Avenue Supermarts, which owns the supermarket chain D-Mart, has been a consistent outperformer since listing. From its IPO price of ₹299, the stock has surged as much as 1069 percent to ₹3,496.10 till April 10, 2023. Meanwhile from its listing price of ₹641, on March 21, 2017, the stock has jumped 445 percent.

Up 1069% from IPO price, PL sees another 40% upside in this retail stock; here's why you should buy

TL;DR.

From its IPO price of ₹299, the stock has surged as much as 1069 percent to ₹3,496.10 till April 10, 2023. Meanwhile from its listing price of ₹641, on March 21, 2017, the stock has jumped 445 percent.

The stock's IPO opened for subscription between March 8 and March 10, 2017, and was subscribed 104.48 times.

Incorporated in 2002, Avenue Supermarts Limited is Mumbai-based supermarket chain D-Mart. The company is among the largest and most profitable F&G retailers in India. It offers a wide range of products with a focus on the Foods, Non-Foods (FMCG) and General Merchandise & Apparel product categories.

The company has 112 stores located across 41 cities in India. It operates and manages all its stores. It also operates distribution centres and packing centres which form the backbone of the supply chain to support its retail store network. The firm has 21 distribution centres and six packing centres in Maharashtra, Gujarat, Telangana and Karnataka.

However, in the last 1 year as well as in 2023 YTD, the stock has shed around 15 percent each. While it has gained around 2 percent in April so far, it fell 0.5 percent, 2.4 percent and 14 percent in March, Feb and Jan 2023, respectively.

Post the recent correction in the stock, brokerage house Prabhudas Lilladher sees a 40 percent potential upside in the stock in the next 1 year.

The brokerage has a ‘buy’ call on the stock and has raised the target price of the stock to ₹4,699 from ₹4,675 earlier.

Avenue Supermarts stock price trend (since listing)

"We remain positive on D’Mart Ready as it has increased city presence to 22, reduced delivery time to 1 day with a reduction in delivery charges (Flat ₹49 as against 3 percent earlier). We believe attractive prices and a far better consumer proposition than Big Basket (the largest online retailer) will enable D’Mart Ready to turn EBIDTA positive by FY25 and PAT positive by FY27. We believe D’Mart has a huge growth runway ahead given the low probability of heightened competition in modern trade, 1500+ store potential in existing clusters (current stores 306) and fast scale up in D’Mart Ready," explained the brokerage.

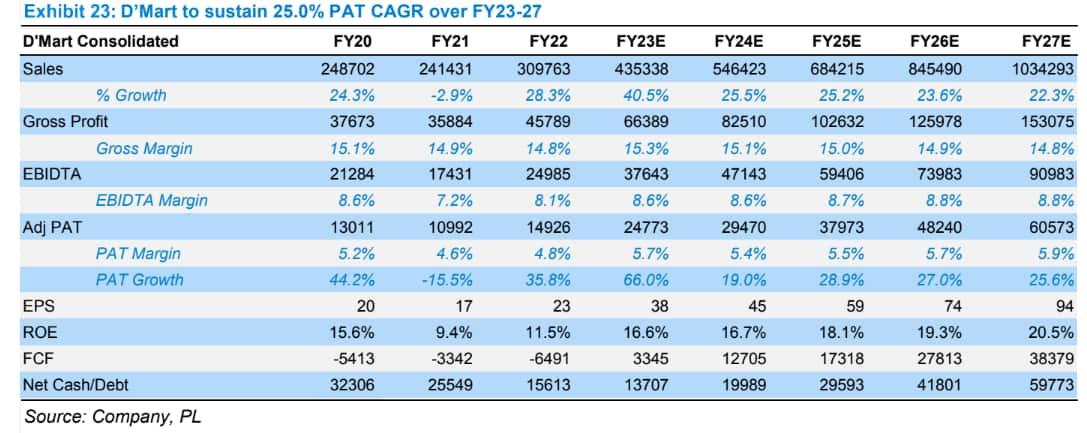

It has estimated a 25 percent PAT CAGR over FY23-27 and expects revenue and EBITDA CAGR of 24 percent and 24.7 percent, respectively, over FY23-27. It also sees D’Mart turning free cash flow (FCF) positive in FY23 with a steady increase in FCF.

However, it also pointed out that the stock has corrected by 27 percent from a 52-week high due to concerns on 1) slow post Covid recovery in sales parameters 2) deterioration in sales mix 3) effectiveness of D’Mart 4) sustainability of growth & profitability metrics.

It had hit its 52-week low of ₹3,185.10, in May 2022.

