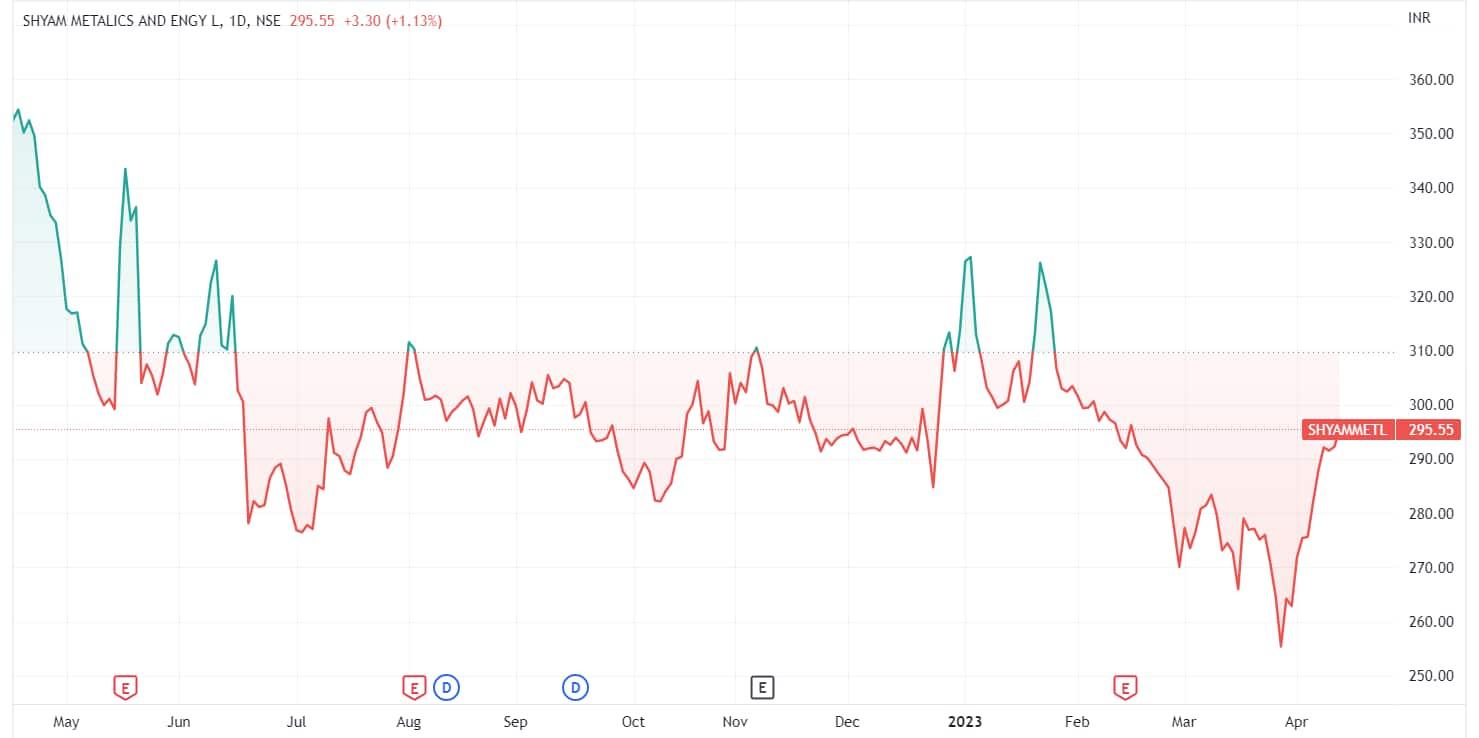

Shyam Metalics and Energy (SMEL), a leading integrated metal producer, has witnessed a decline of over 17% to ₹295.25 in its share price during the last one-year period. However, ICICI Securities, a leading domestic brokerage firm, remains optimistic about the company's future and has assigned a target price of ₹570 apiece, that suggests a whopping 93% upside potential.

The brokerage highlights several key reasons for its bullish outlook. These include the ramp-up and stabilisation of existing capacities; the company's recent foray into stainless steel and colour-coated steel, which is expected to yield an additional EBITDA of ₹6 billion by FY25E; the earnings contribution from Ramsarup Industries, and niche capacities in aluminium foil and low-carbon ferrochrome, which are likely to be earnings-accretive, it said.

ICICI Securities pointed out that the company's business model is unique and differentiated, focusing on niche segments that provide value instead of focusing on volume.

The company has commissioned its 14 ktpa low-carbon (LC) ferrochrome plant, making it the first domestic company to produce LC ferrochrome since Balasore Alloys in FY14.

Additionally, SMEL has stabilized its 40 ktpa aluminium (Al) foil plant, producing 6-micron thin foils, of which 75–80% is exported. It has also embarked on a 0.4 MTPA colour-coated line capable of producing GI/GL and PPGL products and started custom rolling at Mittal Corp's stainless-steel plant in Indore, the brokerage noted.

The upcoming facilities of the company have a significantly lower capex intensity in comparison to its peers, leading to a payback period of less than three years and a RoE of 20–22% over the next two years.

Moreover, the integration of raw materials such as ferrochrome and sponge iron for the stainless-steel plant and pig iron for the DI pipe plant is anticipated to further enhance profitability, according to ICICI Securities.

Despite a capex of Rs. 15-20 billion per annum (which will be funded through internal accruals) until FY25, the net debt/EBITDA ratio is projected to remain within 0.4x, which is the lowest among its peers, the brokerage highlighted.

ICICI Securities believes that by FY25, SMEL will be the only metal company in the world to have revenue streams from carbon steel, stainless steel, and downstream aluminium business.

“Owing to continuous capacity expansion through both organic and inorganic routes, we expect revenues to increase to ₹265 billion by FY25E. The revenue growth is spurred by rolled products volume,” said the brokerage.

ICICI Securities finds SMEL as the best-placed steel company in its coverage universe due to its attractive growth prospects. The stock is currently trading at the lowest valuation among its peers, with a 2.4x FY25E EBITDA.

SMEL has consistently traded at a lower valuation compared to its peers on both EV/EBITDA and P/E. It is currently trading at a 50% discount to Tata Steel and Jindal Steel & Power on EV/EBITDA and at a discount of 42% and 56% to Tata Steel and Jindal Steel & Power, respectively, on FY25E EPS, it stated.

While recognizing the potential of Shyam Metalics and Energy, the brokerage also outlined some of the few risks. One such risk is being exposed to fluctuations in prices of raw materials, intermediates, and final products, which are heavily influenced by demand and supply in both domestic and global markets. The volatility of these prices can significantly impact SMEL's business, financial condition, and operational results.

Delay in the commissioning of capacities and export duty on iron ore lingering, resulting in further decline in pellet prices, are the other downside risks, it added.

03 analysts polled by MintGenie on average have a 'strong buy' call on the stock.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.