Tata Consultancy Services (TCS) and Infosys are set to report their financial results for the quarter and year ending March 31, 2022, next week.

Result Preview: IT sector growth to be moderate in March Quarter

TL;DR.

The report estimates cross-currency headwinds of 30- 60bps in Q4 given the appreciation of USD against EUR, GBP and AUD.

In their latest report on "Earnings Preview on Indian IT Services", brokerage firm Prabhudas Lilladher reported that the revenue growth for IT services would be moderated by 150bps on a higher base in Q4 on the back of strong sequential growth in the last 2 quarters and it estimates currency headwinds of 30-60 bps.

They believe that margins will be under pressure in FY23, given persisting supply-side constraints and the gradual return of travel and facility costs.

"We expect strong demand commentary from IT majors led by Infy with revenue growth guidance of 11-13% YoY CC for FY23", says the report.

It anticipates margins to decline by 40-80bps QoQ due to headwinds from aggressive hiring led to a drop in utilization and backfilling of attrition with lateral recruits at higher costs, partially offset by INR depreciation and operating leverage. Margins are expected to decline by 150bps YoY due to increased supply-side pressures and roll out of wage hikes twice in the last one year.

Prabhudas Lilladher prefers Infy and TCS from Tier 1, which have strong growth momentum on a high base and best in class operating metrics. Among tier 2 they prefer Mindtree and Coforage. Affle remains their buy idea in internet space.

They believe that Coforge is the only company that(120 bps QoQ) is expected to post a QoQ increase in margins.

The report estimates, 1.4%-5.5% QoQ CC (avg: 3.2%) for Tier-1 and 3.9%-8.5% QoQ CC (avg: 4.3%) for Tier-2 and the average revenue growth estimates, 0.9%-5.0%(avg:2.7%) for Tier – 1 and 2.0% - 5.0% (avg: 3.8%) for Tier -2.

The report pegs TCS, Infosys, and Wipro – the country’s leading software exporters – to post revenue growth in the range of around 3-3.1% quarter-on-quarter (QoQ), while HCL Technologies is expected to post the weakest growth of 0.9%.

TechM (5.5% QoQ CC) is expected to lead the growth in Tier 1 due to seasonal strength in communication and contribution from acquisitions.

In Tier – 2 Persistent is expected to lead the growth, 8.5% QoQ CC (6.5% QoQ CC organic), it added.

| Q4FY22 Estimates | USD Revenue growth QoQ | USD Revenue growth YoY | CC Revenue growth QoQ | EBIT Margins | QoQ Bps | YoY Bps |

| TCS | 2.6% | 11.7% | 3.1% | 24.9% | -12 bps | -193 bps |

| Infosys | 2.6% | 20.7% | 3.0% | 22.9% | -62 bps | -161 bps |

| HCL tech | 0.9% | 11.4% | 1.4% | 18.2% | -85 bps | 163 bps |

| TechM | 5.0% | 21.1% | 5.5% | 14.2% | -63 bps | -228 bps |

| Average Tier-1 | 2.7% | 17.8% | 3.2% | 19.4% | -44 bps | -156 bps |

| L TI | 4.7% | 29.4% | 5.1% | 17.4% | -55 bps | -196 bps |

| Mphasis | 4.9% | 26.9% | 5.2% | 14.7% | -36 bps | -136 bps |

| Coforge | 3.8% | 33.7% | 4.2% | 16.1% | 126 bps | 280 bps |

| LTTS | 4.0% | 18.5% | 4.4% | 18.3% | -33 bps | 170 bps |

| CYIENT | -1.6% | 3.6% | -1.2% | 12.9% | -98 bps | 25 bps |

| Persistent | 8.0% | 40.7% | 8.5% | 13.5% | -46 bps | 35 bps |

| Zensar | 2.0% | 22.2% | 2.5% | 10.2% | 13 bps | -605bps |

| Average Tier - 2 | 3.8% | 26.1% | 4.3% | 15.2% | -26 bps | -55 bps |

| Overall Average | 3.4% | 22.9% | 3.9% | 16.8% | -33 bps | -94 bps |

| Source: Prabhudas Lilladher |

Mindtree is expected to report 5.3% CC growth, and revenue growth of 5.0%.

The report estimates cross-currency headwinds of 30- 60bps in Q4 given the appreciation of USD against EUR, GBP and AUD.

For Zensar tech, the brokerage house decreased EPS estimate by 8.7%/11.6% for FY23/24E led by - a cut in revenue estimates by 2.7/1.3% for FY23/FY24 and a cut in margin estimates by 90bps/150bps in FY23/24 which is due to cost pressures of high attrition levels (26.7% in Q3FY22) and investments in sales team and tech capabilities.

"We expect a healthy growth in headcount in Q4 as well as in FY23 given demand is chasing supply, we believe quarterly attrition will stabilize this quarter but is still at elevated levels. LTM attrition is expected to inch up. Russia Ukraine crisis is likely to add pressure on ER&D talent supply,” the report added.

Prabhudas Lilladher in their report mentioned some key things to monitor for IT services in Q4-

Impact of current macro/geopolitical uncertainties on tech spending, the scope for gaining market share from vendors who have a considerable supply-side presence in Ukraine and war-affected regions in Eastern Europe, especially for ER&D companies, Growth and margin outlook for FY23, Durability of demand, commentary on attrition, sub-con costs and resumption of travel.