The brokerage further noted that the deterioration in sales parameters is a result of a 3x increase in stores within emerging clusters and a 100 percent increase in the number of stores with <2 years’ vintage, which will correct over time.

Earnings

In the December quarter, Avenue Supermarts reported a 6.7 percent YoY rise in its consolidated profit after tax to ₹589.68 crore as against a profit of ₹552.56 crore in the corresponding quarter last fiscal. Meanwhile, its revenue grew 25 percent YoY to ₹11,305 crore in the quarter under review vs ₹9,217.76 crore in the corresponding quarter in the last fiscal.

However, its revenue growth slowed down on a sequential basis in Q3FY23, even though the company posted a double-digit rise in the top line. This growth in the topline in Q3 is the lowest since the March quarter of FY22.

In the September quarter, the company’s revenue grew 36% on-year to ₹10,385 crore.

Investment Rationale

The brokerage informed that D’Mart Ready has expanded to more than 22 cities in Q3FY23 from just 5 cities in FY21. The company is finding the right balance with 1) No free delivery and flat ₹49 charges for home delivery and free pickup from D’Mart Ready outlets 2) Delivery time - D’Mart has reduced it to 0-1 days from 2-3 days amid store penetration and improving supply chain 3) Zero difference in prices between D’Mart Ready and D’Mart stores.

"Our analysis suggests that D’Mart remains highly competitive with a slight edge over Jio Mart, while it has a huge pricing advantage over the largest online player Big Basket," said PL.

Average Bill Value: Average bill value has increased by 59 percent from ₹1,237 in FY20 to ₹1,973 in FY23 due to inflation in consumer products, it said. While PL expects bills/stores to increase and average bill value to come down, there seems to be some structural change in the scenario. Bills per store would have grown by 5.7 percent for first half of 2023 and PL is factoring in a 3.7 percent growth over FY22-27 as against 5.9 percent over the previous 5 years.

Store openings: D’Mart opened its highest-ever stores in FY22 (50) and is expected to continue the momentum going ahead with the huge potential that India offers, said PL.

Online segment: D’Mart has been a reluctant entrant in online retail given 1) high discounting 2) lack of customer loyalty 3) deep losses and 4) sky-high consumer expectations, however, D’Mart Ready (its online store) has grown into a formidable player, stated the brokerage. Its sales have grown from ₹140 crore in FY19 to ₹1670 crore in FY22. D’Mart first started with D’Mart Ready stores with consumer pick-up from stores and later extended it to home delivery format, informed PL. Sales jump from ₹140 crore to ₹790 crore in FY21 and sharp growth during covid enabled D’Mart to fine-tune its model, it added.

Customer service: D’Mart Ready is clear in its focus to service customers who are looking for bargain deals and not get into instant delivery, free delivery and cash deals which is cash burning and unsustainable in long term, said PL. The company has not been undertaking even flash sales like Independence Day, Republic day etc. while focusing on proving “Everyday Value”. It has been gradually improving consumer offers in terms of delivery charges, delivery time, and minimum order value and has also started credit card-based offers recently, it highlighted.

While D’Mart Ready has not been giving any credit card/debit card linked schemes in the past like other players who offer a plethora of such schemes; it has made a small beginning recently with 7 percent cash back on Kotak Mahindra Bank credit card on orders above ₹4,000. PL believes such value-based orders can increase the average ticket size and improve competitiveness with other players.

DMart Ready: D’Mart Ready is currently 4.9 percent of consolidated sales and PL expects the same to increase to 10 percent by FY27. Its gross margins (GM) have improved by 190 bps since FY20, but it will remain lower than the GM of consolidated business. This will happen as the share of lower margin Food and Grocery will be higher and that of General Merchandise and Apparel will be lower than the company average, it explained.

PL also estimates that D’Mart Ready will drag GM by 20bps in FY23 and this will gradually come down to around 12-14bps, as the share of non-food and grocery increases from the current level. It further predicts D’Mart Ready will achieve EBIDTA margins of 1.5 percent by FY27. D’Mart Ready will provide scale and an absolute increase in profitability; it will broadly cap the consolidated margins of D’Mart, added PL.

It anticipates topline from D’Mart Ready to more than triple by FY25 and the business to turn EBITDA positive as well by FY25. It estimates that D’Mart Ready will turn PAT positive by FY27.

Disclaimer: The views and recommendations made above are those of individual analysts or broking companies, and not of MintGenie.

Source: PL

First Published: 10 Apr 2023, 01:40 PM IST

Topics to follow

Related Stories

markets

Explained: What does ex-dividend date mean and when is one entitled to stock dividend?

Dhanya Nagasundaram