Nifty Bank index is down 11.3 percent vs 7.3 percent for the Nifty50 in the past month.

Bank Nifty continues to underperform. Key reasons why

TL;DR.

The whole banking sector has been under pressure in the previous month, with the Nifty Bank index down 11.3 percent vs 7.3 percent for the Nifty50.

ICICI Bank and HDFC Bank have each corrected by 10% to 15% and stocks like AU Small Finance Bank, Bandhan Bank, RBL Bank, Punjab National Bank, and State Bank of India have experienced a more significant drop.

American depository receipts or ADRs of leading private banks - ICICI Bank and HDFC Bank too, have plummeted by 15% to 18% in a month.

Until early January, much of the price decline in banking stocks was led by sector rotation on the part of foreign investors.

However, this cognitive process has changed. With bond yields rising, new concerns have emerged about how this may affect bank financials in the March 2022 quarter (Q4).

What has triggered the underperformance and what’s in store?

High fiscal deficit puts a strain on banks' treasury income

Treasury income of banks took a hit in the October-December (Q3) quarter, due to a sharp rise in yields on government securities, which has impacted investment portfolios of banks.

The yields on government securities rose over 50 basis points (bps) in Q3 due to various factors such as an uptick in US Treasury yields, volatile Brent crude oil prices and discontinuation of government securities acquisition programme (G-SAP), among others.

The increase in bond yields coincided with the revelation of a larger-than-expected fiscal deficit and gross borrowing schedule for the coming fiscal year in the budget

A 50-bps increase in portfolio yields leads to treasury loss of ₹5,800 crore for State Bank of India, ₹1,100 crore for Punjab National Bank, and ₹480 crore for Canara Bank, according to Motilal Oswal Securities.

Analysts expect MTM losses for banks, especially public sector banks, to increase in the coming quarters as yields on government securities are continuously rising.

The state-owned lenders will take a major hit because they have a higher share of government securities in their portfolios. SBI has the highest share of Available for Sale (AFS) and Held for Trading (HFT) portfolio at 43% of total investments, the brokerage said.

The surge in Brent crude oil prices in the international market during October-December led to inflationary pressure, which resulted in offloading securities by some investors.

The rise in crude oil prices leads to higher imported inflation for large consumers like India. Meanwhile, during that period US Treasury yields also rose on expectations of faster than expected tapering.

The yields on 10-year US Treasury notes rose 20 basis points during Q3.

Additionally, discontinuation of G-SAP and devolvement of securities on Primary Dealers at weekly bond auctions also weakened investors' sentiments leading to a sharp rise in bond yields and decreasing treasury income of most banks.

While volatility in bond yields is likely to keep other income of banks under pressure, lenders are looking to recoup treasury losses via higher credit growth and recoveries.

“Other income, it will be growing in the coming quarter also. Whereas the trading income, we presume that it will be at this level only. It will not increase. I think we are expecting to compensate the loss in the trading income through recovery in written-off accounts, through income from other sources and also through interest income. So finally, when we see, there will not be any impact whatever treasury is not giving to the Canara Bank,” said L. V. Prabhakar, managing director and chief executive officer at Canara Bank during a post-October-December earnings call.

Selling pressure from Foreign Investors

The Russia-Ukraine crisis has led to a rush towards safe-haven assets such as gold and the US dollar. Investors are selling riskier assets such as Indian equities.

Foreign portfolio investors (FPIs) have pulled out ₹38,068 crore from Indian equities and debt in February. This is the highest monthly outflow of foreign funds from the domestic market after their record sell-off in March 2020.

As per depositories data, FPIs have pulled out ₹35,592 crore from equities and ₹3,073 crore from the debt segment last month.

Nifty Bank's performance since November 2021.

Prior to this, the highest monthly outflows from Indian equities and debt were in March 2020 when the foreign investors pulled out a record sum of ₹61,973 crore from equities and ₹60,376 crore from debt, spooked by the coronavirus outbreak and its impact on the economy due to lockdown and restrictions.

