With Nifty just one percent away from its peak of 18,887.60, hit in December 2022, brokerage house Ambit Capital, in a recent report, predicted that Nifty is likely to touch 20,900 by March 2024, implying a 12 percent upside from current levels.

As per the brokerage, the Indian markets are currently not expensive, however, it noted that there can be some volatility as institutional flows can be lower due to global liquidity, which can worsen as we move into the year.

Still, a greater than 10 percent upside from the Nifty fair value indicates an interesting opportunity, it said, adding that stock selection would hold the key.

"We roll forward our target to Mar-24. EYBY Gap implied Nifty fair value is 20.9k (Mar-24) at 7.1 percent yield, Mar-24 EPS ( ₹940). Upside surprise is possible if yields sustain at lower levels (<7.1 percent) or Mar-24 earnings are higher than expectations (>940)," stated Ambit.

Amid the current scenario, the brokerage noted that its preference remains in favour of large-caps over small and mid-caps.

Meanwhile, it has reduced weight in the IT sector but still remains marginally overweight on Banks. Also, it is underweight on auto and FMCG; and overweight on OMCs and Metals.

The brokerage also stated that India enters FY24 during a time of global uncertainty and despite the external headwinds, India is better positioned than most of its emerging market peers. India's external account would be the silver lining in FY24, with the combined effect of narrowing the current account deficit and strong capital inflows that could lead to the rupee appreciating by 2.4 percent. However, the risk of fiscal profligacy remains high in an election year, it warned.

Earnings estimates

The brokerage noted that the EPS estimates in FY21-23 were resilient but trend continuation in FY24 looks difficult.

"Earnings trajectory will likely change from FY24, with BFSI contribution to incremental EPS growth tapering to 43 percent. Our house view suggests IT, Metals & O&G (Reliance) contribute 20 percent of incremental EPS growth and are at risk. While banks' EPS trajectory remains robust, risks to Tech earnings remain with the expectation of revenue growth normalization to the pre-Covid period. Delay in China's recovery can hit Reliance and Metal earnings. Our analysis suggests, even in FY21-22 year when aggregate headline earnings were met, earnings delivery breadth remained poor. We don’t see material upgrades, additionally yield softening can put even bank NIMs at risk," it said.

Portfolio Positioning

The brokerage informed that its portfolio is mainly concentrated in large-caps (83 percent), whereas Mid//small-cap allocations are 12 percent/5 percent and cash allocation 5.2 percent.

While the brokerage retains overweight on banks, it recommends reducing weight as valuations aren’t as cheap as in May-22 and the book yield bond yield differential model suggests muted 1-year returns. Also, the brokerage reduced weight in IT and add to Healthcare. Other key overweights include Metals and OMCs, while key underweights include FMCG, Auto and Capital Goods.

Ambit has also made 5 changes to its portfolio

What’s in: SBI Cards, IndiGo, Affle, Max Health, and IndiaMart

What’s out: LIC Housing, Godrej Consumer, and Nifty Bank

Why the inclusion?

IndiaMart: After its struggles with new paid client acquisition during Covid, revenue has returned to 17-18 percent CAGR from pre-Covid levels while EBITDA margins have normalised, said Ambit. It remains convinced of the firm's strong network effects and execution. IndiaMart also appears to be a ‘Make In India’ beneficiary, it added.

Affle: As per the brokerage, global mobile/programmatic advertising is set to outpace total ad spends, with similar trends likely to replicate in underpenetrated markets like India, South East Asia, Latin America and Middle-East, from where Affle derives over 80 percent of revenues. This should drive 24 percent revenue CAGR over FY23-25E and EBITDA margin could expand 230bps over FY23-25E to 22.4 percent (26 percent by FY33E) on acquisition turnarounds, it added.

SBI Cards: Ambit expects momentum in card addition and card spending to continue given the state of the economy and the lower penetration of credit cards in India. Thus, it believes credit card is a high-growth and high-RoE industry for a long period. It expects EPS CAGR/average RoE of 30 percent/27 percent over FY23-25E.

IndiGo: Indigo remains a key beneficiary of consolidation in the sector (exit of Kingfisher/Jet/GoAir) and favourable demand-supply dynamics in the long run given low air travel penetration in India, said Ambit. Despite the increasing competitive intensity, it prefers Indigo given its established leadership, strong balance sheet, efficient fleet and cost structure. Longer term, Ambit continues to believe Indigo’s strategy to focus away from metro routes and expand into Tier-2/Tier-3 domestic routes and international routes would ultimately bear fruit.

Max Health: Ambit noted that Max Healthcare is a leading hospital chain in North India, particularly in the Delhi/NCR region, and the second-largest hospital chain in India in terms of revenue. Its concentrated, cluster-based approach has allowed it to build a well-regarded brand in its target market cities and has achieved industry-high margins and RoCE led by initiatives brought in after the takeover by Radiant Lifecare in 2018, stated the brokerage. It also added that FY24-27 bed expansion (83 percent of bed capacity) is most aggressive among peers.

Its top large-cap buy ideas include Bharti Airtel, HCL Tech, Axis Bank, Tata Motors, SBI Cards and Dr Reddy's.

Top midcap buy ideas: TVS Motor, Indian Hotels, Federal Bank, Prestige Estates, and Zee

Top smallcap buy ideas: PB Fintech, Bajaj Electricals, City Union Bank, Amber Ent, Safari Ind, and AMI Organics.

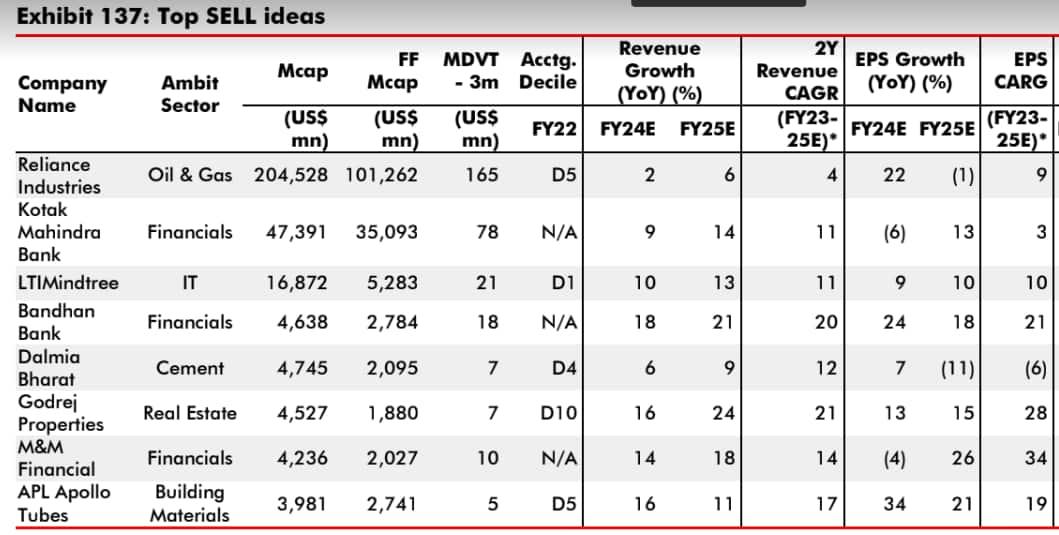

Meanwhile, the brokerage's top SELL ideas include Reliance Industries, Kotak Bank, LTIMindtree, Bandhan Bank, Dalmia Bharat, Godrej Properties, M&M Financial, and APL Apollo Tubes.