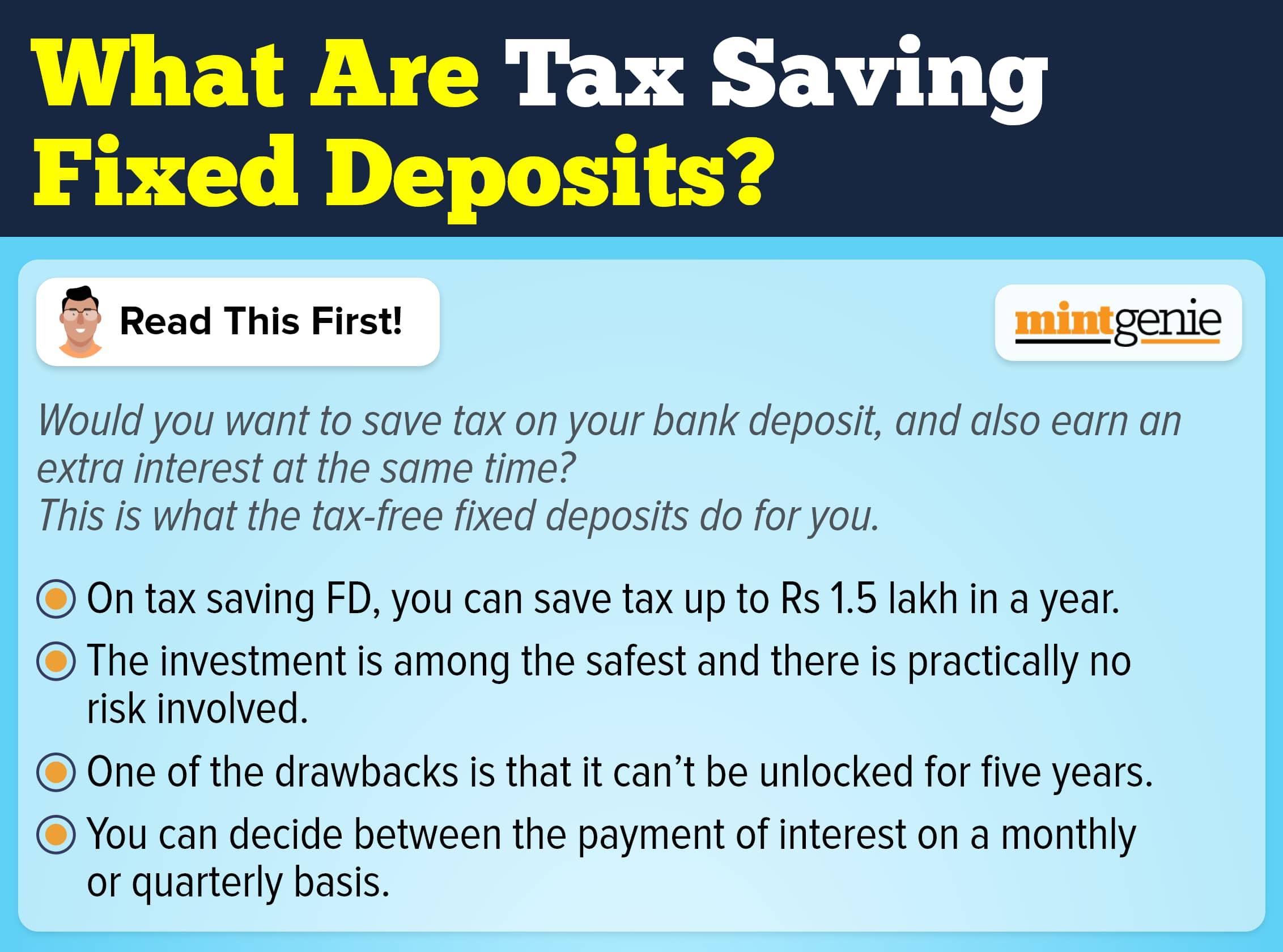

Check out the interest rates earned by banks and you will find how the Reserve Bank of India (RBI)’s stance to keep the repo rates unchanged has encouraged many banks to continue accepting deposits at high-interest rates. Take, for example, DCB Bank is now offering eight per cent interest on its fixed deposits (FDs). Similarly, Suryoday Small Finance Bank (SSFB) has revised its interest rates to 9.5 per cent while regular customers of Unity Small Finance Bank also earn somewhere around nine per cent interest on their deposits with the bank.

While the high-interest rates on these fixed deposits may look enticing at first sight, bank account holders often wonder if they are worth the risk. No doubt, these small finance banks are regulated by the RBI, investing in them is considered riskier than putting money in traditional scheduled commercial banks. The quandary persists about selecting the right bank before depositing the money into an FD scheme. Nevertheless, there are specific criteria that one can contemplate before investing in an FD scheme.

Credibility matters

Remember when our elders said, “Your reputation must precede you”. They were not wrong considering how perception about your business has a deciding effect on your credibility. This holds true for banks too that are involved in handling transactions worth lakhs of rupees each day.

Primarily, choose a bank that has a commendable history of providing stability and dependability. To appropriately evaluate a bank's financial standing, one can examine its financial statements, annual reports, and other financial indicators.

Another approach is to verify the financial ratings assigned by reputable agencies like ICRA or CRISIL. For instance, individuals can refer to CRISIL’s FAAA rating and ICRA’s MAAA rating when selecting a specific FD scheme.

Check regularly for interest rates

This aspect should also be taken into account when selecting a specific FD scheme. The interest rate represents the percentage that a bank or financial institution will pay to an individual for holding funds in their FD scheme. Typically, FD schemes with longer tenures tend to offer higher interest rates.

Hence, it is essential for individuals to assess their financial goals and select a tenure that aligns with them, while also comparing the interest rates offered by different banks for that particular duration.

Are there penalties for premature withdrawals?

In cases of premature withdrawal, which occurs when an individual withdraws their funds before the FD’s maturity date, some banks may impose a penalty. The penalty amount can vary and is typically calculated as a percentage of either the interest earned or the principal amount.

Is the bank covered under the deposit insurance scheme?

The Deposit Insurance and Credit Guarantee Corporation offers deposit insurance of ₹5 lakh per account holder per bank, encompassing both the principal and interest. To safeguard one's bank deposits, it is crucial for an investor to verify whether the bank is registered with the insurance provider. Based on this information, they can make an informed decision regarding their deposit.

Once you have made your choice of bank, it is for you to decide what kinds of investments you wish to pursue with the bank. You may opt for FD investments, though investing in one go may backfire in the long run. Instead, opt for the FD laddering technique where you invest your money in small batches of differing tenures. This allows investors to stay invested in gaps of equal tenure.

For example, if you have ₹5 lakh in your hand, you may divide the amount into five different batches to invest in five different FDs. One FD may mature after a year, the second may mature after two years, the third may mature after three years, and the fourth and fifth batches will mature after four and five years, respectively. This allows for some cash in hand after a definite tenure even when the remaining amount stays invested in high-interest FDs.