The metal sector has been in the limelight since the beginning of CY23 amid China's reopening. Steel stocks have remained resilient in the recent market correction and exhibited strength post the Union Budget. Tata Steel and JSW Steel are two major steel companies in our country, but let's find out which is a better long-term investment.

Tata Steel vs JSW Steel: Which one is better for long-term investment?

TL;DR.

Steel stocks have remained resilient in the recent market correction and exhibited strength post the Union Budget. Tata Steel and JSW Steel are two major steel companies in our country, but let's find out which is a better long-term investment.

Stock price trend

In the last 1 year, while Tata Steel has declined around 9 percent, JSW Steel has advanced 9 percent.

Just in February so far, Tata Steel has shed nearly 9 percent on the back of weak Q3 earnings while JSW Steel has been flat. Meanwhile, in January 2023, Tata Steel rose 6 percent whereas JSW shed 6 percent.

In the long term, both steel stocks have given multi-bagger returns. Tata Steel has rallied 101 percent in the last 5 years while JSW Steel has surged 156 percent.

Tata Steel stock price trend

About the stocks

Tata Steel is the steel arm of the prestigious Tata Group. It's primarily engaged in the business of steel making, including raw material and finishing operations. Its product portfolio caters to Agriculture, Automotive, Steels, Construction, Consumer Goods, Energy and Power, Engineering, and Material Handling sectors. The company is also the world's most geographically diversified steel producer in over 50 countries.

JSW Steel, on the other hand, is a part of the JSW Group and is involved in the business of manufacturing and selling iron and steel products. The company has a diversified product portfolio used in the automotive, general engineering, and project and construction sectors.

Earnings

Tata Steel reported weak earnings for the third quarter of FY23. In Q3, it posted a net loss of ₹2,500 crore versus a net profit of ₹9.598 crore in the year-ago period. Its revenue from operations slipped 6% to ₹57,084 crore in Q3FY23 as compared to ₹60,783 crore in Q3FY22. Net debt stood at ₹71,706 crore, with net debt to EBITDA at 1.76x and net debt to equity at 0.65x. Consolidated EBITDA for the firm stood at ₹4,154 crore, with an EBITDA margin of 7 percent in the last quarter. Sharp drops in realisations and spreads in Europe affected profitability.

For the India business, the company logged a profit of ₹1,918 crore with a revenue of ₹32,325 crore for the period under review. On the outlook, Tata Steel said there was a visible pickup in steel prices across key regions on improved China demand outlook and sustained spending on infrastructure in India.

Meanwhile, JSW Steel reported an 89 percent fall in net profit at ₹490 crore for the three months ended December 2022. The company had posted a profit of ₹4,357 crore in the last year period. Its revenue from operations, meanwhile, grew 2 percent YoY to ₹39,134 crore as against ₹38,017 crore reported in the corresponding period of last year. The company has clocked an operating EBITDA of ₹4,547 crore, while margins came in at 11.6 percent. The margins were higher sequentially due to lower coking coal prices. The company's net debt stood at ₹69,498 crore as of December-end with net debt to equity at 1.09x.

Despite a challenging global economic scenario, the company sees healthy demand growth in steel in India, which it says, will aid the performance in the coming quarters. On the outlook, JSW Steel sees recovery in rural demand on the back of a better winter crop and in residential real estate. Autos and renewables remain strong, which should augur well for the company.

Though Tata Steel's total revenue is nearly twice that of JSW Steel, its revenue has grown at a CAGR of 17.2 percent against 23.5 percent of JSW Steel in the last five years. Meanwhile, the five-year average operating profit margin for Tata Steel stood at 18.7 percent against 21.8 percent of JSW Steel.

JSW Steel stock price trend

Which is a better stock?

Vinit Bolinjkar, Head of Research at Ventura Securities, prefers JSW Steel over Tata Steel. He believes that JSW Steel is better positioned to benefit from the revival in domestic steel demand.

Bolinjkar noted that Tata Steel generates 33-35 percent of its sales volume from Europe. In a backdrop of inflation-led macro risk in the US and Europe, he expects the overseas business of Tata Steel will continue to remain under pressure and could drag the overall consolidated performance of the company.

On the other hand, he stated that JSW Steel is a pure domestic play and export contributes only 8-10 percent of its volumes. The company is expected to benefit from strong demand for infrastructure and revival in the real estate market.

Due to its strong growth outlook, JSW Steel stock is trading at a premium valuation of 6.4X FY25 EV/EBITDA, while Tata Steel stock is trading at 5.3X FY25 EV/EBITDA, said Bolinjkar.

Aditya Welekar, Senior Research Analyst, Axis Securities, on the other hand, likes Tata Steel. Here's why:

1) Tata Steel has the plan to grow towards the 40 MTPA capacity target in India by 2030. As a part of the journey towards expanding its Indian capacity, the company has begun operations at Neelachal Ispat Nigam Limited (NINL) and is getting ramped to a rated capacity of around 1MTPA. FY24 should fully reflect the incremental 1MTPA NINL volumes. The company expects the Kalinganagar phase II 5MTPA blast furnace and the ramp-up of the 0.75MTPA Electric Arc Furnace at Punjab to start in FY25. The company has sufficient landbank and raw materials (iron ore) for this organic expansion.

