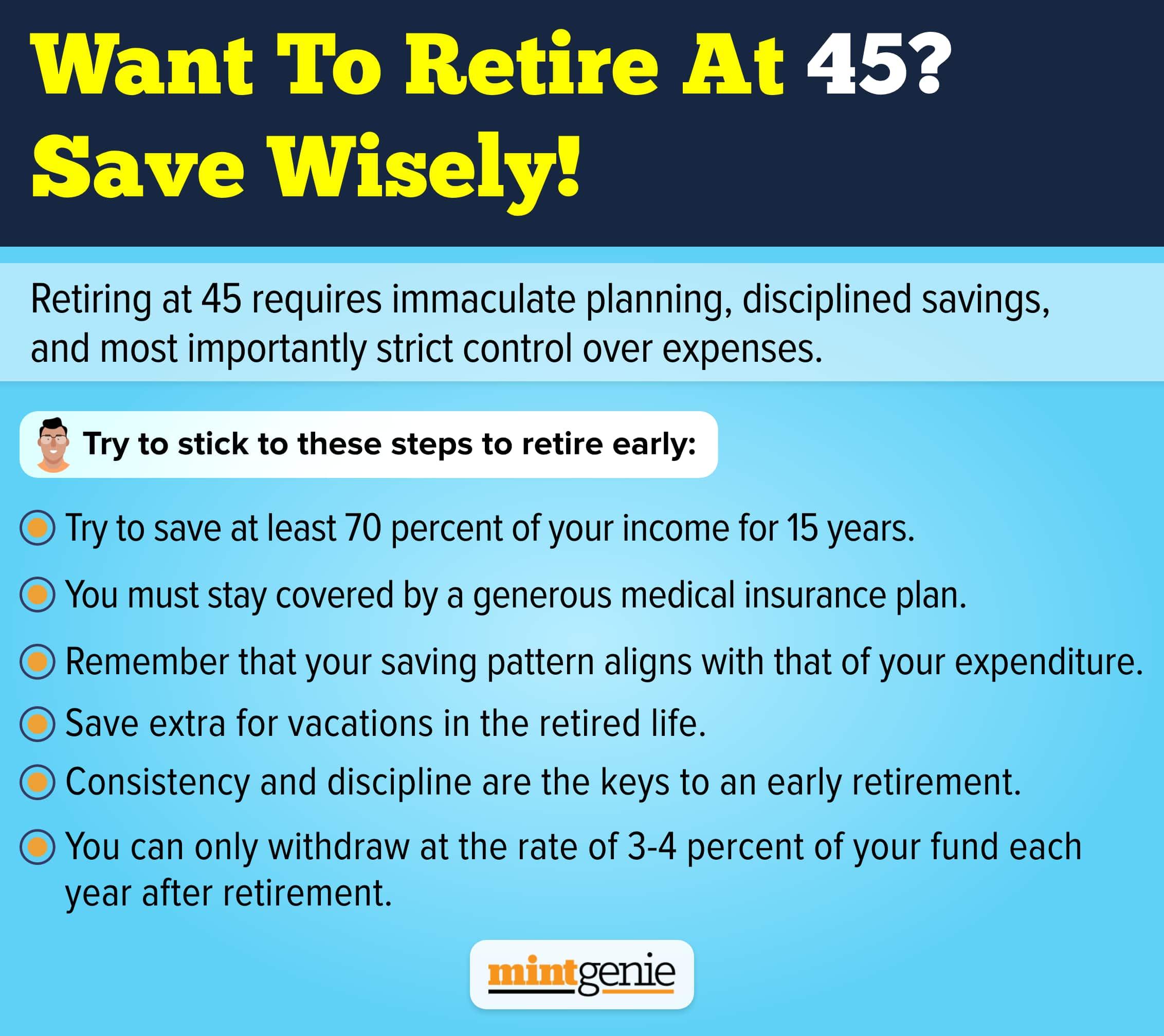

We all are apprehensive of what lies in the future. This explains well why we save and invest for our retirement. But then many people complain how they are already finding it difficult to save consistently owing to mounting expenses including children’s education, home loans and other necessary expenditures. Imagine salaried people with access to a regular income finding it difficult to meet their expenses? What would happen to them once they retire and will have no access to a regular income source? Depending on children is synonymous with collaborative living but expecting them to look after your post-retirement expenses out of deference and love is a big “No”. The aim must be to save and invest enough consistently from an early age so that there is enough time for the money to compound and grow into the much-needed corpus.

Prioritize your savings, as you will regret not having enough later. Having children does not mean that you will be looked after. With joint families crunching down into nuclear families, it is impossible to expect that your son or daughter can afford to pay toward your expenses too. The best way out is to determine how much money you may need after you have retired. There is no thumb rule to calculate one’s retirement corpus. Ideally, you must save at least 25 to 30 times your annual expenses. Rising costs consequent to the impact of inflation have necessitated the accumulation of retirement savings equivalent to at least 40 times the money you spend each year.

It’s okay if you are unable to deal with your finances. Not everyone is adept at financial planning. For this, you can start with hanging out with people who discuss finances and are willing to guide you with your investment plans. You can talk about your financial goals and the amount you would be able to set aside every month. They can then help you with information regarding the various investment plans and how you must allocate your money between equity, debt, gold, real estate and other options to gain maximum returns while saving on taxes too.

Build the right mindset. Everything starts with the mind, which is why deciding that you will be able to do what you had set out to do is important. It is okay to acknowledge your limitations and fears. For example, you may not earn enough to build a big house. Instead, buy a small comfortable flat with a home loan that you can pay off at nominal interest rates. This will save you from slogging your entire life from paying more on your interest at a prolonged tenure toward home loan repayment. Also, avoid buying big-ticket items that cause you to spend your money without yielding anything in return. If you are working remotely or from home, shift to a small city where the cost of living expenses would be far less.

Avoid relying on credit cards to buy things or pay for expenses. Credit card repayment involves huge interest payments if not paid back in time. This can cause a huge dent in your savings that you could have otherwise allocated to some high-interest investment option. Also, avoid making unnecessary expenses. Get rid of the superfluous mindset that prompts you to show off your money. Do shopping in moderation be it clothes, jewellery, household items or artefacts as there is no point in spending too much on them. Replace your habit of giving costly gifts with giving something that would ideally help them in their day-to-day lives.

Get rid to face the reality. That sense of entitlement wherein you feel your children are dutybound to look after you are retired is nothing short of folly. This is despite how much you do for them. There may not be a two-way street in every family, which means that you must prepare yourself for the worst when your children would want to move to a different city or state or country and raise their families there leaving you behind to fend for yourself.

Check for possible pension plans. Agreed that these plans may not be the best retirement tool, but you can still bank on them for a fixed month every month to pay off your necessary expenses. Alternatively, you can park some money in the National Pension Scheme (NPS) which yields market-linked returns while giving you the dual benefit of a monthly pension and tax deductions. You may invest in balanced mutual funds or retirement plans that park only a part of your money in equities leaving the rest to earn from debt instruments.

Last but not the least, avoid feeling entitled to what your children earn. Parents must look after their children and vice versa, but in most cases, the latter may not happen owing to many reasons. So, if you are planning your retirement, do not assume your children to part with a part of their earnings for you or deposit a fixed amount in your account regularly. You have to seek and make provisions for yourself. Settle down your savings in a way that there is no scope for disputes among your family members regarding the right to heritage.