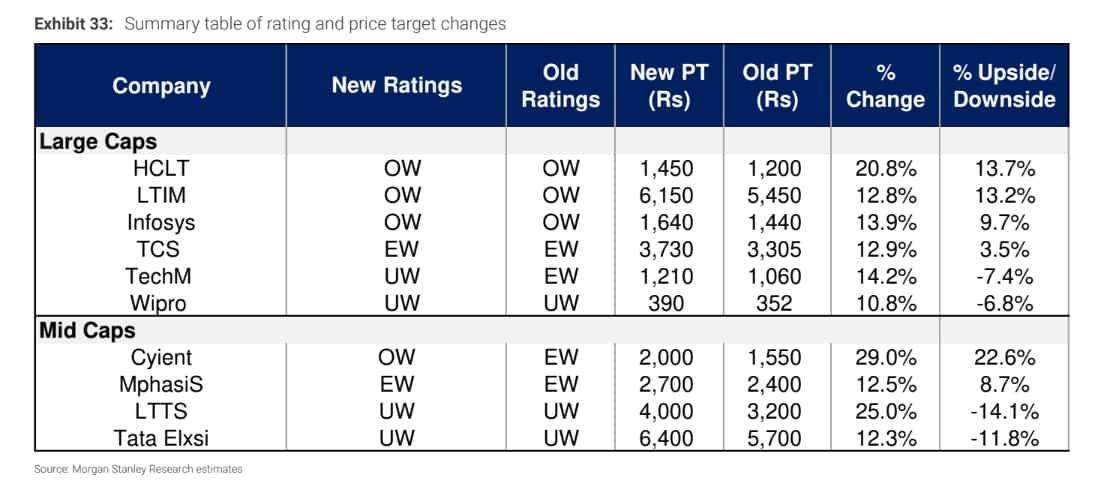

Despite the recent outperformance by the IT space, brokerages seem to be at crossheads when it comes to the sector. In a recent note, brokerage house Morgan Stanley has raised price targets for certain large-and mid-cap IT stocks by up to 29 percent driven by earnings improvement and optimism about growth and margin estimates for 2024-25.

However, another brokerage Nirmal Bang expects the contrary. It has ‘sell’ calls on all, except 1 (Tech Mahindra) IT stock under its coverage. It remains ‘underweight’ on the Indian IT space and has also cut FY25 estimates for this space.

"We believe the market is taking the view that the worst is over and that revenue/earnings will accelerate sharply in FY25. We have a non-consensus view that FY25 growth is going to be only a tad faster than FY24 with risks that it could be as bad or weaker. While the US macro has surprised positively in 2023 so far, deterioration is likely ahead in 2024. Demand is likely to be slower for longer," explained Nirmal Bang.

Morgan Stanley on IT

The brokerage has raised target prices for TCS, Infosys and HCL Tech. Meanwhile, it has largely maintained favourable ratings for the remaining IT stocks under its coverage.

“We have revised our price targets up by 11-29 percent, led by roll forward, lower probability of bear case, and higher probability of bull case, and increased long-term earnings. We have raised our margin assumptions for ER&D names, while our revenue growth assumptions remain largely unchanged, except for Wipro and Mphasis (numbers lowered),” the firm said in a note.

Its top picks in the sector are HCL Technologies, LTIMindtree, Infosys, and Cyient.

Morgan Stanley believes that a strong outlook on FY25 revenue growth, improving margins, and double-digit EPS growth should keep valuations afloat. It expects the current P/E valuation, similar to the 5-year average, to persist due to projected double-digit EPS growth in FY25 and relatively low ownership by both domestic and foreign institutional investors, although ownership is gradually increasing.

It further noted that along with the stabilisation of macroeconomic risks, the conversion of pipeline projects into the order book (evidenced by numerous significant deal announcements) and commentary on the discretionary spending environment, though weak, not deteriorating further, point towards improved growth trends.

Also, margins have more tailwinds in FY25, including falling attrition rates, suboptimal utilisation rates, room to improve the employee pyramid, and operating leverage, added the brokerage.

Morgan Stanley attributed the optimistic revenue growth forecasts for FY25 to stabilising macro risks, the leveling off of hyper-scale revenue growth, an anticipated rebound in BFSI (banking, financial services and insurance) spending in CY24, announcements of significant deal wins and robust order bookings in the second quarter of FY24.

Stocks

Within largecaps, employee and subcontracting costs as a percentage of revenues have the biggest room for improvement for HCLTech and Tata Consultancy Services (TCS), it said.

Regarding individual stocks, Morgan Stanley has retained an ‘overweight’ rating on HCLTech, LTIMindtree, and Infosys within the largecap segment but maintained ‘underweight’ call on Wipro, L&T Tech and Tata Elxsi.

Meanwhile, it has upgraded Cyient (within ER&D services) to ‘overweight’ due to increased earnings and higher multiples, with the revenue growth cycle remaining strong.

However, it has downgraded Tech Mahindra from "equal weight" to "underweight", saying the period of strong outperformance has ended and over concerns about potential downward pressure on EPS.

"Within large caps, we like HCLT (mid-single-digit revenue growth in F24e with a resilient margin profile), followed by LTIM (room to surprise in 2H on both growth and margins) and Infosys (healthy order book to support F25 outlook). We maintain our EW on TCS and Mphasis, owing to valuations. We downgrade Tech M to UW, as strong outperformance is behind us and we see potential downside risk to EPS. We upgrade CYL to OW, owing to EPS upgrades, led by resilient margins and low expectations on revenue growth. We maintain our UW on Tata Elxsi, LTTS and Wipro," it said.

Contrary opinion

While Nirmal Bang has a SELL recommendation on most IT stocks in its coverage, it has upgraded Tech Mahindra to ‘Accumulate’ as it believes margin expansion in FY26 may surprise on the upside under a new management.

"While TML will see continued weakness in revenue and margins in the remaining quarters of FY24, it will also be impacted by the shallow US recession we are expecting in 2024. From the current extremely low levels, we believe that its EBIT margin could expand a lot faster than current consensus expectations. From 10.2 percent EBIT margin in FY24E, we are expecting the same to expand to 15.4 percent in FY26. We do not think this by any means is an aggressive target as this was already achieved in FY19. For FY24, we have raised our EBIT margin estimate by 60bps. For FY25, as has been the case with other companies under our coverage, we have cut our USD revenue estimate by ~300bps while raising our EBIT margin estimate by 30bps. It is for FY26 that we have raised our EBIT margin estimate substantially by 210bps to 15.4% while keeping USD revenue constant," it explained.

The brokerage noted that while the IT sector has seen PE multiple expansion (especially for Tier-2) in the last 6/12 months, there have been no meaningful earnings upgrades. Further, post two successive quarters of weak results (in aggregate), it believes that Q2FY24 and Q3FY24 may see QoQ growth for its coverage universe, but the next couple of quarters’ performance will not herald the beginning of a sustained pick-up.

On margins as well, the brokerage disagrees with the consensus that they will improve over FY24-FY26. The mega deals are fiercely competed (‘priced to win’) and are dilutive not only in initial years but are dependent on the extraction of significant productivity gains and operational efficiencies, where companies may fall short, it noted.

The brokerage expects that the big pent-up demand-driven spike will be in FY26 and not in FY25. Hence, the expectation of double-digit growth in FY26 for Tier-1. Post that spike, it estimates that Tier-1 players will likely settle into a 7-8 percent CAGR for the foreseeable future.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie. We advise investors to check with certified experts before taking any investment decisions.