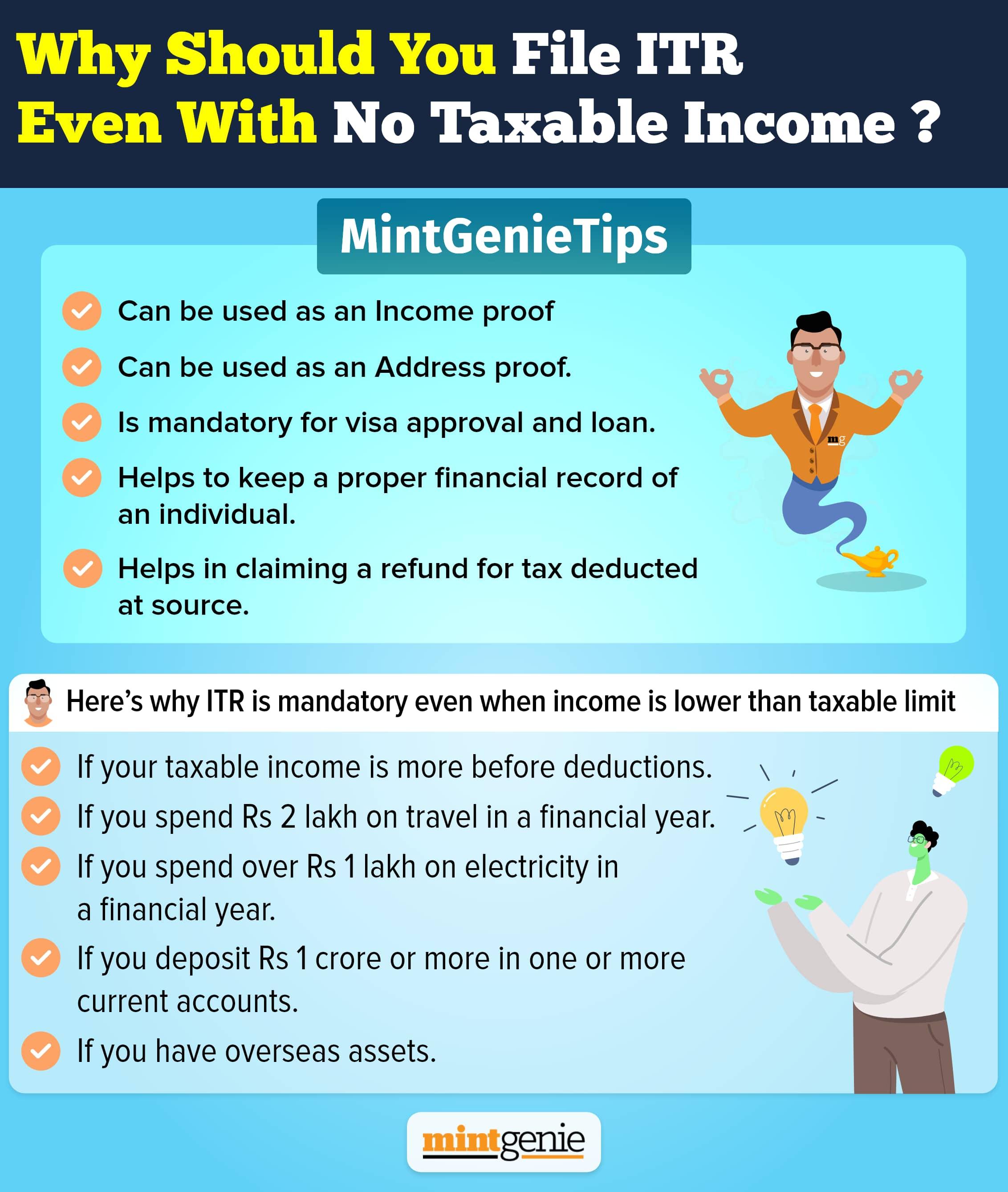

Cash transactions are now under strict scrutiny by the Income Tax Department. In recent times, the department along with various investment platforms like banks, mutual fund houses, and brokerage platforms, has imposed stricter regulations on cash transactions for the general public. These institutions now have set limits on cash transactions, and anyone exceeding these limits may receive a notice from the department.

The heightened vigilance against cash transactions by the department is part of a broader effort to combat black money and tax evasion. Cash transactions have often been misused to hide illegal income, and by imposing limitations on them, the Department aims to deter tax evasion.

The new regulations on cash transactions have several implications for the general public. Although this may cause some inconvenience, it is essential to recognise that these measures are in place to safeguard the public from financial crimes. If there is a minor violation, the Income Tax Department might issue a notice to the offender.

Engaging in substantial cash transactions could result in an individual receiving a notice from the Income Tax Department. Various cash-related transactions, such as those conducted through banks, mutual fund houses, brokerages, and property registrars, fall under scrutiny. It is mandatory to report high-value transactions to the department if they exceed a certain threshold.

