Amid the weakness seen in the market this year, FMCG (fast moving consumer goods) is the only sector that has given a positive return in 2023 so far. The Nifty FMCG index has risen nearly 3 percent year-to-date (YTD) versus a nearly 6 percent fall in Nifty.

ITC vs Godrej Consumer: Which is a better FMCG stock for long term?

TL;DR.

The Nifty FMCG index has risen nearly 3 percent year-to-date (YTD) versus a nearly 6 percent fall in Nifty. Let's find out between ITC and Godrej Consumer Products (GCPL), which stock is a better investment for the long term.

The overall positive outlook for the space as well as a recovery in demand, especially rural, kept the investors bullish on the sector while the equity market remained highly volatile, impacted by inflation, rate hikes, and the latest banking crisis in major US and European banks.

Amid this background, let's find out between ITC and Godrej Consumer Products (GCPL), which stock is a better investment for the long term.

Stock price trend

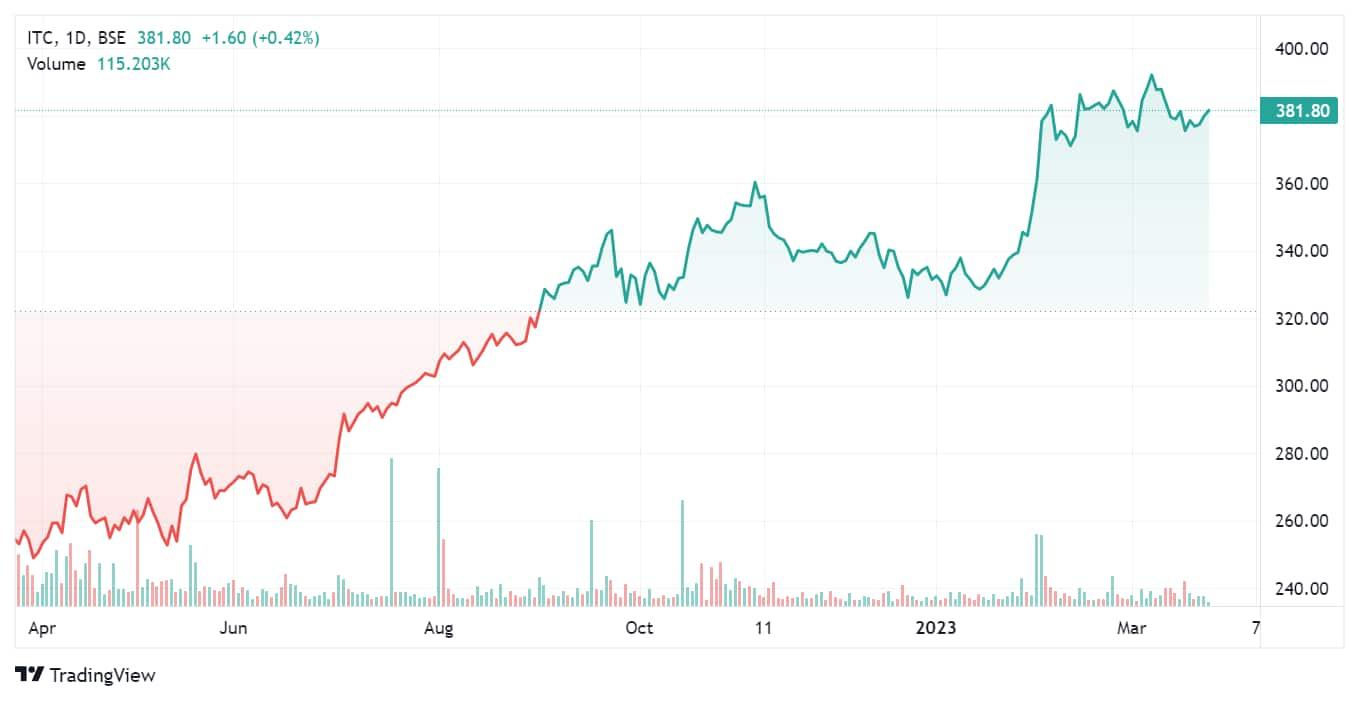

In the last year, both ITC and Godrej Consumer have given positive returns, up 51 percent and 39 percent, respectively. In comparison, the Nifty FMCG index has surged 27 percent while the benchmark Nifty is down around 1 percent.

