Tata Group firm Titan Company failed to meet expectations in its June quarter (Q1FY24) earnings, reporting a dip in its net profit as well as margin.

Titan Q1 results disappoint: Brokerages remain mixed; set target prices between ₹2,600 and 3,400

TL;DR.

Brokerages remained mixed on Titan after its June quarter results with target prices between ₹2,600 and 3,400, indicating potential for a 13 percent downside to a 14 percent upside.

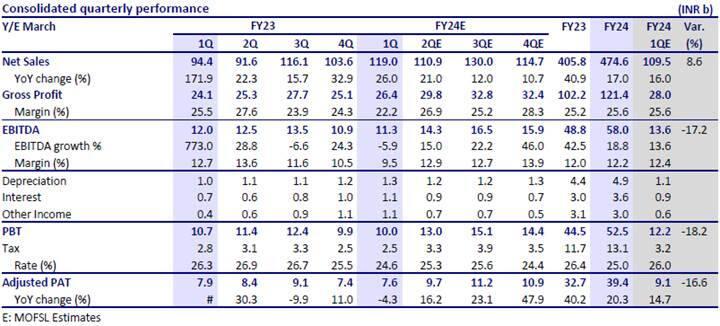

The company posted a 4.3 percent decline in its consolidated net profit at ₹756 crore in Q1FY24 versus ₹790 crore in the same quarter last year. Meanwhile, on a sequential basis, the company's profit rose 2.7 percent from ₹736 crore in the previous quarter.

Its total consolidated revenue, however, rose almost 26 percent to ₹11,897 crore as against ₹9,443 crore in the year-ago period. Meanwhile, the company's revenue increased 14.83 percent QoQ from ₹10,360 crore in the previous quarter.

“The year has started well for us with double-digit revenue growth across business segments. The jewellery business remained the star performer with a 19 percent growth on a YOY basis,” said CK Venkataraman, managing director of the company.

Stock Price Trend

Shares of Titan fell as much as 3.2 percent to its intra-day low of ₹2,883 on Thursday on the back of weak earnings for the June quarter. The stock is now over 10 percent away from its 52-week high of ₹3,211.10 seen on July 7 this year and has risen 27 percent from its 52-week low of ₹2,268.90, hit on February 2.

It has gained 25 percent in the last one year, outperforming the 13 percent rise in Sensex in the same period. Meanwhile, it has advanced 12.5 percent in 2023 YTD.

Titan stock price trend

What brokerages say:

Brokerages remained mixed on Titan after its June quarter results with target prices between ₹2,600 and 3,400, indicating potential for a 13 percent downside to a 14 percent upside. While they remained bullish on Titan's strengths and long-term growth prospects; the decline in margins and expensive valuations kept them cautious.

Centrum Broking: The brokerage has a ‘buy’ call on the stock with a target price of ₹3,400, indicating an upside of 14 percent from its current market price of ₹2,979, as on August 2.

“Titan’s Q1FY24 print was mixed; despite volatility in gold prices consol. revenues grew 26 percent, yet EBITDA/PAT declined by 5.9 percent/4.3 percent. We remain upbeat on Titan’s operating performance led by strong pent-up demand across business segments yet its footing in the international market appears to be promising. We note Titan’s strategy revolving around serving millennials, meeting their aspirational demand with introduction of new designs and channels, yet a rising share of wedding jewelry could pay richly in our view. Further with rising interest rates and industry formalization showing up in market share gains for Titan. The turnaround in the Caratlane, watches, and eyewear divisions and continuity in their profitability potential. With a stable margin outlook, we tweaked FY24E/FY25E earnings by 4.1 percent/6 percent,” it says.

Prabhudas Lilladher: The brokerage has retained an ‘accumulate’ rating with a target price of ₹3,240, implying an upside of around 9 percent.