Through agreements with various government agencies, the department has established a robust system for sharing financial information. This collaborative approach empowers the department to track down individuals who participate in substantial cash transactions without disclosing them in their tax filings. These agreements serve as a potent tool for combating tax evasion.

With access to a diverse array of financial data, including bank account records, credit card statements, and investment transactions, the department can effectively identify individuals who may be evading taxes. These comprehensive data sources enhance the Department’s ability to enforce tax compliance.

The cash transactions that may cause you to receive an unwarranted notice from the Income Tax officials include:

Bank fixed deposits

The Central Board of Direct Taxes (CBDT) has mandated that cash deposits in bank fixed deposits should not exceed ₹10 lakh. As part of this announcement, banks are now required to disclose whether individual deposits exceed the specified limit in one or more fixed deposits.

Savings account deposits with banks

Cash deposits in bank accounts are subject to strict limits in India. For savings accounts, the annual cash deposit limit is ₹10 lakh. This means that a savings account holder cannot deposit more than ₹10 lakh in cash in a single financial year. If a savings account holder exceeds this limit, they may receive an income tax notice from the tax department.

Cash deposits in current accounts are subject to a higher limit of ₹50 lakh. However, even current account holders should be aware of the cash deposit limits, as any cash deposits or withdrawals that surpass the ₹10 lakh limit in a financial year must be reported to the tax authorities.

Paying off credit card bills

The Central Board of Direct Taxes (CBDT) has implemented stringent guidelines concerning cash payments for credit card bills. Any cash payment of ₹1 lakh or more against credit card bills must be promptly reported to the tax department. Moreover, individuals who make cash payments of ₹10 lakh or more to settle credit card bills within a financial year are required to disclose such transactions to the tax department.

These regulations have a broad scope and apply to all individuals, irrespective of their income or tax status. Enforced by the income tax department, non-compliance with these rules can lead to penalties.

The primary objective behind these rules is to combat money laundering and tax evasion. By compelling individuals to report significant cash payments for credit card bills, the government aims to make it challenging for criminals to disguise their illicit activities. These rules not only serve as a deterrent against financial wrongdoing but also assist in identifying individuals who may be facing difficulties in managing their credit card payments.

If you are considering making a substantial cash payment to settle a credit card bill, it is crucial to be aware of CBDT’s regulations. To comply with the requirements, individuals can report such transactions by filing Form 61A with the Income Tax Department. Staying informed and adhering to these guidelines will help foster a transparent financial system while curbing illicit practices.

It is essential to disclose any significant transactions when filing your Income Tax Return (ITR). If you have engaged in high-value transactions using credit cards, remember to report them on Form 26AS while filing your ITR to avoid getting an income tax notice.

Transactions surrounding real estate sales or purchases

In India, property registrars are obligated to notify the tax authorities of any immovable property investments or sales amounting to ₹30 lakh or more. This means that whether you pay for the property in cash or through other means, if the transaction exceeds ₹30 lakh, the property registrar will send a report to the tax authorities.

The primary purpose of this reporting requirement is to enable the tax authorities to identify individuals who may be evading taxes on their real estate transactions. If you have intentions to buy or sell a property valued at more than ₹30 lakh, it is crucial to be aware of this reporting obligation. To ensure compliance, it is advisable to report any cash transactions related to the property in Form 26AS while adhering to the tax regulations. This will help you stay by the law and avoid potential complications with the tax authorities.

Shares, mutual funds, debentures, and bonds investments

Investors who engage in mutual funds, stocks, bonds, or debentures must be mindful of the cash transaction limits. The maximum cash amount that can be invested in these assets during a financial year is ₹10 lakh. Exceeding this limit could lead to an investigation by the tax department.

To track high-value cash transactions, the authorities have introduced an Annual Information Return (AIR) statement. This statement encompasses all financial transactions an individual undertakes in a financial year, including investments in mutual funds, stocks, bonds, and debentures.

In cases where an investor makes a cash investment in these assets surpassing ₹10 lakh, the transaction details will be reported to the tax department. Subsequently, tax officials will scrutinise the transaction to ensure compliance with the law.

Being well-informed about the cash transaction limits and accurately reporting all financial transactions is crucial for investors. By doing so, they can contribute to the prevention of money laundering and tax evasion, thus avoiding potential investigations by authorities.

It is crucial to understand that if investigated by the tax department, investors may face penalties or even criminal prosecution.

The AIR statement serves as a potent tool for the tax department to identify individuals evading taxes, making adherence to the law essential to maintain financial integrity and compliance.

The due date for filing the ITR is getting closer with each passing day. As per a statement issued recently by the Ministry of Finance, over 70 percent of taxpayers have zero tax liability while more than two crore people have already filed their ITRs to date.