The recent data published by the Reserve Bank of India (RBI) highlights the continued growth in credit card spending by Indians. According to recent statistics from the country’s Central Bank, credit card spending in May of this year reached a significant milestone, hitting a record high of ₹1.4 lakh crore. This figure highlights the growing trend of credit card usage and indicates a substantial increase in consumer spending through credit cards during that period.

An analysis of the data reveals that the total spending or outstanding dues on credit cards, which remained relatively stable throughout the previous fiscal year, have been steadily increasing by five per cent month-on-month in the current year. This indicates a sustained upward trend in credit card usage and highlights a consistent growth in consumer spending through credit cards.

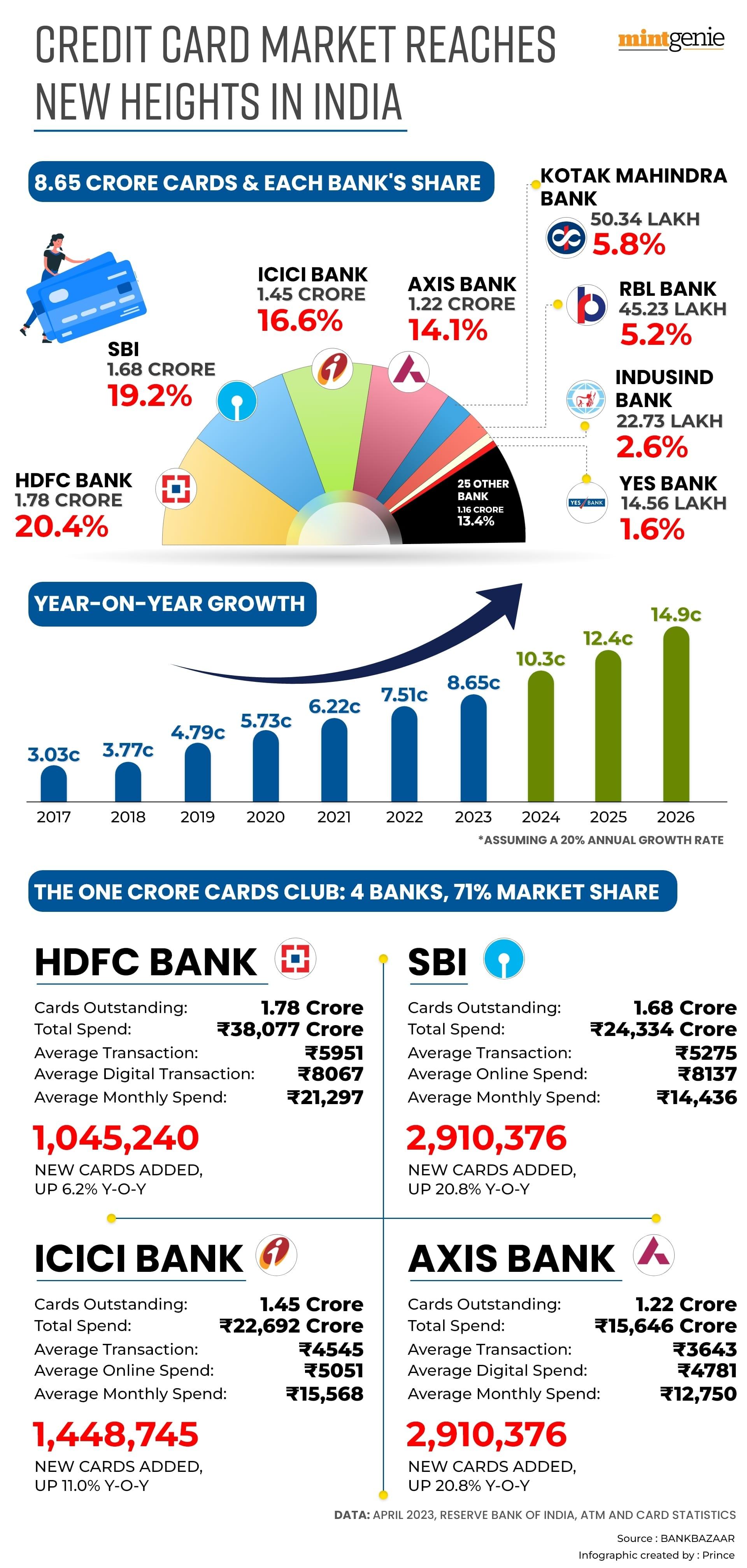

Likewise, the number of active credit cards has surged by over five million since January, surpassing 87.4 million during the reported month. This marks a new record high in May, as per the data provided by the RBI. The increase in the number of credit cards in circulation further underscores the growing popularity and widespread usage of credit cards among consumers apart from an increased credit card burden in recent times.

Growing credit card debt, if continued unchecked, can spell doom. Apart from the high-interest rates that one must pay, credit card companies also charge annually, thus, highlighting added expenses for credit card users. Credit card purchases are on the rise. These underscore the growing dependence on credit to pay for products or services that one cannot normally pay for.

