Softening commodities and better earnings visibility drove an uptick in indices from the lows of June last year. The Nifty Midcap index outperformed the benchmark Nifty, rising 25 percent from June lows as against a 9 percent rise in Nifty50 (from June lows).

However, overall in 2022, the midcaps underperformed the benchmarks, rising a little over 1 percent as against an over 4 percent jump in Nifty.

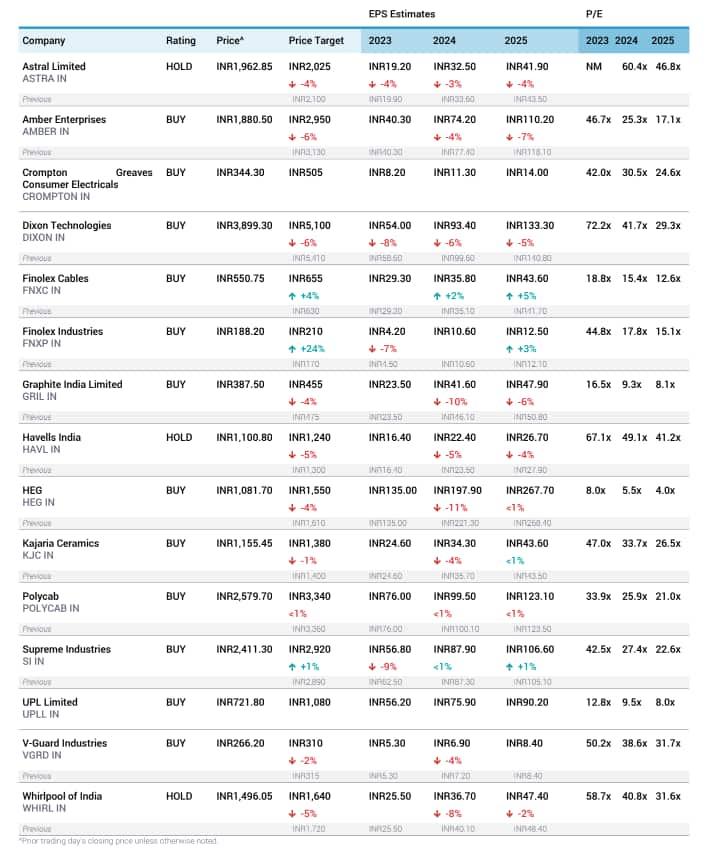

Going ahead, global brokerage house Jefferies sees an earnings revival in mid-cap firms in FY2024 as commodity prices turn favourable and also expects the operating margins of midcaps to rise around 90 basis points (bps) YoY. The brokerage recommends a bottom-up approach in the mid-cap space and advises investors to stay selective. It prefers themes like capex revival, housing, and PLI (production-linked incentive).

"FY22 RoE (return on equity) of Nifty at 15 percent is higher than RoE of Nifty Midcap at 11 percent. But, over FY22-25E, prospects of RoE expansion appear higher in Midcaps (+320 bps) vs Nifty (+60 bps), indicating signs of margins bottoming and earnings revival," said the brokerage.

Investment rationale

Commodities Turning Favourable: As per the brokerage, PVC prices have seen an uptick of 9 percent MoM (month-on-month) in December 2022 to $850/MT which could improve near-term operating margins (OPM) of mid-cap firms like Supreme Industries, Finolex Industries, and Astral led by waning inventory losses. Also, LME copper has risen by 13 percent in Q3FY23, which would likely bode well for OPM in cables & wires, especially for Polycab, Finolex Cables, and V-Guard Industries, the brokerage pointed out. Further, the correction in crude oil by 23 percent in H2CY22 will likely soften natural gas prices in 2023, which augers well for Kajaria Ceramics, it noted.

Trend Reversal: In H1FY23, midcaps posted stronger sales, up 30 percent YoY but weaker EBITDA margin (avg -210 bps), noted the brokerage. But now, many sectors like durables, tiles, electrodes are alluding to softer offtake, leading the brokerage to pencil in lower sales growth in FY24E at 16 percent YoY (+29 percent in FY22). Even so, select demand pockets could stay healthy, for example, private capex revival and PLI upside will be positive for Dixon Tech and Amber Enterprises, noted the brokerage. With most input commodities turning favourable, Jefferies expects average OPM for its mid-cap coverage universe to rise by +90 bps YoY in FY24E vs -180bps YoY in FY23E.

Capex Revival & Housing to Drive Volumes: The brokerage further pointed out that with the economy resuming post Covid, uptick in capex (B2B) and housing appears to be gaining pace. As government's budgetary allocation for infra/capex has risen notably in 2022, private capex is also on an upward trajectory, it noted. Key beneficiaries, as per the brokerage, could be Polycab, Havells, and Supreme Industries.

PLI Tailwind: Indian electronic manufacturing services (EMS) industry is forecasted to reach $135bn by FY26, as cited by Dixon, implying a 30 percent CAGR over $36 billion in FY21. Indian labour cost is ~1/3rd that of China. PLIs provide opportunities for exports and backward integration, said Jefferies. Dixon Tech (Buy) is a recipient of 5 PLI approvals (mobiles is the largest), whereas Amber Ent (Buy) has 2 PLI approvals. But, the relative slowdown in mobile / durable sales is likely to weigh on near-term top-line growth, it cautioned.

Graphite Electrodes

Jefferies highlighted that the impact of rising interest rates on construction/infra and volatility in European energy costs would likely be key risks for Graphite India and HEG in 2023. Over FY22-25E, it estimates HEG's sales/PAT CAGR (+27 percent/+38 percent) to outpace Graphite India's (+13 percent/+23 percent), as GRIL's German production (18 percent of its capacity) could be impacted by volatility in energy costs, noted the report. Leverage will be a key monitorable amid rising interest rates, it added.

Top Picks

Jefferies prefers strong brand franchises that demonstrate good margin resilience. It likes Supreme Ind as its margin uptick is likely from FY24e with PVC stabilizing; 40 percent value-added mix. It is also bullish on Polycab on the back of solid execution despite softening copper; focus to improve FMEG. Kajaria Ceramics is another of its top picks amid its focus on exports by Morbi to aid domestic demand and pricing stability. And finally, it prefers Crompton Greaves Consumer Electricals due to its healthy margins in core business and potential synergies from Butterfly integration.

Meanwhile, the brokerage maintained its hold calls on Astral, Havells and Whirlpool.

Demand slowdown and raw material volatility are key risks for the midcap space, it added.