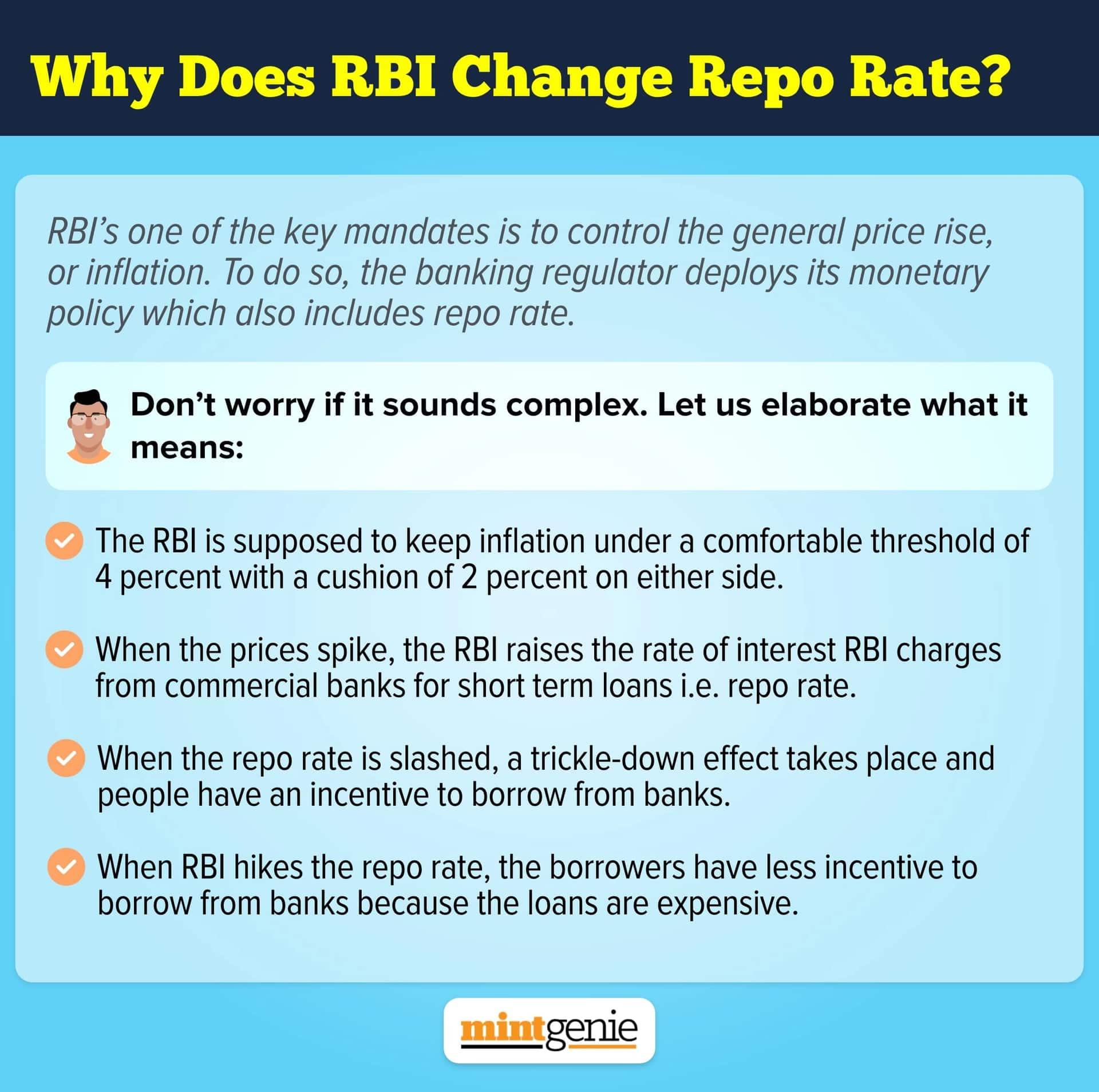

Even as seasonal inflationary pressures gather momentum, the Reserve Bank of India (RBI) has kept the repo rate unchanged at 6.5 percent in the August Monetary Policy, thereby maintaining a status quo in both, policy rate and stance. This comes amid a sharp spike in vegetable prices, a spatially uneven monsoon, and a divergent global monetary policy cycle.

The MPC voted unanimously to keep the repo rate unchanged. It decided to take a pause in April for the first time after consecutive rate hikes in 6 previous policies. The central bank has already increased the repo rate by a total of 250 basis points since May 2022 in a bid to contain inflation. This was the third time that the RBI has kept the rates unchanged.

Meanwhile, the MPC voted by a 5:6 majority to remain focussed on the ‘withdrawal of accommodation’ to ensure inflation aligns with the target while focussing on growth.

"Cumulative rate hike of 250 bps from FY23 is working its way through the economy. MPC remains resolute in its commitment to align inflation with the 4 percent target and anchor inflation expectations. Global economy continues to face daunting challenges," RBI Governor Shaktikanta Das said in his policy speech.

This decision was expected by most experts, however, the RBI raised the inflation forecast for FY24 to 5.4 percent from 5.1 percent in the June policy. But the GDP growth forecast for FY24 was retained at 6.5 percent.

Indian markets extended losses after the RBI policy announcement, even though it was on expected lines, because of the hike in inflation forecast. Both benchmarks Sensex and Nifty were trading around 0.5 percent lower dragged mainly by banks and financial stocks.