FPIs have been net sellers of Indian equities since October 2021 pulling out ₹1,07,416 crore till February 2022. They also pulled out ₹10,253 crore from Indian debts during this period.

Unsecured loans are back

Banks are again facing stress in the unsecured loan segment, after a gap of 13 years. Most private banks that had grown their unsecured loans portfolios like credit card and personal loans aggressively in the last few years are now seeing repayment falling overdue in the October-December quarter.

However, those loans have not been classified as non-performing assets (NPA) due to the Supreme Court order in September that directed banks not to classify loans as NPA, which were not declared as NPA as on August 31, till further orders.

A recent report by Transunion CIBIL indicates that the pool of sub-prime and near-prime borrowers increased by 300 and 200 basis points year-on-year respectively in November 2021 while the downgrade in credit scores shot up by 500 basis points.

Given that 60 – 70 per cent of loans restructured since August 2020 pertain to the retail segment, banks may be taking risk by increasing their exposure to unsecured loans.

Banks' gross NPAs are rising

The economic slowdown owing to the ongoing covid pandemic for the last two years have hit the micro, small and medium enterprises (MSMEs) the most despite a lot of schemes and packages announced by the Reserve Bank of India (RBI) and the government.

Thousands of MSMEs either shut down or became sick after the government announced a nationwide strict lockdown in March 2020 in the wake of the Covid.

According to the RBI, bad loans of MSMEs now account for 9.6 per cent of gross advances of ₹17.33 lakh crore as against 8.2 per cent in September 2020. In fact, MSME bad loans had declined from ₹1,47,260 crore (8.8 per cent of advances) in September 2019, only to pick up again in 2021.

According to a report in The Indian Express, MSMEs' gross non-performing assets (NPAs) rose by ₹20,000 crore to ₹1,65,732 crore as of September 2021 from ₹1,45,673 crore in September 2020.

Public sector banks accounted for the bulk of MSME NPAs at ₹1,37,087 crore, the RBI says.

Among state-owned banks, PNB had MSME NPAs of ₹25,893 crore as of September 2021, followed by State Bank of India ₹24,394 crore, Union Bank ₹22,297 crore and Canara Bank ₹15,299 crore, the RBI says.

The rise in bad loans happened even after the RBI announced four loan restructuring schemes for MSMEs in January 2019, February 2020, August 2020 and May 2021.

Loans of as many as 24.51 lakh MSME accounts worth ₹1,16,332 crore were restructured under these schemes. Under the May 2021 circular issued by the RBI, loans for ₹51,467 crore were restructured, according to the RBI’s ‘Trend and progress of banking’ report.

Banking frauds will increase over the next two years

During the covid-19 pandemic, a push towards financial inclusion and digitisation made both consumers and banks rely heavily on electronic channels for banking. This significantly changed the way the industry operates.

Frauds related to data theft, cybercrime, third-party-induced fraud, bribery and corruption, and fraudulent documentation have increasingly been identified as major concerns, according to the Deloitte India Banking Fraud Survey.

Meanwhile, the RBI and the Indian government have announced a variety of measures—a moratorium on loan repayments, the interim freeze on insolvency and bankruptcy code (IBC) cases, and bank loan restructuring among others—to help struggling households during the pandemic. But these only worsened the problem.

Besides, remote working models for banking, which involve handling sensitive information, added to the problem.

With a significant number of bank staff working from home, banks had to provide their staff remote access to their organisation’s network and information.

This forced banks to bring about significant organisational and operational changes rapidly to avoid service interruptions, thereby raising concerns over vulnerability to fraud.

New loans and extensions arising out of the government’s support to businesses, along with the RBI’s moratorium, need careful monitoring of companies’ creditworthiness and viability of businesses in changing scenarios, according to industry experts.