On a year-to-date basis as well, ITC has added 15 percent while Godrej is up 9 percent versus a 3 percent jump in Nifty FMCG.

Both ITC as well as GCPL gave positive returns in all the 3 months of 2023. ITC is up 1.5 percent in March so far, gained 7 percent in February and 6.2 percent in January.

Meanwhile, GCPL advanced 3.3 percent in March so far, 1 percent in February and 4.5 percent in January.

GCPL stock price trend

About the Firms

ITC is one of India's foremost private sector companies with a gross sales value of ₹90,104 crore and a net profit of ₹15,058 crore in 9M FY23. ITC has a diversified presence in FMCG, hotels, packaging, paperboards & specialty papers and agri-business.

Godrej Consumer is an FMCG firm engaged in manufacturing and marketing personal, household and hair care products. Its geographical segments include India, Indonesia, Africa and others.

Earnings

ITC reported a 23.09 percent increase in consolidated net profit at ₹5,070.09 crore for the third quarter ended December 2022, helped by growth momentum across its operating segments. It had posted a net profit of ₹4,118.80 crore during the same quarter last year.

Its revenue from operations was up 3.56 percent to ₹19,020.65 crore during the quarter under review, as against ₹18,365.80 crore in the corresponding period of the previous fiscal.

"The company sustained its strong growth momentum across all operating segments during the quarter driven by a focus on accelerated digital adoption, customer centricity, execution excellence and agility," ITC said in its earnings statement.

On the other hand, Godrej Consumer reported a 3.55 percent rise in consolidated profit after tax at ₹546.34 crore in the third quarter ended December 31, 2022, versus ₹527.6 crore in the same period last fiscal. Its consolidated total revenue from operations during the quarter under review stood at ₹3,598.92 crore as against ₹3,302.58 crore in the year-ago period, it added.

"We delivered an all-round performance in 3Q FY 2023. Overall sales grew by 9 percent and we witnessed a sharp sequential uplift in underlying volume growth," GCPL Managing Director and CEO Sudhir Sitapati said.

On the outlook, he said, "With commodity pressures abating, we expect a gradual recovery in consumption, expansion in gross margins, upfront marketing investments with a significant focus on reducing controllable costs and improvement in profitability in the coming quarters."

ITC stock price trend

Which is a better long-term investment?

Preeyam Tolia, Senior Research Analyst, Axis Securities, has picked ITC over GCPL.

"We like ITC as the long-term narrative around the company is getting strong on account market share gains and new product launches; (2) FMCG business reaching the inflection point as its EBIT margins are expected to inch up going ahead led by effective implementation of localization strategy, driving premiumization, leveraging technology on both demand and supply side; 3) strong and stable growth in hotels as travel, wedding, and corporate activities have picked up and 4) steady and decent performance in paperboard and agribusiness makes ITC a better play in the long run as it provides better earnings visibility," it explained.

Deepak Jasani, Head of Retail Research, HDFC securities, also said the ITC continues to be his preferred pick.

The market expert noted that ITC’s performance in the past 3 consecutive quarters has been above expectations. Its core business of cigarettes has been reporting solid volume growth and with consistent stability in the taxes and demand environment, Jasani expects volume CAGR to remain healthy in the coming quarters. Unlike its staples peers, the company has displayed resilient operating performance of its FMCG business in the past few quarters. The hotel business has also reported a sharp turnaround and prospects are likely to be buoyant going forward, he forecasted. With strong margin performance across segments coupled with a healthy outlook, and favourable valuations, ITC continues to be Jasani's preferred pick.

