India's largest passenger car manufacturer Maruti Suzuki posted strong results for the June quarter of FY24 (Q1FY24). While its profit beat estimates, its margins were below Street expectations.

Maruti Suzuki Q1: Margins disappoint but PAT beats estimates, say brokerages; retain buy calls

TL;DR.

While most brokerages have retained their buy calls on Maruti Suzuki and some have even raised target prices, they remained disappointed by the company's margins reported in Q1FY24 and thus, cut earnings estimates.

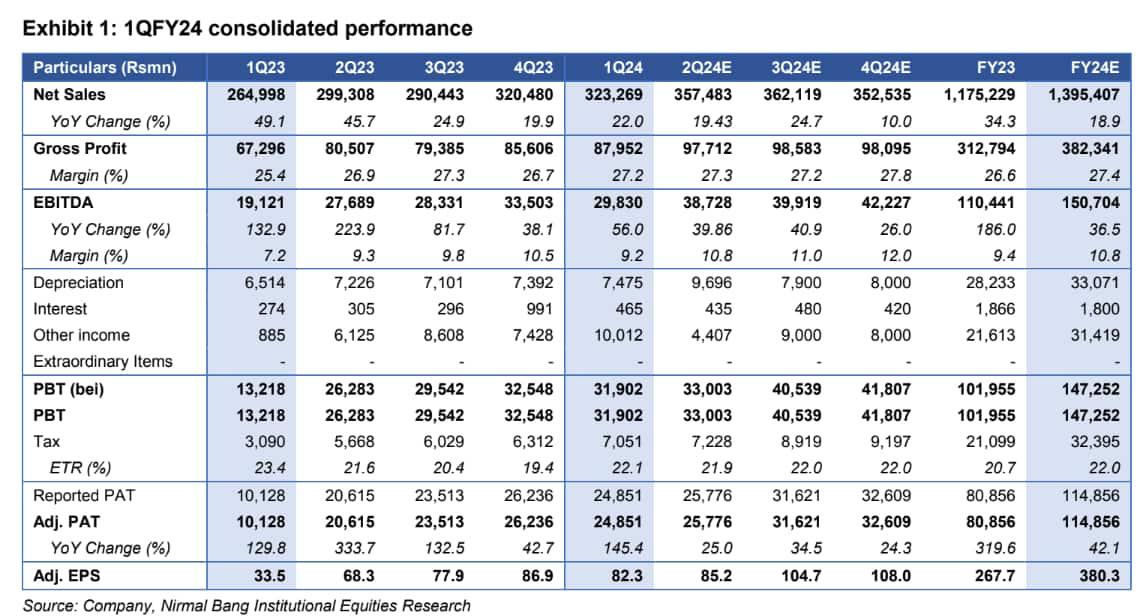

Maruti's standalone profit surged 145 percent year-on-year (YoY) to ₹2,485.1 crore for the quarter ended June 2023, driven by larger sales volume, improved realization, and higher non-operating income. In comparison, it posed a PAT of ₹1,012.80 crore in the year-ago period.

Meanwhile, the auto major’s standalone revenue jumped 22 percent to ₹32,326.9 crore in Q1FY24 from ₹26,499 crore in the corresponding period last year. EBITDA also rose 56 percent to ₹2,983.1 crore in the quarter under review versus ₹1,912 crore in the year-ago quarter. EBITDA margin also expanded by 200 basis points (bps) to 9.2 percent from 7.2 percent, YoY, but missed most analysts’ estimates.

Further, the company announced the termination of the contract manufacturing agreement and exercised the option to acquire 100 percent shares of Suzuki Motor Gujarat Pvt Ltd (SMG) from Suzuki Motor Corporation (SMC).

While most brokerages have retained their buy calls on the stock and some have even raised target prices, they remained disappointed by the company's margins reported in Q1FY24 and thus, cut earnings estimates. The target prices for Maruti are in the range of ₹10,920-11,503, indicating an upside potential of up to 17 percent.

Prabhudas Lilladher: The brokerage reiterate its ‘BUY’ recommendation with an unchanged target price of ₹11,100, implying an upside potential of 13 percent from its current market price of ₹9,821, as on July 31.