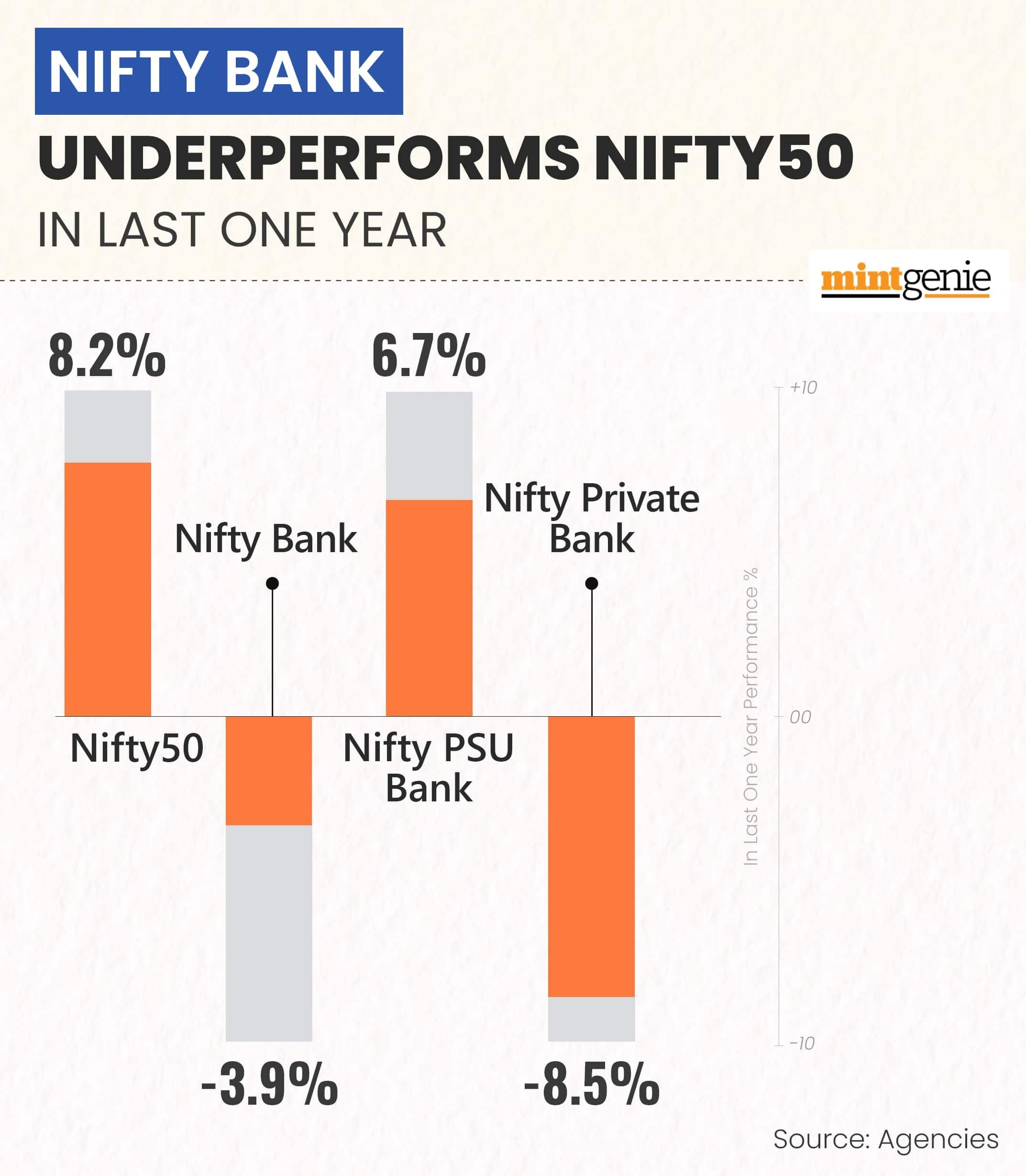

Exchange data show Nifty50 has given a return of 8 percent in the last one year (since March 2021) whereas Nifty Bank has fallen 4 percent in the same period. Some private banks are the worst hit while PSU banks have done much better. Nifty Private Bank index is down almost 9 percent in the last one year while Nifty PSU Bank index is up 7 percent.

First Published: 14 Mar 2022, 11:15 AM IST