Shares of HDFC Bank gained 1.5 percent on Monday, in line with the overall positive sentiment in the market as well as the banking index. The Nifty Bank has advanced nearly 1 percent in today's deals.

While India's largest private sector lender has given pretty muted returns in the current calendar year 2023 so far, up less than 1 percent, the stock is only 5 percent away from its 52-week high of ₹1,733.95, hit on May 4, 2023. Meanwhile, the stock has advanced 29 percent from its 52-week low of ₹1,271.75, hit on June 17, 2022.

Overall, in the last 1 year, the stock has added over 16 percent.

In the March quarter, HDFC Bank posted a 20 percent YoY rise in net profit to ₹12,047 crore while its total income grew 31 percent YoY to ₹53,851 crore. Net interest income for the lender also advanced 24 percent YoY to ₹23,352 crore for the quarter under review.

Meanwhile, its asset quality was largely stable. The gross non-performing assets ratio was 1.12 percent as of Q4FY23, compared to 1.23 percent a quarter ago, and 1.17 percent a year ago. The net non-performing assets ratio was 0.27 percent as of March 2023 quarter, compared to 0.33 percent a quarter ago, and 0.32 percent a year ago.

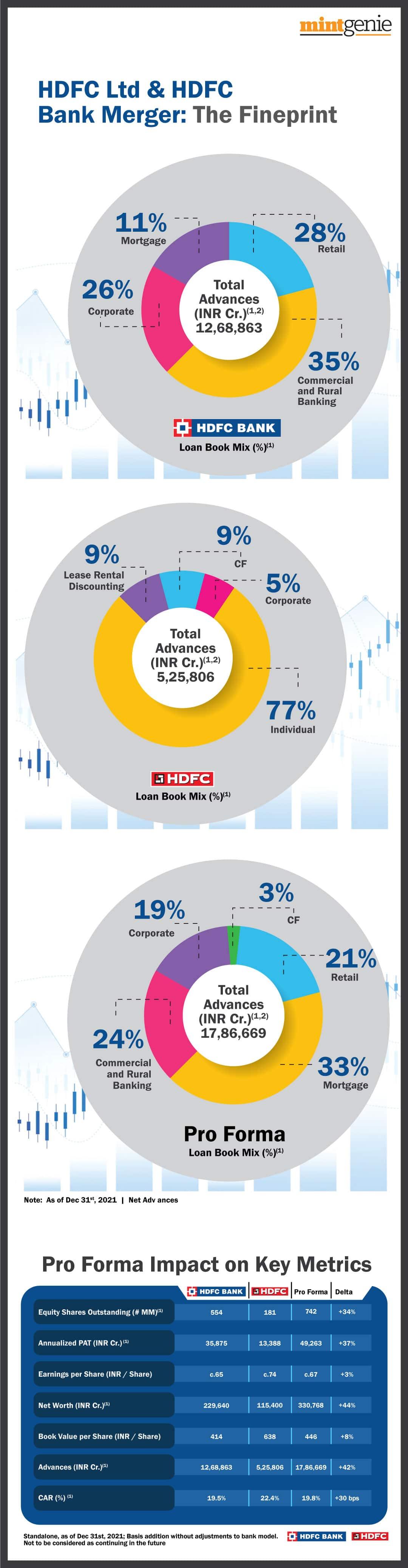

On the back of the ongoing merger with HDFC and the positive outlook of the entire banking space, brokerages have optimistic views regarding the lender going ahead.

Post HDFC Bank's analyst meet, brokerage house Motilal Oswal reiterated its ‘buy’ call on the stock with a target price of ₹1,950, indicating an upside of another 20 percent. The brokerage noted that HDFC Bank remains one of its most preferred picks.

According to MOSL, HDFC Bank appears well positioned to sustain healthy growth, supported by new initiatives, robust branch additions and expansion of digital offerings. It has delivered strong business growth versus peers, resulting in constant market share gains, it further stated, which was propelled by sustained momentum in the Retail segment, along with robust growth in Commercial and Rural Banking.

Also, the lender's asset quality ratios remain robust, while the restructured book has moderated to 31 bps of loans, it observed, adding that a healthy PCR and a contingent provisioning buffer should support asset quality.

The brokerage estimates HDFC Bank to deliver a 19 percent PAT CAGR over FY23-25, with RoA (return on asset) of 2 percent.

Analyst Meet

At its analyst meet, MOSL stated that HDFC Bank management highlighted how the bank is getting future-ready by focusing on strengthening its digital capabilities and sustainable growth after the merger while maintaining RoA at the current level. The bank also plans to announce various new initiatives to provide a superior experience to customers, it added.

For the bank, technology has moved from being an enabler to being a driver of outcomes and it has emphasized that running the bank includes modernizing the existing infrastructure, along with building competencies and CoE (cost of equity), highlighted MOSL. Growth is likely to be broad-based, mainly driven by technology and expanding distribution network, while improved cross-selling will further augment revenue growth, the management further said. They also pointed out that the cost-to-income (C/I) ratio may remain sticky for the near term but could decline to 30 percent over the next 10 years.

On the merger front, the management suggested that the merger process is on track and is expected to be completed in about five weeks, informed MOSL.

"The bank is positioning itself to capitalize on new growth opportunities in mortgage assets, higher cross-selling as customer stickiness improves, and faster growth in liabilities. Investments in branches and digital infrastructure will further support growth over the long term," MOSL further stated.

Another Brokerage

Meanwhile, another brokerage Haitong also retained its bullish call on the stock post its analyst meet. It maintained an ‘outperform’ call on the stock with a target price of ₹1,978, indicating an upside of over 22 percent.

"We believe HDFC Bank is well placed to report a sustained growth momentum and report healthy return ratios. Here on, the growth momentum, traction in deposits and NIM trajectory will be the key. We have not yet factored the merger in our estimates. We have maintained our OUTPERFORM rating with a SOTP of ₹1,978 (unchanged), valuing the bank at 3.0x Mar-25E ABV (unchanged)," it said.

Risks include (i) no improvement in NIMs, (ii) slower than expected credit and deposits growth, and (iii) attrition at the senior management level, it added.