“We cut our FY24/FY25 EPS estimates by 4.9 percent/2.3 percent as we cut EBIT margins in Jewellery by 50 bps to 12.3 percent (lower end of TTAN guidance of 12-13 percent band) and 50 bps each in watches and Eyewear. We believe Titan is investing for future growth which is reflected in rationalization of physical gold premium, increased advertising and consumer activations and exchange schemes in a tough demand environment, which bodes well for long-term growth. Demand trends in July remain strong across segments which gives us confidence of a pick-up in margins in coming quarters,” it says.

JM Financial: The brokerage has a ‘buy’ call on the stock with a target price of ₹3,070, indicating an upside of just 3 percent.

In simple words, Titan’s June quarter growth was achieved at the cost of short-term margin - a choice exercised by the business to tide over issues that emanated due to gold-price volatility and consequently, weaker consumer sentiments, it said.

“A rather generous gold-exchange offer to attract buyers, however, caused a significant erosion in gross margin and led to lower profit vs year-ago level, despite strong growth in topline. What is comforting, however, is that the issues aren’t structural in nature and the impact, therefore, should not be long-lasting. We believe the management retaining its 12-13 percent margin guidance is a testimony to this. Demand seems rather resilient thus far - July growth appears to be close to the Q1 range. The stock could react negatively to the weak June quarter result - a buying opportunity, in our view,” added the brokerage.

Motilal Oswal: The brokerage has a ‘buy’ call on the stock with a target price of ₹3,325, indicating an upside of 12 percent.

“Titan's Q1FY24 revenue grew 26 percent YoY, ahead of our expectation, with double-digit growth across all segments. However, due to lower-than-expected margins, EBITDA and adj. PAT missed our estimates. Margins were adversely affected by seasonality, volatility in gold prices and a one-time diamond price inventory gain in Q1FY23. Four-/Five-year Jewelry EBIT CAGR was robust at 24 percent/22 percent in 1QFY24. Management indicated that Jewelry's margin guidance of 12-13 percent in FY24 remains unchanged and 1Q is normally weak on the margin front due to more gold contribution. Titan's brand-building initiatives across segments, increasing customer base, store expansions and development in international markets continued to be impressive,” said the brokerage.

Phillip Capital: The brokerage downgraded the stock to ‘neutral’ with a revised target price of ₹3,100, implying a 4 percent upside.

“We downgrade Titan to Neutral from BUY with a revised TP of ₹3100 (60x June-25 EPS, 16% EPS Cagr over FY23-26) as near-term margin pressure (expect 100 bps YoY) in FY24 and rich valuations (61x FY25 EPS) are most likely to limit any meaningful stock price appreciation. We expect the Ebitda margin to drift to 11.5 percent in FY24 vs 12.5 percent in FY23. Moreover, rich valuations (61 x FY25 EPS) do not leave scope for error in a highly volatile demand environment,” it said.

“We would turn buyers on the stock at lower levels, as structural levers for formalization remain intact. In our view, Long term drivers remain intact including: (1) increasing consumer shift to organised jewellery, as unorganised jewellers find it difficult to operate due to increasing cost of compliance in an industry where margins are wafer-thin, (2) aggression in the highly lucrative wedding jewellery market, (3) increasing traction on the revised gold exchange programme for Titan’s Golden Harvest Scheme (4) stringent cost efficiency program (5) Network expansion in Tier 2/ Tier 3 and targeting market leadership in those markets,” it added.

HDFC Securities: The brokerage has a ‘sell’ call on the stock with a target price of ₹2,600, indicating a downside of almost 13 percent.

Titan’s top-line growth remains healthy. Revenue grew 26 percent YoY and ex-bullion sales grew 22 percent YoY as both buyers’ growth and ticket sizes aided growth. The key takeaway from the Q1 print was the preference for market share gain over margins. Growth investments via (1) aggressive exchange offers; (2) price rationalisation; and (3) brand building led to a decline in jewellery margins. The base quarter also had a one-time diamond price inventory gain, it said.

“We suspect that consumer demand normalization amid rising competition will keep jewellery margins under pressure. Hence, we cut FY24/25 EPS estimates by 3 percent each and maintain our REDUCE rating,” said the brokerage.

Source: MOSL

First Published: 03 Aug 2023, 01:54 PM IST