"The policy is not that hawkish but a couple of factors contributed to the market's decline. Firstly, the decision to maintain an additional 10 percent of the Incremental Cash Reserve Ratio (CRR) for the banks. Additionally, a shift in the inflation forecast from 5.1 percent to 5.4 percent could also be influencing the market sentiment negatively," said Shrey Jain, Founder and CEO SAS Online.

Let's take a look at what experts have to say about this policy:

Most experts said that while the policy is on expected lines, the increase in inflation forecasts means that the high policy rates will remain for long and, therefore, a rate cut can only be expected in the next financial year. Also, if inflation exceeds the RBI's forecast in the near term, another 25-bps rate hike is not out of the question, they added, saying that the domestic growth resilience is countered by external risks and inflation.

VK Vijayakumar, Chief Investment Strategist at Geojit Financial Services

The MPC has delivered in line with market expectations on rates, stance, and tone, with retention of rates and stance and the tone turning hawkish. The significant change is the upward revision in the FY24 CPI inflation projection from 5.1 percent to 5.4 percent. This means the high policy rates will remain for a long and, therefore, a rate cut can be expected only in Q1 FY25. From the market perspective, there are no positive or negative surprises in the policy.

Naveen Kulkarni, Chief Investment Officer, Axis Securities PMS

The RBI has maintained the status quo on rates which was on expected lines. With inflationary risks arising with the sharp surge in vegetable prices, the RBI has revised its estimates for inflation upwards to 5.4 percent, with a significant upward revision in Q2 estimates. The banking credit growth continues to show strength. The management commentaries of banks that have reported their Q1 numbers so far have also highlighted no demand slowdown. Despite the seasonal weakness in Q1, banks have so far reported healthy results. Margin compression was visible during the quarter, and continued pressure will be seen in the coming quarter. However, despite margin pressures, we expect earnings growth for banks to remain healthy, though lower vis-à-vis FY23.

Sujan Hajra, Chief Economist & Executive Director, Anand Rathi Shares and Stock Brokers

Despite raising the near-term inflation estimate, the RBI kept the longer-term inflation estimate unchanged. This implies that the RBI views the current inflation spike as transitory and explains why the RBI maintained the status quo on policy rate action. The temporary incremental CRR increase is a reaction to the sharp increase in systemic liquidity overhang, which is attributed primarily to the demonetisation of ₹2,000 notes. We expect this measure to be reversed as systemic liquidity approaches balance. At the same time, we believe that by maintaining its liquidity-tightening stance, the RBI maintained its concern about upside inflation risk. If the RBI's current assessment of inflation as transitory holds true, we expect the RBI to maintain the status quo for the next year. If inflation exceeds the RBI's forecast in the near term, another 25-bps rate hike is not out of the question. The measures are favourable in the short term for rate-sensitive industries.

Aditya Gaggar, Director of Progressive Shares

While the MPC decision of no change in the rates or the stance is on expected lines, the surprise element was the temporary hike in (incremental 10 percent) CRR requirements. The soaring vegetable prices were the reason for the hikes in inflation expectations for the next two quarters which are expected to cool down/reverse quickly with Q1FY25 estimates of around 5.2 percent. There is definitely an upside risk to inflation as the RBI maintained the liquidity-tightening stance. Also, the RBI MPC remains resolute in its commitment to align inflation with the 4% target and anchor inflation expectations. Surely with these estimates, there is no rate cut at least to happen in the current financial year, and no ruling out of hikes if necessary.

Anitha Rangan, Economist, Equirus

While in line with consensus, RBI has kept its policy rate unchanged. Notably, inflation estimates, especially near-term estimates (Q2, Q3) have been revised upwards meaningfully, while growth estimates are retained. Furthermore, the Q1FY25 inflation estimate of 5.2 percent and governor reiterating, the commitment to align to 4 percent on a durable basis, suggests that rate cuts are out of the way beyond the near term. Higher for longer is not just for the external world but also for India. Domestic growth resilience is countered by external risks and inflation. RBI is not ruling out hikes if necessary, clearly, cuts are out of sight.

Umeshkumar Mehta, CIO, Samco MF

It may be a pause, but inflation tantrums are expected to last longer than the D-Street is expecting. The vagaries of extreme climate, prolonged geopolitical wars, and higher commodity prices including food will tie the hands of central bankers across the globe in curtailing interest rates at lower levels. The outlook for Indian equities, therefore, moderates further given that the election bell will start ringing which may start weighing down from next quarter. Overall, the macros and monetary policies will dampen investor sentiments and in turn pause the equity rally going forward.

Radhika Rao, Executive Director and Senior Economist, DBS Group Research

The RBI MPC commentary on Thursday can be characterised as a pause with hawkish underpinnings. The decision and commentary were in line with our expectations, as highlighted in the preview note. The accompanying commentary reflected the MPC’s vigilance on inflation while highlighting the supply-driven nature of the recent run-up in food segments. Policymakers drew confidence from moderation in core prints and expect a seasonal correction in food in Q4FY23, but this was balanced with an emphasis that further action will be warranted on signs of un-anchoring in inflationary expectations as well as if inflation stays above the mid-point target of 4 percent on a durable basis. The evolving inflation trend is likely to be watched closely, pushing back rate cut expectations, especially in light of a notable upward revision in the 1QFY25 inflation forecast.