2) Its Indian operations can do well in the short to medium term as they are fully integrated for iron ore (25 percent for coking coal). European operations are, however, a drag on the company. The company has guided on negative EBITDA/t for the upcoming three quarters in Europe due to weak demand, high energy costs, and the relining of one of the blast furnaces at its Netherlands operations.

3) The management is evaluating the support framework proposed by the British government for Tata Steel UK towards a green steel transition. The original ask was for 50 percent capex support for the electric arc furnace, slab caster, and downstream capacities, but the government has proposed a partial amount. Thus, the management is relooking at configuration. Woes at its European operations would be the significant overhang on the stock. Management's approach towards bringing the European business to profitability will be an important watchpoint.

According to Bolinjkar, quick economic revival and pick up in the capex cycle have reaffirmed India’s credential as the world’s fastest-growing economy, at a time when much of the developed economies of the western world and China are beset with recessionary risk. As a result, the domestic steel industry will see improvement in demand in CY2023, however, the global steel demand is expected to remain muted, he noted.

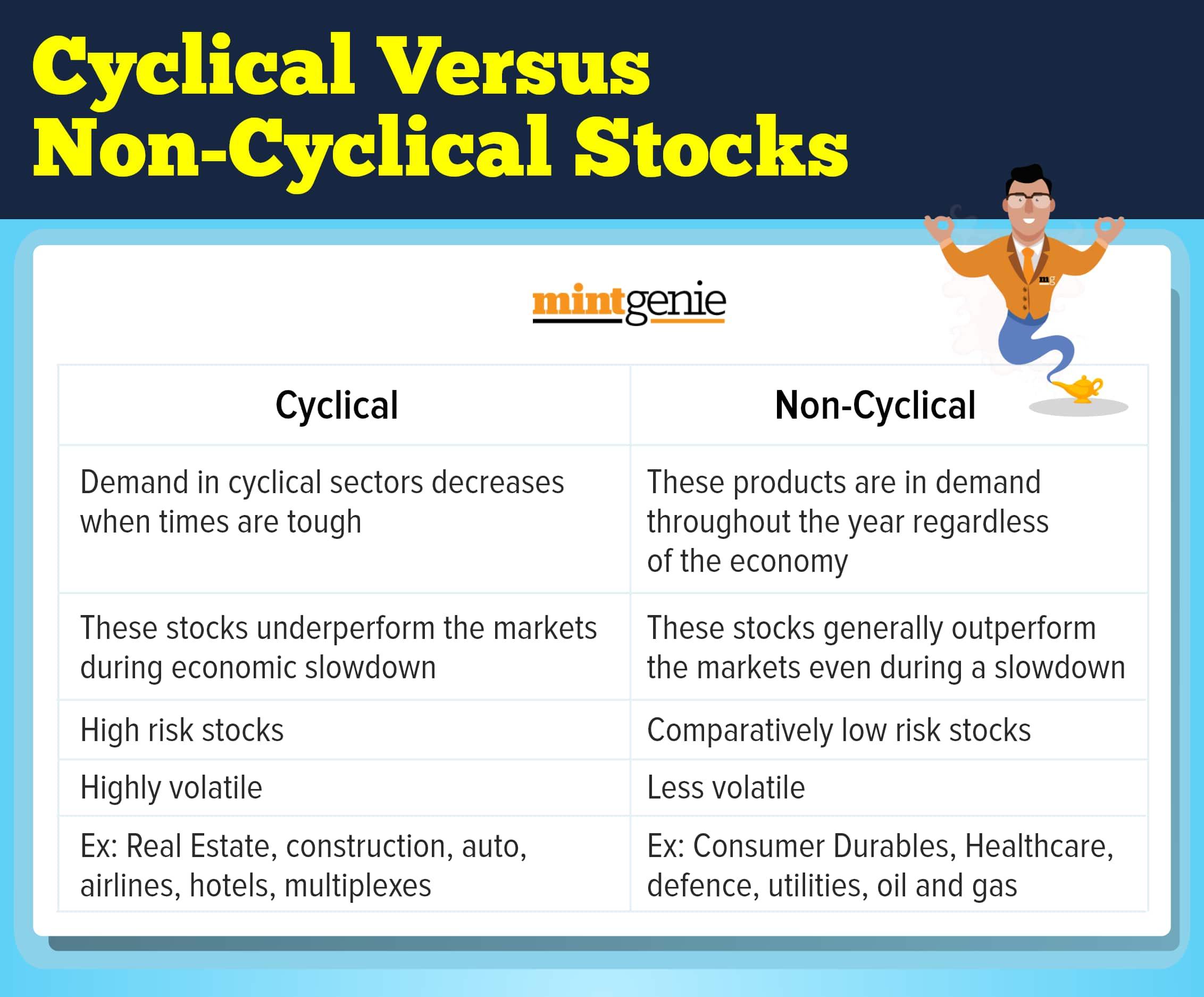

Cyclical vs non-cyclical

First Published: 10 Feb 2023, 01:33 PM IST

Related Stories

personal finance

Your Questions Answered: Equity vs real estate — Which will yield better returns in the long term?

International Money Matters