Whenever the salary is increased, one must increase investments by the same percentage. In an interview with MintGenie, Girirajan Murugan, CEO, FundsIndia shares how one must step up emergency corpus along with the rise in inflation.

Edited Excerpts:

Q. How should people get started with saving money in their bank accounts?

Start a separate account - could be a savings account, FD, or RD. Analyse all the rates and schemes/accounts available in the market and go for the one that suits you best. Most people use a single account for everything. The problem here is easy accessibility - a whole lot of transactions cloud you from seeing how much you actually save. A separate account helps you see your actual savings, and is not a confusing mess of transactions.

Q. What are the common barriers to saving enough money?

Temptation - You have a surplus of ₹500. You might be more tempted to spend it on outings than to direct it to your savings.

Greed - Purchase to get certain offers, gambling and betting, lottery tickets, etc.

Carelessness - Most people tend to save where their known ones do, instead of finding the best instrument for them.

Q. Should one allocate a specified percentage to savings while working on a monthly budget?

A Big Yes. The order should be Income – Savings - Investment = Expenditure, and not Income – Expenses = Savings + Investment. If it isn’t done so, you’ll end up spending your income to the very last penny.

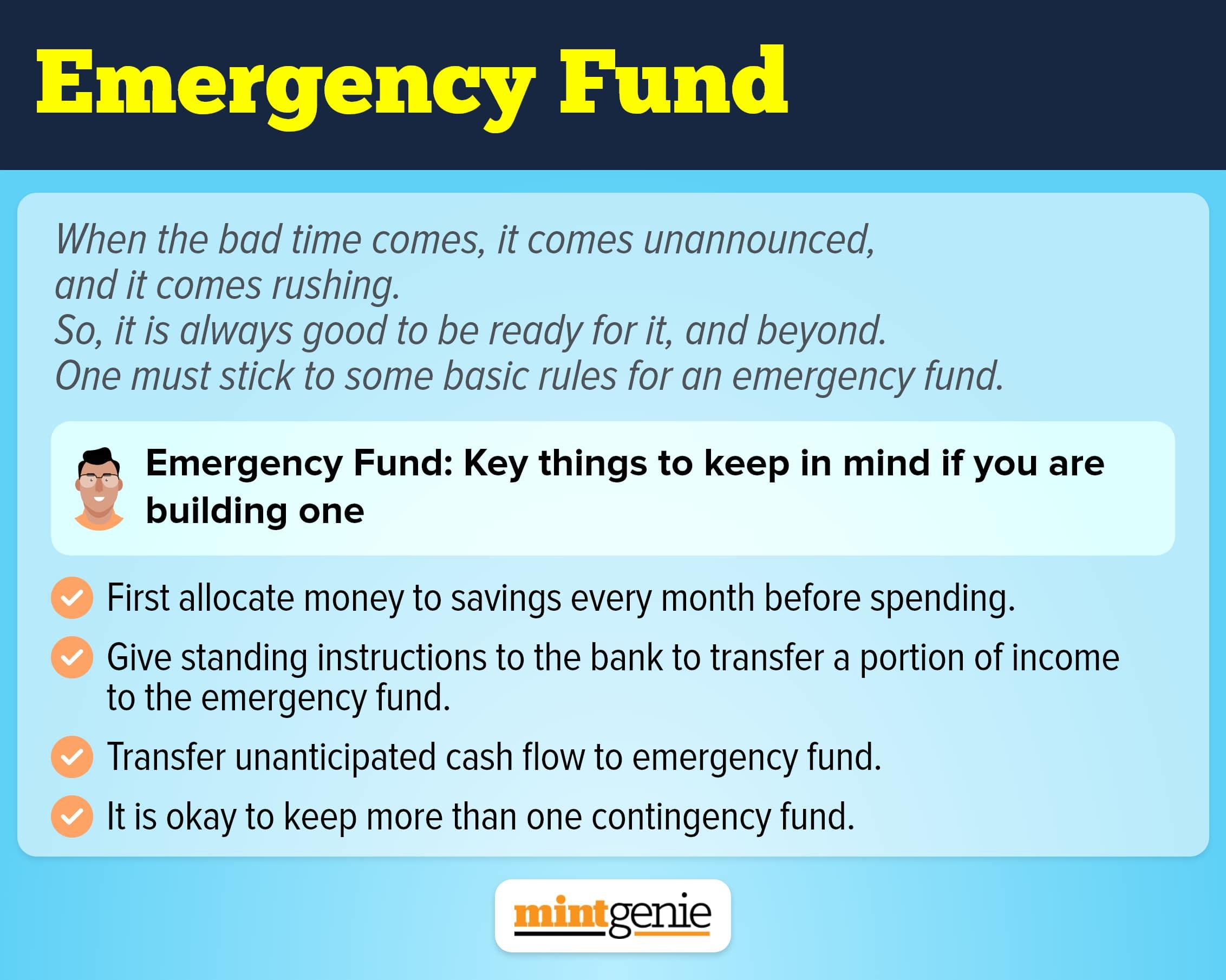

Q. What is the first step to saving enough money for emergencies and investments?

Calculation and Research. Calculate your average monthly expenditure and find out how much you would need to sustain your family for at least 6 - 12 months (pre-Covid it was three to six months), in the absence of an income. Research where to park your money. Choose an avenue that has high liquidity and low risk. Your good old savings account or fixed deposits is a good choice. Alternatively, you could also look at liquid funds, super savings accounts or digital gold, to park your emergency fund.

Q. Do you advise people to step up their savings like they step up their investments too?

Absolutely. My answer could be supported by a simple comparison. Calculate the average household expenditures for the previous year and the current year. This comparison is enough to show you that the contribution to your emergency fund should also be stepped up, along with the increase in inflation. Also, whenever there is a salary increase I strongly recommend increasing the investments by at least the same percentage.

Q. How much should one save in his or her emergency fund?

Ideally, an amount that could keep your current lifestyle covered, for at least 6-12 months. This amount should factor in your family’s food & household expenses, rent, essential bills such as electricity bills, water tax, education, fuel/transport, automated investments, etc.

Q. Low-income households or those with greater familial responsibilities find it difficult to save money. What strategies would you advise them?

While I understand that it is extremely hard for low-income households to find spare cash, for a regular contribution, I would advise them to build their emergency fund first. They could go for avenues with low risks, such as FDs, Corporate FDs, and Post office deposits.

If they are able to make a regular contribution, I would suggest they prioritise insurance over investment. These steps tackle the danger of unpredictability.

Q. What is the next step post savings? What is the first step to investing money for the future?

The next step would be insurance and investment. The role of a good health plan and good insurance in financial planning cannot be emphasised enough. Once good insurance plans are in place, the next wise step would be to start a SIP in a mutual fund that best suits your goals and requirements. A dutiful commitment to a SIP could reap wonders for your future.