Growth outlook

Prabhudas Lilladher expects a healthy growth momentum in FY23 given continued demand for compressed technology transformation led by cloud, data analytics and customer experience. It expects Infy to guide 11-13% YoY CC growth in FY23, lower than the 12-14% YoY CC guidance given at the start of FY22 due to lower contribution from large/mega deals to TCV.

Further, it expects HCLT to provide double-digit revenue growth guidance and estimates revenue growth of 12%-15% YoY USD for Tier 1 and 17%-21% YoY USD for Tier 2 in FY23.

Infy’s margin guidance to remain at 22-24% for FY23. Since HCLT’s margins are near the lower end of their FY22 guidance band of 19-22%, we expect HCLT to lower its margin guidance band to 18-20% for FY23. We anticipate margins to remain under pressure in FY23 led by continued supply-side pressures and partial return of travel and facility expenses. These headwinds are expected to be partially offset by pyramid optimization, higher offshoring, price improvements and revenue growth leverage. We note that the benefit of price improvements in new deals will flow through P&L with a lag, said the brokerage.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

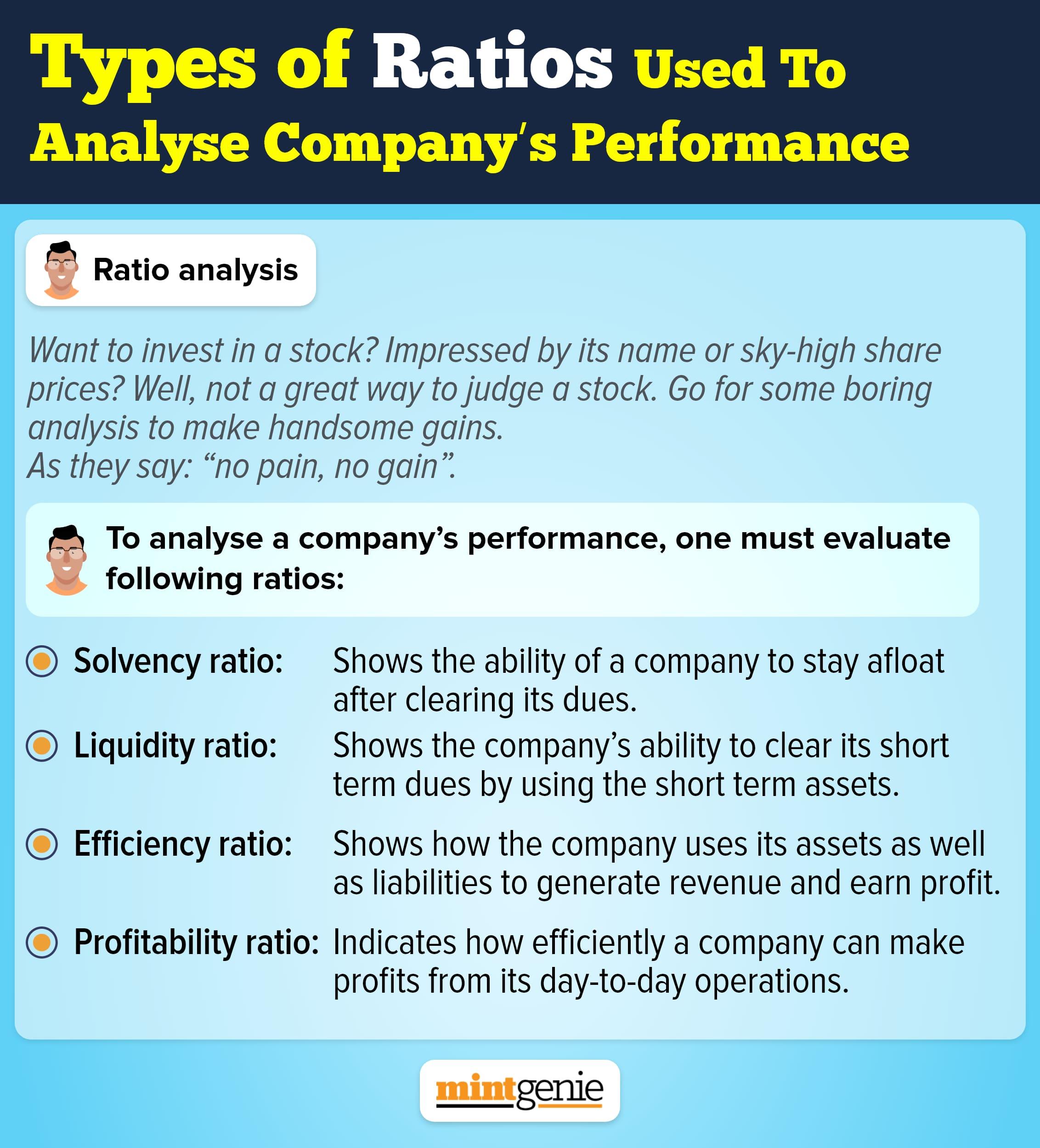

Types of ratios used to analyse company's performance

First Published: 11 Apr 2022, 07:57 AM IST