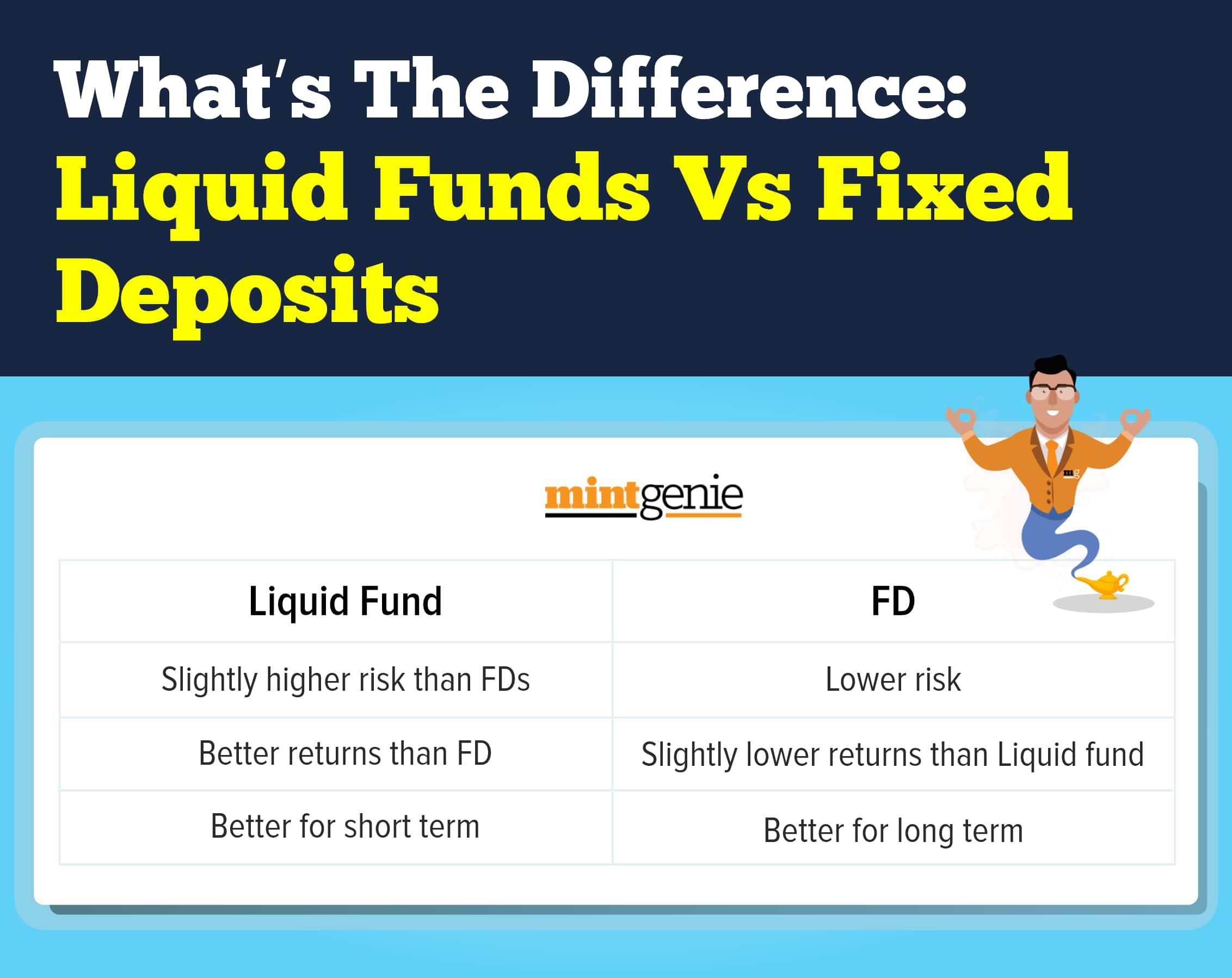

It always serves best to have a contingency fund in place that has scope for liquidity when needed. Many people for this purpose allow their money to sit idle in savings accounts or parked in fixed deposits with hardly any expectation of high-interest rates. Add to it the effect of inflation, the returns earned from them post taxes are negative.

It makes sense to explore these alternate investment options with so many funds that promise quick liquidity at better interest rates. Parking money in these funds allows us the benefit of immediate liquidity during contingencies. The exit option is easy, thus, allowing investors the benefit of quick money availability whenever needed.

What are liquid funds?

As opposed to equity funds that are most sought after for their high returns, liquid funds are comparatively lesser-known funds among investors. These invest in short-term assets including treasury bills, government securities, certificates of deposits and commercial papers. The Securities and Exchange Board of India (SEBI) mandates investments in liquid funds to be limited to only debt and money market instruments with maturity dates not exceeding 91 days. The SEBI norms do not permit investments in risky assets as they aim to contain the risk element in the liquid fund portfolio.

How much returns you earn on liquid funds depend on the market prices of the securities held by the fund. The earnings from liquid funds mainly depend on the interest payments on their debt holdings with a minor percentage being generated via capital gains. These funds are of short-term nature, which means that their prices are less likely to fluctuate compared to long-term bonds or other investment options. Compared to debt funds, liquid funds are less affected by rising interest rates in a changing market scenario. This explains why liquid funds are comparatively more stable than other debt funds. While most liquid funds process the redemption request within one working day, some offer instant redemption too.

Does exit loads on liquid funds matter?

Like all other funds, there is an exit load on liquid funds if redeemed before the maturity date. However, should exit loads deter one from investing in liquid funds for less than a week? This is a question that has been asked repeatedly as many liquid funds announced exit loads ranging between 0.0045 per cent and 0.007 per cent if the money is redeemed within seven days of being invested. The exit load is structured in a way that it reduces with every passing day of investment. This means that if the money is redeemed within a day of investment, the mutual fund houses would charge 0.0070 per cent of the investment while the same drops down to zero if the money stays invested for more than a week.

For example, if you invest ₹50,000 in liquid funds and exit just after five days with absolutely no returns earned on them, you have to pay only a negligible exit load of ₹2.50. Exit loads announced to deter investors from taking out money from their liquid funds immediately do not impact much on the returns earned on the funds. This is because even after factoring in the exit loads, investors continue to earn decent earns on liquid funds, which is way more than the overnight funds with investment tenures of three days or more.

So next time, you are thinking of parking your extra money in a fund that allows you to redeem early sans any hassles, you may consider investing in a liquid fund than limit your knowledge and investments to bank accounts alone.