India will observe the “National Insurance Awareness Day” on June 28 this year, thus triggering the need to learn about insurance and include them in their investment portfolios. Not many people are aware of the essence of buying life insurance or health insurance or investing in them to secure their financial future.

Buying life insurance is essential as investing in health insurance considering the fragility of life and the proclivity to suffer from sudden diseases. Take, for example, the effect of the sudden and unprecedented nature of the Covid-19 pandemic, that caused many people to lose their loved ones while others continued to seek prolonged treatment at various hospitals. The hospital bills forced many people to dig into their savings and utilise their emergency corpus, thus reiterating the need to have a health insurance plan in place.

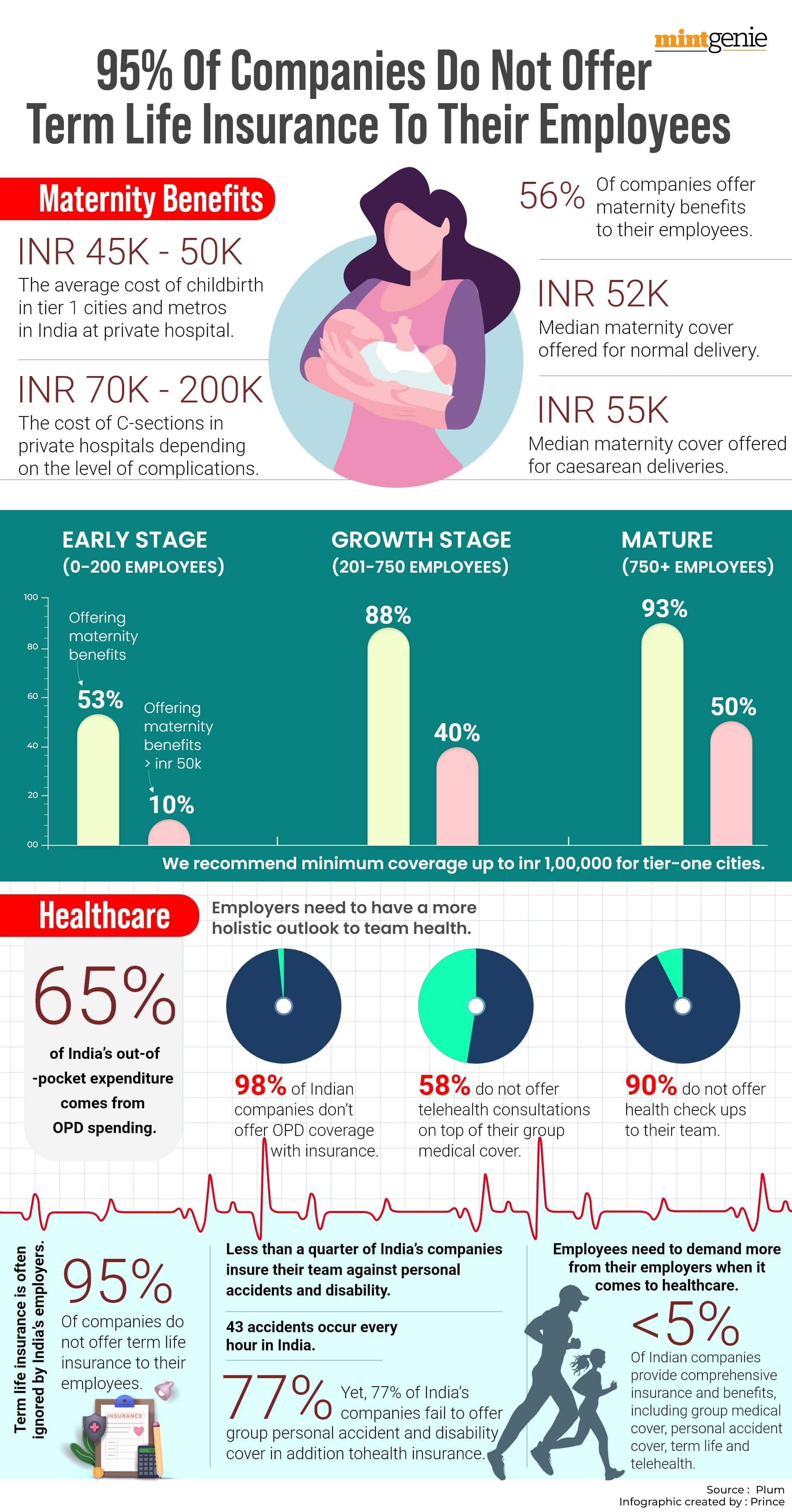

For example, the idea behind buying health insurance is to ensure a protective financial shield that will pay for your hospitalisation and treatment expenses, when needed. Every day brings forth new revelations of escalating medical inflation and emerging health emergencies. Many people complain how it is the out-of-pocket expenditure that bugs them more than the actual hospitalisation costs. This can be attributed to their higher frequency and different parameters set by health insurers regarding these costs.

