The life insurance space in India still remains underpenetrated, giving it a robust growth opportunity for the future. Recently, domestic brokerage house Religare Broking has initiated coverage in the life insurance space with a bullish outlook.

Religare Broking bullish on life insurance sector; initiates coverage on 4 stocks with 3 ‘buy’ calls

TL;DR.

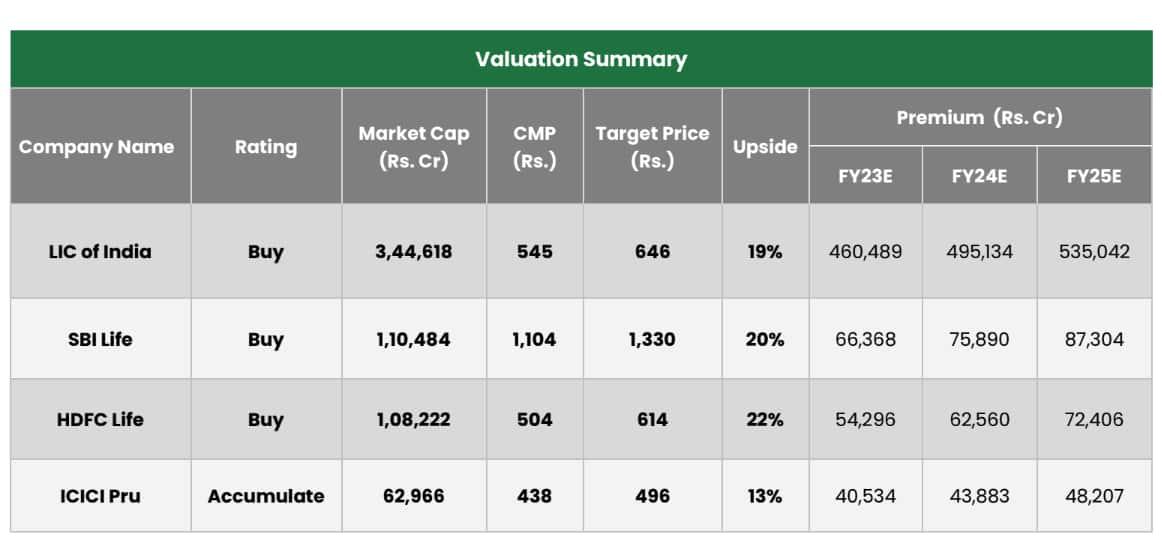

Religare Broking has initiated coverage on the top 3 private insurance players - HDFC Life Insurance, SBI Life Insurance, and ICICI Prudential, and public sector major LIC of India in this space.

"We are positive on the life insurance sector as it is poised for growth due to favorable factors like rising GDP growth, increasing financial literacy amongst individuals, growth in group insurance, and focus on financial inclusion. Government schemes like Pradhan Mantri Jeevan Jyoti Bima Yojana, Pradhan Mantri Suraksha Bima Yojana would also give a push to sector and help in penetration of Insurance in rural areas," it said.

Religare expects the topline growth to improve due to favorable product mix and improvement in the value of new business (VNB) margins. It has initiated coverage of the top 3 private insurance players - HDFC Life Insurance, SBI Life Insurance, and ICICI Prudential and public sector major LIC of India in this space.

The brokerage has ‘buy’ calls on 3 of these life insurers - LIC, SBI Life and HDFC Life with a potential upside of up to 22 percent and an ‘accumulate’ call on ICICI Prudential with a 13 percent potential upside.