Maruti's Q1FY24 revenues were marginally higher than estimates, however, higher employee costs and other expenses led to a miss on EBITDA margins. EBITDA margins expanded by 280 bps YoY, but were lower QoQ on lower volumes and higher employee and operating expenses. Chip shortage impacted 28k units and MSIL noted that the situation is largely normalised now. Going ahead, MSIL hopes to outgrow the PV industry’s growth led by its SUV (Sports Utility Vehicle) portfolio, increased traction from CNG models, and servicing stronger order book, said the brokerage. It expects the firm to partially recoup lost market share through faster growth than the industry in the UV (Utility Vehicle) & MUV (Multi Utility Vehicle) segments. PL has built its UV and MUV mix to increase to 30 percent in FY24 vs 21 percent in FY23.

"MSIL is well placed to strongly benefit from (1) market share gains and ASP (average selling price) increase coming from ahigher mix of the new UV portfolio, (2) 260 bps increase (over FY23-25E) in EBITDA margins on the back of commodity cost softening, cost control, operating leverage and higher UV share and (3) rural revival. However, PL has marginally changed its EPS estimates for FY24E by -1.5 percent.

HDFC Securities: The brokerage maintains a BUY call on the stock with a revised target price of ₹10,920 (from ₹10,214 earlier), indicating an upside potential of over 11 percent.

Maruti's Q1FY24 PAT was ahead of estimates even as a lower-than-expected margin was offset by higher-than-expected other income. Over the last three quarters, MSIL has been on an aggressive launch spree, having launched four new models in a bid to recover its lost share in UVs, which has now recovered to 23 percent in Q1. MSIL is now again the market leader in the UV segment. The recent success of GV and the higher-than-expected order bookings for Invicto are a case in point; customers are considering Maruti’s products as 'worthy contenders' even in the ₹15 lakh segment, where few investors were so far doubting the company’s 'right to win'. Given the new growth opportunities, the brokerage continues to maintain its BUY call.

JM Financial: The brokerage has retained its buy call on the stock with a target price of ₹11,500, indicating an upside potential of 17 percent.

In Q1FY24, MSIL’s Adjusted EBITDA margin came in at 10 percent, which is below estimates. The sequential decline in margin was due to new launch expenses and higher discounts. Employee cost also had the one-off impact of 80 bps related to employee retention bonus. MSIL lost 28k units due to chip shortage during Q1FY24 but the management highlighted that chip supplies have largely normalised. Order inflow continues to remain healthy with over 355k units of pending bookings led by recent launches/CNG variants. With the introduction of Jimny, Fronx, and Invicto, MSIL intends to further strengthen its presence in the B-segment (regained leadership position in SUVs in 1QFY24). The benefit of a richer portfolio mix, softening commodity costs and higher operating leverage is expected to aid margins going ahead, it rationaled. JM estimates revenue and EPS CAGR of 13 percent and 23 percent over FY23-26E. After two consecutive years of market share loss, it believes that MSIL is at the cusp of market share recovery led by new launches.

Motilal Oswal: The brokerage also has a buy call on the stock with a target price of ₹11,150, implying a 14 percent potential upside.

MSIL is expected to outperform underlying industry growth of 6-8 percent in FY24, resulting in market share gains and margin recovery. This should be further supported by easing supply challenges, said the brokerage. Stable growth in domestic PVs and a favorable product lifecycle augur well for MSIL. It expects market share gains and margin recovery in FY24, led by an improvement in supplies, a favorable product lifecycle, mix and operating leverage.

MOSL increased its FY24E EPS by 3 percent to factor in better ASPs and higher other income. However, it cut FY25E EPS by 1 percent, as the benefits of higher ASP and higher other income are more than offset by the SMG acquisition.

Nirmal Bang: The brokerage, as well, retained its bullish view on the stock with a target price of ₹11,503, indicating an upside potential of over 17 percent.

MSIL’s 1QFY24 results were broadly in line with our estimates. PAT came in 12 percent above our estimate due to other income being higher than our estimate. MSIL’s plan to expand production will help it to increase its overall market share and the rising share of SUVs in its overall portfolio will boost margins. It expects the sales momentum to continue in the coming quarters and SUV market share to increase.

The brokerage remains positive on MSIL and expects 8 percent volume CAGR over FY23-FY25E, led by new model launches and market share gains. The company is doing very well in the UV segment and had 23 percent market share in 1QFY24. It expects the momentum to continue in the coming quarters.

Source: Nirmal Bang

First Published: 01 Aug 2023, 12:36 PM IST

Related Stories

Explain Like I am 5

markets

What are the investing mistakes retail investors make and how to avoid them?

Manik Kumar Malakar