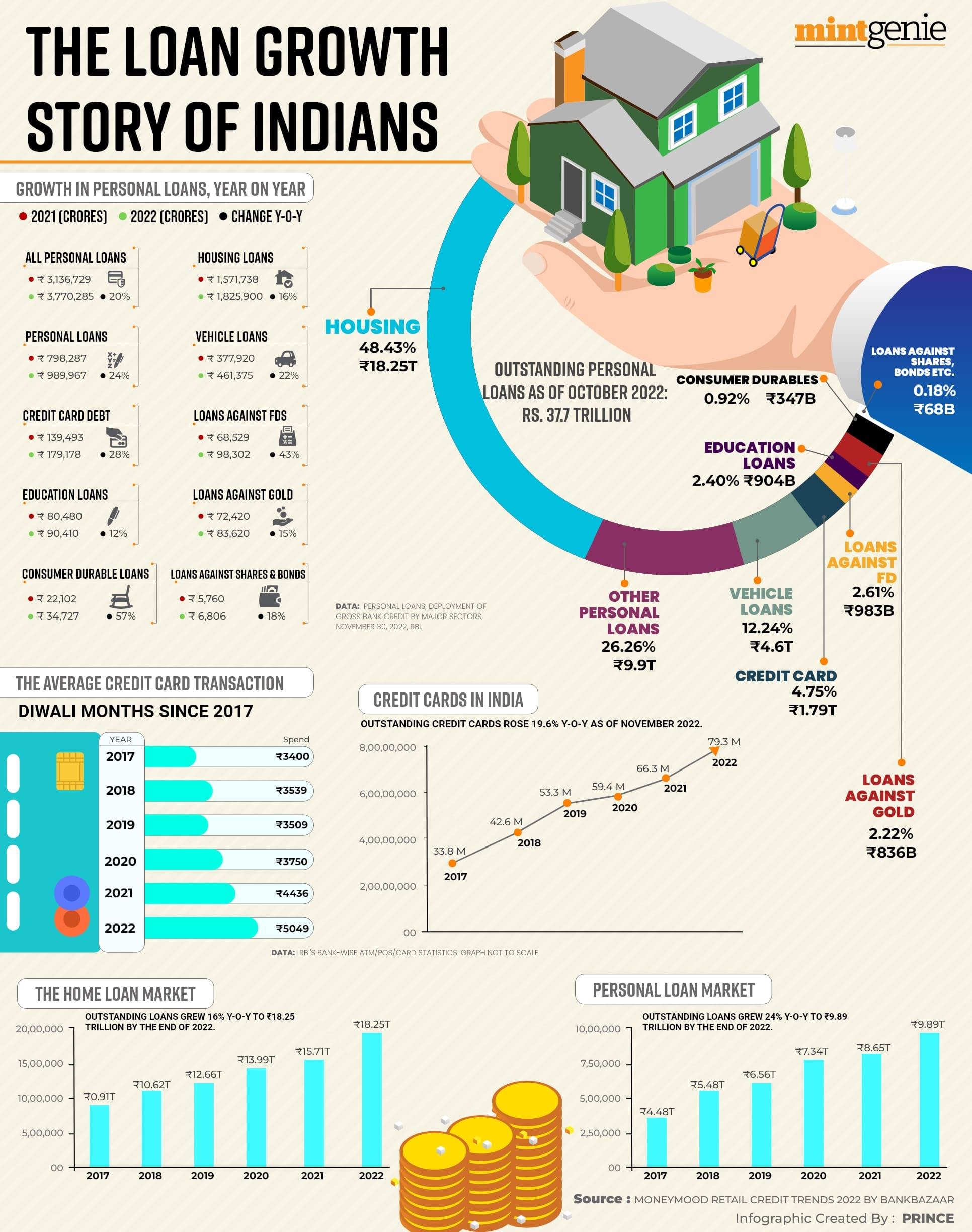

Owning a house is everyone’s dream. We all work hard in our lives to achieve our dreams. However, it is not easy today to buy a house in metro cities. Prices of residential real estate units have gone up like anything. It is nearly impossible to pay the full price of the house unless one has huge savings already. For a middle-income earner, the only visible choice is taking a home loan and paying it back over the years. Applying for a home loan has its own set of rules and requirements.

In this article, we are going to discuss all you need to know about joint home loans. As the name simply suggests, a joint home loan is a loan which is taken jointly with another person, usually spouse or parents. There are multiple reasons as to why people apply for joint loans rather than individual loans, some reasons are:

Increased loan eligibility: When two people apply for a home loan together, their combined income is used to calculate the loan amount. This can lead to a higher loan amount being approved, which can be helpful if you are looking to buy a more expensive home.

Creditworthiness: This applies to all types of loans, the lenders always check your credit score before deciding the eligibility in terms of loan amount, tenure, and interest rate. It is easy to avail the loan if you have a strong credit history in terms of timely repayment.

However, if your credit history is not very strong, a co-applicant can be added to the loan proposal so that bank can have additional comfort about the loan proposal and there would be two people involved in repaying the loan rather than single person exposure.

Shared responsibility: When you take a home loan jointly, both borrowers are equally responsible for repaying the loan. This means that if one borrower is unable to make a payment, the other borrower is still obligated to do so. This can be a good option for couples or other partners who want to share the responsibility of owning a home.

Lower interest rate: Some lenders offer lower interest rates on joint home loans. This is because they are considered to be lower-risk loans, as there are two borrowers who are responsible for repaying the loan.

Tax benefits: As per the income tax regulations, joint home loans allow both co-borrowers to claim tax benefits under Section 80C as well as Section 24.

- Section 80C: Amount of principal repayment can be claimed under this section up to Rs. 1.5 lakhs per annum by each of the co-borrowers.

- Section 24: Amount of interest paid as a component of EMI can be claimed under this section up to Rs. 2 lakhs per annum by each of the co-borrowers.

There are also multiple disadvantages of having joint home loan, some of these are:

Default by a co-borrower: If one borrower defaults on the loan, the other borrower may be held liable for the entire amount. Additionally, the credit score is affected negatively for both the borrowers even when another co-borrower has been paying on time.

Separation: Usually the joint home loans are availed by married couples. This can raise all sorts of legal problems if the co-borrowers are married to each other and get separated by divorce even as the home loan remains to be repaid. To further complicate the issue, If the property is registered in the name of one co-borrower, then after the loan has been fully repaid, he/she will become the rightful owner even if the other co-borrower has also paid their share of the EMIs.

Credit score: Default by any one of the co-borrowers affects the credit score of all the borrowers. This impairs the ability of a genuine borrower to borrow in future.

Few things that should be kept in mind before applying for a joint home loan:

- Do not apply for a joint loan just for the formality. Usually, banks ask for a co-borrower just to reduce their risk. However, if your credit score is decent and your income eligibility allows for a required loan amount then you should not involve a co-borrower unnecessarily just for the sake of formality.

- Do not apply for a joint loan just for the sake of tax deduction. Dual tax deduction might sound tempting but in case of separation or disputes, it could affect the title of property and make it difficult to sell due to legal complications.

- Do not apply for a higher loan amount just because you can do it with the help of a co-borrower. Always keep in mind that the EMI amount should be well within a reasonable limit that can be paid out in due course. Once you borrow money from a bank, there is no turning back.

Rohit Gyanchandani is Managing Director at Nandi Nivesh Private Limited