The health insurance industry is continuously evolving, offering a wide range of options in the market today to reduce out-of-pocket medical expenses. However, before delving into methods to minimise these expenses, it is crucial to grasp the definition and impact of out-of-pocket expenses on policyholders.

Defining out-of-pocket expenses

Health insurance policies provide a multitude of advantages to policyholders, offering coverage for the expenses incurred during medical treatments. However, it is important to note that certain expenses may not be covered by health insurance, necessitating the need to pay for them out of pocket. Therefore, even with a health plan in place, these medical expenses can accumulate significantly if one fails to plan ahead and secure a comprehensive policy.

Upon careful examination of the policy's details, individuals may come across certain exclusions. One notable example is the omission of consumables from coverage, which refers to medical aids and equipment that are disposed of after use. These typically include items like PPE kits, syringes, gloves, and more. Furthermore, traditional health insurance plans have traditionally excluded Out Patient Department (OPD) costs from their coverage.

When selecting a policy with deductibles, the insurance company will only cover expenses once you have personally paid the deductible amount out of pocket. Similarly, if you have chosen a policy with co-payment, you will be responsible for bearing a certain percentage of the bill.

For example, if your policy has a coverage limit of ₹5 lakh and a deductible of ₹1 lakh, you will need to initially pay ₹1 lakh from your own pocket before the coverage comes into effect. Likewise, if you have opted for a 10 per cent co-payment, you will need to pay ₹50,000 during the claim settlement process.

Many people find it difficult to differentiate between “deductibles” and “out-of-pocket” expenses. Each year, before your insurance company begins covering your medical expenses, you are responsible for paying a certain amount known as the deductible out of your own pocket. On the contrary, “out-of-pocket” expenses refer to the expenditure you must incur despite having bought health insurance since the same is not covered in the policy.

And, there are some out-of-pocket expenses that you must pay since the amount exceeds that stipulated in the policy. For example, certain health insurance providers establish limits on specific expenses they will cover, such as room rent and ambulance fees, based on the policies purchased. If the total cost of these items exceeds the specified limits outlined in your policy, you would be responsible for covering the additional expenses, even if you have not utilised all of your insurance funds.

How to minimise out-of-pocket expenses?

One way out is to choose the right health insurance policy that covers maximum costs at reasonable premium charges. This is because health insurance companies are continuously refining their products to cater to the needs of their customers. Consequently, a wide array of options is now available in the market, which, if carefully selected to personalise your health insurance plan, can significantly reduce your out-of-pocket expenses.

Here are some key aspects to consider when reviewing your plan, some of which include:

OPD coverage

In the present-day scenario, many insurance plans offer the option of including OPD coverage either as an add-on or as an inherent feature. This inclusion expands the coverage of health policies to encompass OPD costs that were traditionally excluded from standard plans. Previously, health insurance plans required patients to be hospitalised for a minimum of 24 hours to be eligible for claims. Consequently, they did not account for routine doctor visits or the expenses of treatments that did not necessitate hospitalisation.

Such out-of-pocket costs can accumulate significantly over the course of a year. Thus, it is prudent to consider adding the OPD cover as an add-on to your policy. An OPD cover often includes the payment for diagnostic tests, pharmacy expenses, dental treatments, and hearing or visual aid equipment, thereby further reducing out-of-pocket expenses.

Consumables cover

The cost of consumables during hospitalisation is a significant out-of-pocket expense that often places a heavy financial burden on the patient's family. Typically, insurance policies do not cover these expenses. However, many modern insurance plans now offer the option of consumables cover, which includes the cost of various items such as syringes, PPE kits, sutures, needles, catheters, cotton, bandages, medical gloves, masks, gowns, sanitisers, and more.

Considering that these expenses can accumulate significantly for prolonged hospitalisations related to serious illnesses, having a consumables cover becomes crucial. By including this coverage in your policy, these expenses will be taken care of, relieving you of the financial burden. Additionally, such policies may also cover administrative charges like the cost of admission kits, birth and death certificates, documentation expenses, visitor's pass charges, and similar expenses.

No limit on capping

In addition to the essential add-on features mentioned earlier, insurance plans have evolved to include various options that help policyholders reduce additional expenses. For example, a hospital cash cover provides a fixed daily allowance to the insured individual, which can be used to cover expenses that may not be covered by the health insurance policy. Opting for plans without sub-limits and deductibles is also recommended, as it allows you to fully utilise the sum insured as long as the total medical expenditure does not exceed it.

As medical expenses continue to rise, it is important to be prudent when choosing health plans in order to minimise extra costs. It is also beneficial to compare different policies, features, and premiums online to find a plan that suits your budget. By following these guidelines, you can effectively reduce your out-of-pocket expenses.