For GCPL, the expert noted that Q3FY23 was the first quarter that showcased a meaningful improvement under the new MD’s leadership. Despite the challenging scenario, it posted 3 percent volume growth in its domestic business. He expects this trend to sustain. Increasing traction in the domestic business should improve margins and return ratios. Among staples, GCPL is the key beneficiary of the recent reduction in material costs. Palm oil prices have come off significantly and this should drive the margin recovery. “Indonesia sales and Africa margins shall also recover gradually in our view. Lack of consistency in the Household Insecticides business and economic recovery in Indonesia remain the key monitorables for GCPL,” stated Jasani.

Narendra Solanki, Head Fundamental Research – Investment Services, Anand Rathi, as well, prefers ITC over GCPL.

"We prefer ITC over Godrej Consumer as ITC Limited is indeed a diversified conglomerate. This diversification can help the company mitigate risks associated with fluctuations in a single industry and create a stable revenue stream. ITC brands have strong market positions and enjoy high levels of customer loyalty. The company has a strong distribution network and extensive manufacturing capabilities, which helps it to reach customers in various geographies and offer a wide range of products. The company has a robust financial position, with consistent revenue and profit growth over the years. Additionally, ITC has a good track record of returning value to its shareholders through regular dividend payments and share buybacks," said Solanki.

Furthermore, Vinit Bolinjkar- Head of Research - Ventura Securities, has also recommended ITC over GCPL for the long term due to ITC’s well-diversified business opportunities.

He lists key reasons:

Various growth levers in each vertical: "With buoyancy in the post-pandemic tax collections, the stress on rising cigarette taxation is diminished and should help drive cigarette FCF (free cash flow). Also, FMCG has achieved a critical scale of ₹20,000 cr annual revenue and an EBIT margin of 6.2 percent in FY23. FMCG has been an FCF guzzler, and has become self-sufficient and contributing positively to the overall FCF. Similarly, the agri-commodity business prospects have sharply improved post the Russia-Ukraine war. Furthermore, the reopening of the economy and improving leisure & business travel has significantly improved occupancy at ITC hotels. In addition, increasing migration towards sustainable packaging has improved the prospects for paper and packaging business. We believe that the ITC is firing on all cylinders and could deliver a significant revenue growth and improvement in profitability in the coming years," said.

Valuation gap: The huge valuation gap between ITC and Godrej Consumer. ITC is trading at FY25 P/E of 20.2X, while Godrej Consumer is trading at FY25X P/E of 37.7X, he pointed out.

Dividend: Strong dividend payout of over 80 percent by ITC in the past 3 years, which is likely to sustain due to strong FCF generation from all the business vertical, he added.

Nirav Karkera, Head of Research at Fisdom, said that ITC and Godrej both are strong bets, for a distinct set of reasons.

As per the expert, the consumer segment continues to reel under pressure stemming from the inflationary heat, El Nino risks, sluggish rural demand, and inadequate percolation of softening commodity prices.

However, the story for ITC seems to be swinging against the broader narrative, he said. "ITC's recent earning prints and dividend yields reflect a strong growth proposition. The tobacco segment has been clocking a rather healthy growth rate and we expect the same to sustain to a great degree. As of now, we expect further punitive taxation to be off the table, at least in the near term. Alongside, the non-tobacco segments have also started strengthening with the earliest signs being observed in terms of topline growth. Considering growth prospects and current valuations, ITC is clearly a ‘buy’ in the segment," explained Karkera.

Further, he also highlighted that Godrej consumer has been picking pace lately.

This pace is growing at a healthy rate and seems sustainable right now. The company seems to have a re-oriented focus towards select segments of the domestic business that offer higher margins. While the domestic business grows on the back of margin expansion, critical operations in global emerging markets indicate promising volume growth. Versus peers and basis conventional earnings-based multiples, the stock seems well-priced even at the moment, he said.

Picking the right stocks is the most important part of becoming a successful investor

First Published: 24 Mar 2023, 03:03 PM IST

Topics to follow

Related Stories

Explain Like I am 5

personal finance

Old Vs new income tax regime: CBDT releases tax calculator to help you decide which regime to follow

Team MintGenie