Source: Religare

Insurance Sector

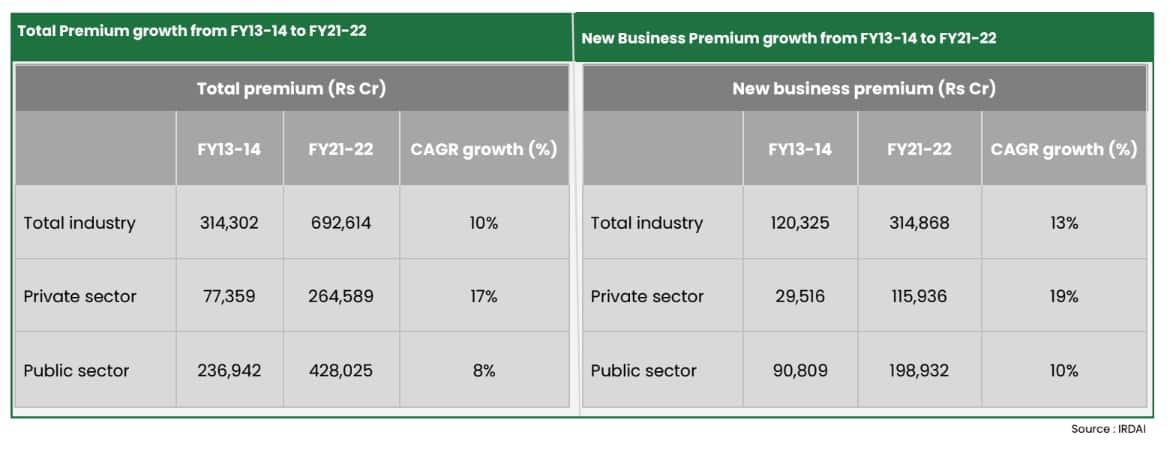

As per the brokerage, the insurance sector (especially life insurance) is one of the underpenetrated sectors in India. As of 2021, as per Swiss Re Report, India’s life insurance business was ranked 9th in the world and 4th in Asia with a global share of 3.23 percent. The share of life insurance premium in total premium was high at 76.14 percent as against the global share of 43.69 percent, it noted, adding that as of FY21-22 the insurance penetration was 3.2 percent (US and Canada 2.7 percent) from 2.72 percent in FY16-17. Although the life insurance penetration remains above US and Canada, the protection gap (83 percent in 2019) remains one of the largest in the world, highlighted the brokerage.

"The under penetration presents an opportunity as the overall industry is in the nascent stage in India and has grown consistently over the years. On a total premium basis, the industry grew at 10 percent CAGR from FY14-FY22 while on a new business premium basis; the industry grew at 13 percent CAGR from FY14-FY22," informed Religare. It also pointed out that on a new business premium basis, the private sector outpaced the public sector (LIC of India) as it grew at a CAGR of 19 percent while the public sector saw a growth of 10 percent CAGR over FY14-FY22.

Going ahead, the brokerage expects the total premium and new business premium to increase in the estimates as more policies are dispensed in the future which will increase the penetration of life insurance. It estimates the total business premium of its coverage universe (representing 82 percent of market share) to grow at 10 percent CAGR over FY22-FY25E while new business premium is seen growing at 12 percent CAGR over FY22-FY25E. The business premium will grow sustainably in the estimates as the number of policies is seeing consistent growth along with growth in new business premiums, it added.

Source: Religare

Stocks

HDFC Life: The brokerage has initiated coverage on the stock with a ‘buy’ call and a target price of ₹614, indicating an upside of 22 percent. HDFC Life Insurance is India’s third largest life insurer with a new business premium market share of 7.2 percent as of February-23. The company has performed consistently as premium grew at a CAGR growth of 19 percent for FY17-FY22, noted the brokerage.

"We are positive on the life insurer due to favorable product mix, diverse distribution channel, and growth in new business premium. The company will benefit from its parent company merger which will provide it the boost to grow its premium income. It will also benefit from the positive macroeconomic tailwinds as we believe that it is rightly a place to benefit from growing trends in the sector. We initiate coverage of the company with a Buy rating and a target price of ₹614 valuating the company at 3.0x FY25E embedded value," it said.

SBI Life: The brokerage has initiated coverage on the stock with a ‘buy’ call and a target price of ₹1,330, indicating an upside of 20 percent. The brokerage informed that SBI is the largest private insurer in terms of market cap and also has the largest market share in terms of annual premium equivalent (APE) and VNB. It has the lowest operating cost ratio amongst its peers and is constantly improving (9.9 percent in FY20 to 8.6 percent in FY22) mainly due to its operating efficiencies and low commission cost, mentioned Religare.

"We are positive on the insurance company due to its cost efficiencies, leveraging on SBI Bank’s network and access to its customer base while changing in product mix from ULIP to protection and non-par products. We believe the insurer is a better place to capture the growth insurance market in the country and also operate efficiently. We expect APE/NBP/VNB to grow at 19 percent/18 percent/23 percent CAGR over FY22-25E. We initiate coverage of the insurance company with a Buy rating and target price of ₹1,330 valuing the company at 2.2x of FY25E embedded value," it said.

ICICI Prudential: The brokerage has initiated coverage on the life insurer with an ‘accumulated’ call and a target of ₹496, indicating a potential upside of 13 percent. The brokerage informed that ICICI Prudential is the fourth largest life insurer with a market share of 4 percent in new business premiums and a 15 percent market share in sum assured amount. The insurer has seen a decline in premium income growth in the past few years while the market share has also declined, it added.

"ICICI Prudential’s market share has declined in the past but we expect the market share to catch up with its peers as it changes in product mix and also the distribution channel will contribute to the premium growth. We remain positive on the insurance company’s growth prospects and as the margins have started to see improvement. We expect APE/VNB/NBP to grow at a CAGR of 11 percent/15 percent/12 percent over FY22-25E. We initiate coverage of ICICI Prudential Life Insurance with Accumulate rating and target price of ₹496 valuing the company at 1.8x of FY25E embedded value," it said.

LIC: The brokerage has initiated coverage on the only public life insurer with a ‘buy’ call and a target of ₹646, implying a potential upside of 19 percent. LIC of India is India’s oldest and largest insurance player with a market share of 64 percent in terms of new business premium and 16 percent in terms of sum assured (as of Feb-23), noted Religare.

