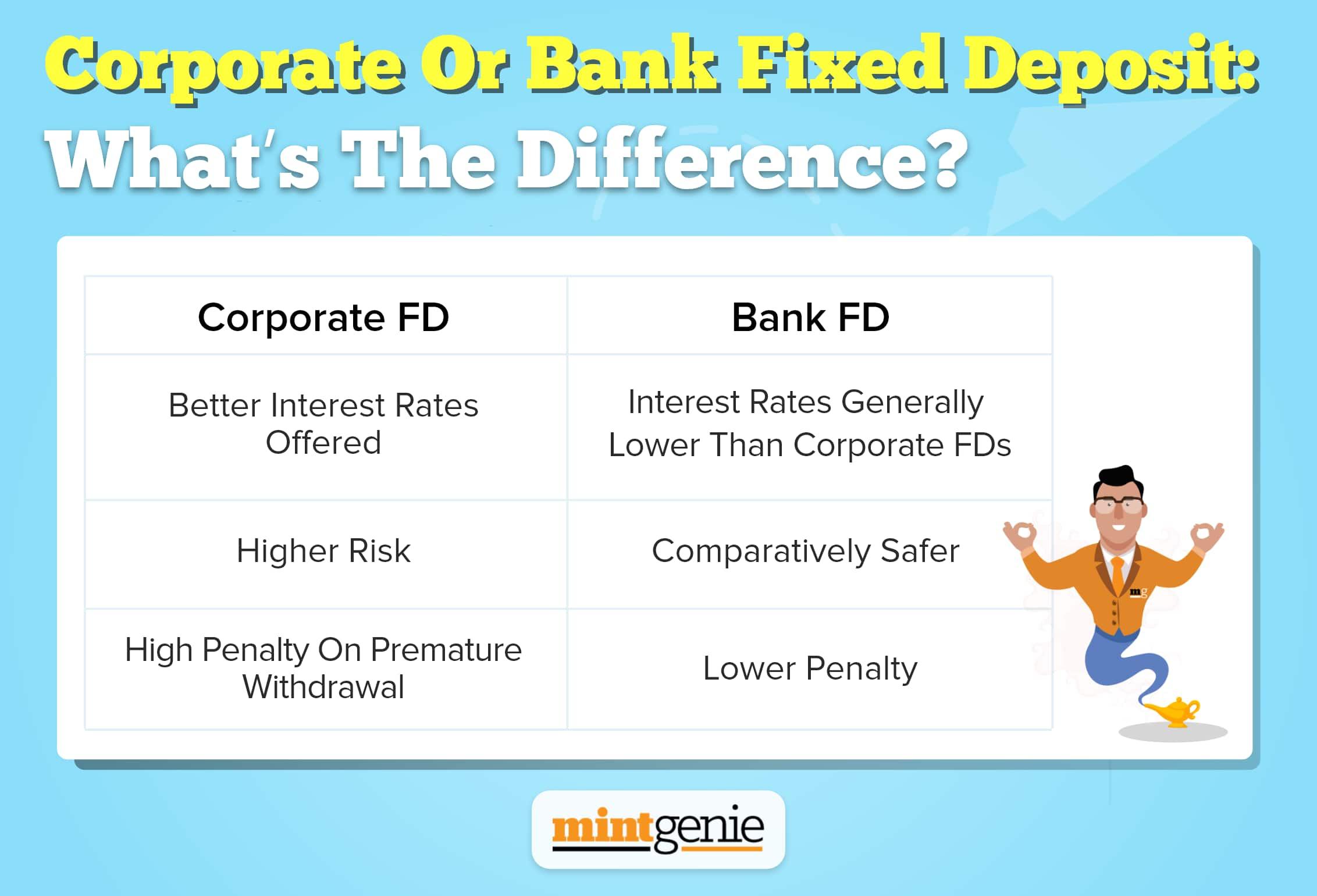

Fixed deposits have always been a popular choice as it provides the benefit of assured returns and has low-risks. There are broadly two types of fixed deposits, one being the most known which is offered by the banks which have lower risks.

While the other one is corporate fixed deposits which offer high interests but have much higher risks when compared with bank fixed deposits.

It has been seen that investors are pretty clear when it comes to returns on FD, but risks associated with FDs are still less clear. Therefore, the article is based on discussing the risks associated with investing in fixed deposits:

Liquidity Risk

It is very well known that a fixed deposit makes availability of funds easy, however not all fixed deposits have high liquidity. For example, a tax saver FD has a lock-in period of five years because of which the investor cannot liquidate the funds before the maturity.

Also, if a certain bank does not have the facility of online liquidation then the individual might have to visit the branch and fill out paperwork in order to liquidate funds out of their fixed deposits.

Default Risk

There have been some cases by the small cooperative banks of defaults, in situations like these investors are usually prone to vulnerability. It has been noted that under a new rule, investors can have a deposit insurance of upto Rs. 5 lakh per account but any amount above this is subject to default risk.

Inflation Risk

It is an unsaid truth that inflation affects every investment and thus increases the risk. For example, if a FD gives 8% interest and inflation rate at the moment is 6% then the real returns earned are just 2%. It is true that interest on FDs are fixed and have no effect on market fluctuations, but the real returns increase or decrease according to inflation.

High Taxation

Fixed deposits interest earnings may be completely taxable unless you’re over 60, where up to Rs. 50,000 is exempted under Section 80 TTB. Your interest earnings are combined with your income and taxed as per your slab.

Therefore, if you’re in the 30% tax slab, a 7% FD may effectively be providing you only 4.9% returns further diminished by rising inflation.

Reinvestment Risk

To discuss this particular risk, let us raise a question - What happens after a FD matures? So, there are two options an investor can choose from as and when a FD matures - either withdraw the money or extend the FD.

The investor can get a new FD but only at the rate which is applicable right now. This can result in jeopardizing your long-term financial goals as you cannot reinvest money at a lucrative rate of returns.

Even though the article discusses risks associated with fixed deposits, the investor should still take a note that they are a great source of income when the amount is invested for long-term purposes.

The risks associated with the scheme are still less when compared to other investment options. Therefore, investors should definitely try investing in the scheme with thorough knowledge of the market and the scheme.