If you are a new investor, you must have heard many times on business channels or perhaps read in the pink newspapers that bond prices moved downward after RBI raises key interest rates.

Else, you may have also heard that after rate cuts, the bond prices rose and their yields declined.

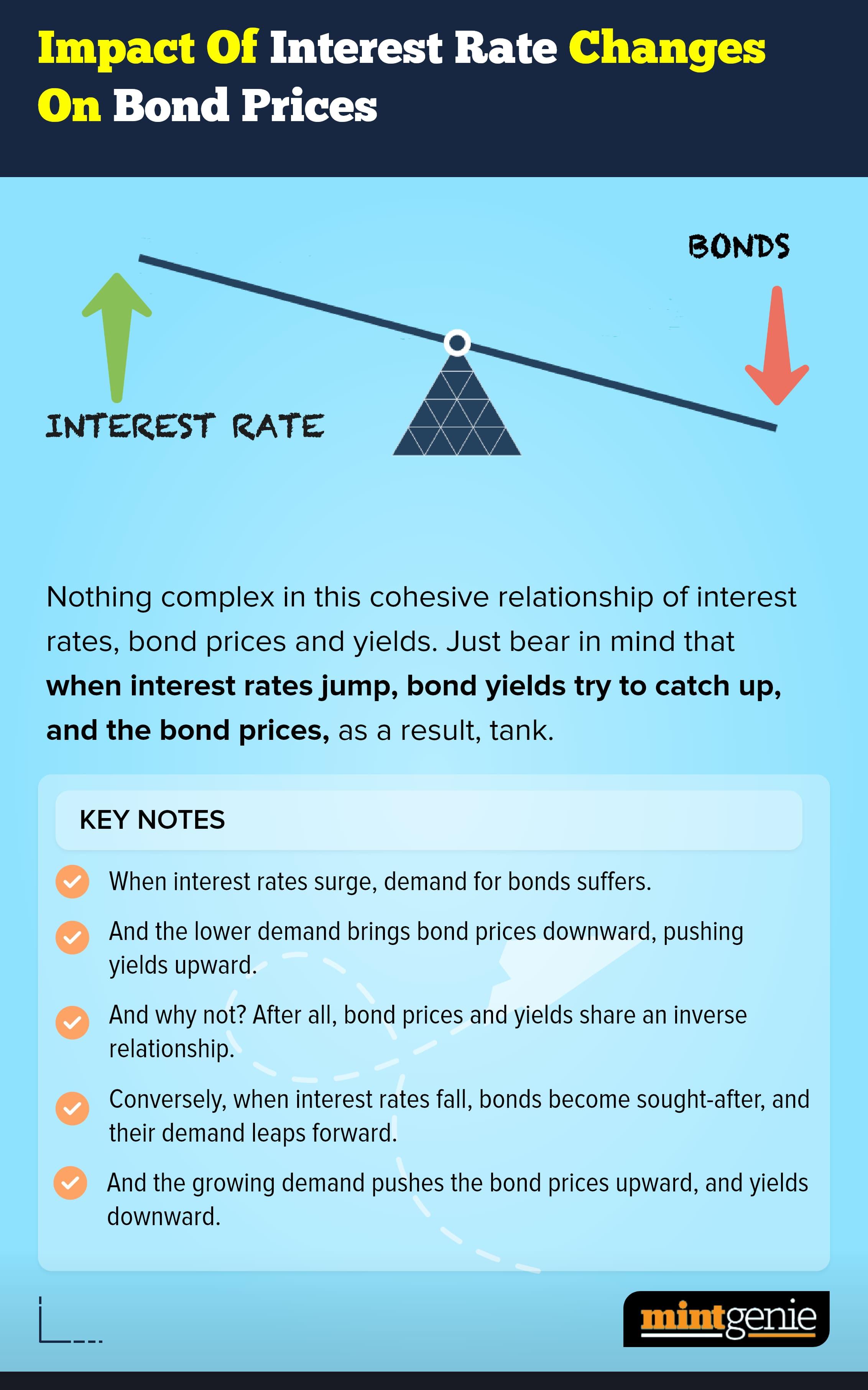

One might wonder what is the unique and harmonious relationship between the three interconnected strands of the bond market – interest rates, bond yields and prices.

We try to deconstruct the relationship here for you:

At the time of issuance of bond

When bonds are issued, say by the Government of India, they are sold at a coupon rate, which is also known as rate of interest. The coupon rate is decided at the time of auction of bonds. The benchmark bond is the debt security issued for a period of 10 years by the Government of India.

When the bonds are issued, the coupon rate is in consonance of the prevailing interest rates in the market. For instance, when the average borrowing cost in the market is 6 percent, the government will not pay more than this to borrow money. At the end of the day, a government bond is a loan taken by the government for which it incurs a cost. And the cost is the interest earned by the bondholder.

So, the bond prices and coupon rate reflect the market reality at the time of issuance of bonds. Now, let us understand what happens afterwards when the interest rates fluctuate, which more likely than not, will happen during the bond’s tenure.

Interest rates fall

Let us imagine that the interest rates fall soon after the bonds were issued at a higher rate of interest. In this case, there is likely to be more demand for the bonds because of the relatively higher coupon rate offered than the prevailing interest rates in the market.

Any prospective investor will gladly pay a premium to buy the bond to be able to earn extra interest that the bonds accrue.

For instance, ₹100 bond with 10 years maturity bears a coupon rate of 10 percent per annum. Soon after the issuance, interest rates decline to 8 percent per annum, the investors would be willing to pay a premium to buy bonds that pay an extra 2 percent (10% - 8%) than the prevailing interest rates. So, you can say that the bond will trade at a premium to the par.

When bond prices rise, the bond yields fall. They share an inverse relationship. For instance, when a ₹100 bond with a coupon of 10 percent is sold for ₹100, its yield is 10 percent. But when it is sold for a premium of ₹120, the coupon and tenure – for obvious reasons – do not change. So, the bond yield (coupon rate /bond price) will fall to 10/120 = 8.3 percent.

In this case, the bond holder earns ₹10 after investing ₹120, so the investor’s bond yield falls to 8.3 percent from 10 percent earlier when bond was sold for ₹100.

Let us now pull together the threads spun so far.

When interest rate falls, the bonds which were issued at a relatively higher rate of interest become hot in demand and their prices start to rise.

When a new investor buys the same bond for a higher price, its yield will be less because the tenure is the same and the coupon is calculated at the face value, which also remains the same.

Interest rates rise

Now let us imagine that the interest rates rise to 13 percent soon after the bonds with 10 percent coupon rate were issued. Now, what will happen?

The bond holders will likely get restless and would want to take part in the higher interest rate cycle by disposing off low-interest bearing bonds.

When the bond holders want to sell these bonds in the market, there will be fewer buyers because other debt instruments would be offering an extra 3 percent (13% - 10%) vis-à-vis bonds.

So, the bond prices would go down to woo the potential buyers. This means the bond is trading at a discount to the par.

And now the new investor has paid less money for the same coupon rate (10%), the bond yield will naturally rise.

For instance, let us suppose a ₹100 bond is sold for ₹80 because the interest rates have risen and the existing coupon rate of 10 percent obviously stays the same. The bond yield will be ₹10/80 X 100 = 12.5 percent.

So, in this case, the new investor is able to earn ₹10 by investing only ₹80, (against ₹100 by the previous holder) which fetches him a yield of 12.5 percent per annum.

We can summarise that bonds are sold for premium during falling interest rate cycles, leading to lower bond yield.

On the other hand, when interest rates rise in the market, bonds are sold for discount, precipitating a higher bond yield.