"We are positive on LIC due to high brand equity, large agency network, widely spread product mix, and balanced product mix. We believe the industry tailwinds will help LIC maintain its foothold in the insurance industry for a prolonged period of time. Market share has been declining over the years as private players are more aggressive in their approach but we expect to see a bounce back from LIC of India due to changes in product mix and further penetration in the rural region. We expect APE/NBP/VNB to grow at a CAGR of 14 percent/10 percent/9 percent. We initiate coverage of LIC of India with a Buy rating and target price of ₹646 valuing the company as 0.7x of FY25E embedded value," it said.

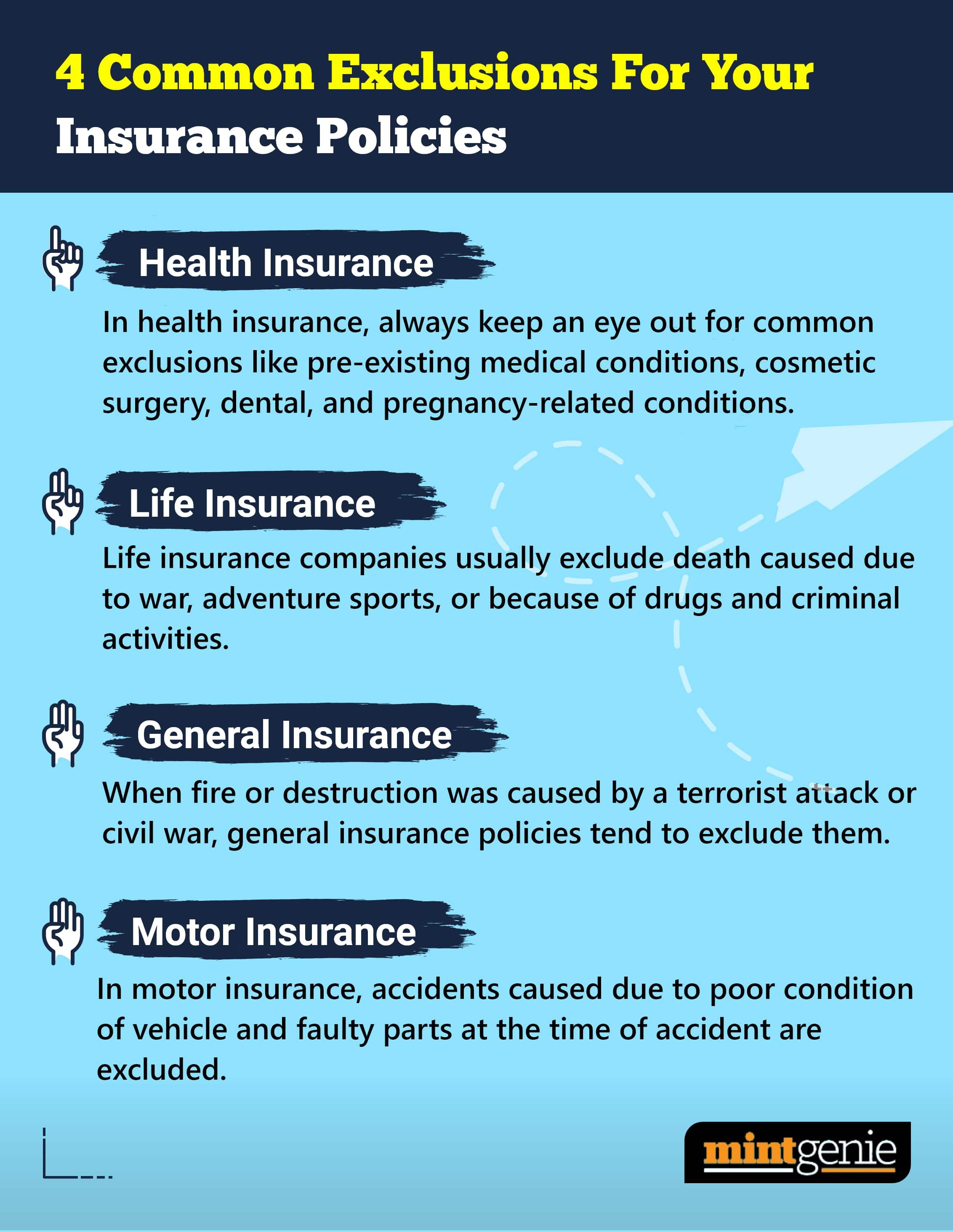

Here we describe the common exclusions for health, life, motor and general insurance policies.

First Published: 06 Apr 2023, 05:43 PM IST

Related Stories

Explain Like I am 5

personal finance

Life Insurance: How can NRIs buy policies in India and what should they keep in mind?

Rakesh Goyal