Personal loans versus credit card debt

The aggravating effect of credit card debt has caused many people to inquire if applying for a personal loan would be a more effective option than paying using credit cards. Undoubtedly, personal loans often offer more favourable interest rates compared to other borrowing options like credit cards and credit card cash advances. This advantageous aspect of personal loans can lead to long-term savings, while still granting you the freedom to utilise the funds according to your individual needs and preferences.

A personal loan can be utilised in various ways to help you retain more money. These include consolidating high-interest credit card debt, financing significant expenses, and even using it as a tool to improve your credit score, which can enable you to access more favourable interest rates for future borrowing. By leveraging a personal loan strategically, you can optimise your financial situation and maximise your savings potential.

Should you take a personal loan?

Any and every kind of loan is a liability that must be rid of within the stipulated period. With a vast range of both private and public lenders on the web, applying for a personal loan is now easy with just the click of a button. However, the easy availability of personal loans should not translate to applying for them rampantly.

“When should you use a personal loan?” is a question that you must ask yourself before applying for one. Though there is no thumb rule stating rules regarding personal loan application and its usage, deciding whether to use a personal loan depends on your specific financial circumstances and objectives.

For instance, opting for a personal loan can be advantageous if it enables you to reduce high-interest credit card debt by securing a lower interest rate compared to your current one. Additionally, utilising a personal loan could be a wise decision if it assists in financing a home improvement project that enhances the value of your property. Ultimately, the appropriateness of a personal loan hinges on how well it aligns with your financial goals and helps optimise your overall financial well-being.

Getting a personal loan can indeed help you to save money in many ways. These include:

Credit card debt consolidation

Consolidating high-interest credit card debt is one of the primary purposes for obtaining a personal loan. Personal loans generally offer lower average interest rates compared to credit cards, which often carry high-interest rates. To secure the lowest rates, having a high credit score is typically required. However, if you're seeking a prompt debt resolution and don't have the time to wait for your credit score to improve, you can consider applying for a loan with a co-signer or co-borrower who has good credit. This increases your chances of qualifying for the best rates.

By obtaining a personal loan with a lower interest rate, you can reduce your monthly interest charges and overall loan costs. These savings can provide you with additional cash flow that can be directed towards paying down the principal debt more rapidly. Ultimately, using a personal loan to consolidate high-interest credit card debt can help you save money and expedite your journey towards becoming debt-free.

Paying for a huge expenditure

Personal loans offer great flexibility as lenders generally allow you to utilise the funds for a wide range of purposes. Whether you need financing for a dream vacation, wedding expenses, purchasing a boat, or covering a one-time medical procedure, a personal loan can be used to address these specific needs. The versatility of personal loans enables you to access the necessary funds to fulfill various financial goals or tackle unexpected expenses.

Before opting for a personal loan to finance a want rather than a need, it is crucial to calculate your loan payments to ensure that you can comfortably repay the loan without jeopardising your budget. Utilising a loan calculator can be helpful in this regard.

This approach can save you money for several reasons. Firstly, by using a personal loan instead of a credit card to finance a significant expense, you may secure a lower interest rate, resulting in potential savings. Additionally, personal loans offer the advantage of providing cash upfront, potentially allowing you to negotiate better deals based on how you plan to use the funds. By strategically choosing a personal loan for your specific purpose, you can maximise your savings and financial outcomes.

Getting rid of high-interest debt

If you find yourself grappling with high-interest debt, a debt consolidation loan can be a viable solution to reduce interest expenses and expedite debt repayment. Ideally, the interest rate on the new loan should be lower than your current rate, resulting in overall savings on interest charges.

To potentially save hundreds or even thousands of dollars in interest, consider paying more than the minimum amount due each month. However, ensure that your lender does not impose any prepayment fees before implementing this strategy.

Alternatively, you can focus on paying down your debt using the debt snowball or debt avalanche method as an alternative to taking out a personal loan. Depending on your specific debt situation and financial circumstances, this approach may prove more effective than acquiring additional debt to pay off existing obligations.

By consolidating multiple debts into a single loan with a lower interest rate, you can diminish the monthly interest charges you incur. This step may also generate some additional cash within your monthly budget, which can be allocated towards faster debt repayment, ultimately saving you significant amounts of interest over the loan's duration.

Improved credit score

In addition to saving money, a personal loan has the potential to improve your credit score. When you carry a high balance on your credit cards and approach your spending limit each month, your credit utilisation ratio increases. This can raise concerns among lenders as it indicates a higher level of risk. Consequently, high-risk borrowers often face higher interest rates, resulting in more expensive borrowing in the future.

However, personal loans can be beneficial for managing credit utilisation by using the loan proceeds to pay off your credit card balances. This action can help reduce your credit utilisation ratio and potentially improve your creditworthiness, thus, making future borrowing more affordable.

When it comes to choosing between a personal loan and credit card debt, it is the utility, eligibility, cost, and availability that matter. However, youth seeking immediate gratification must avoid applying for personal loans for frivolous reasons.

No doubt, personal loans offer various avenues for saving money. Nevertheless, it is crucial to exercise caution and avoid taking on a loan beyond your means, especially for wants rather than essential needs. Assuming such a loan could potentially lead to financial hardship and harm your credit if you fail to make timely payments or default on the loan. It is advisable to carefully assess your financial situation and borrow responsibly to maintain a healthy credit profile and avoid detrimental consequences.