_1639560676401_1647925555730.jpg&w=3840&q=75)

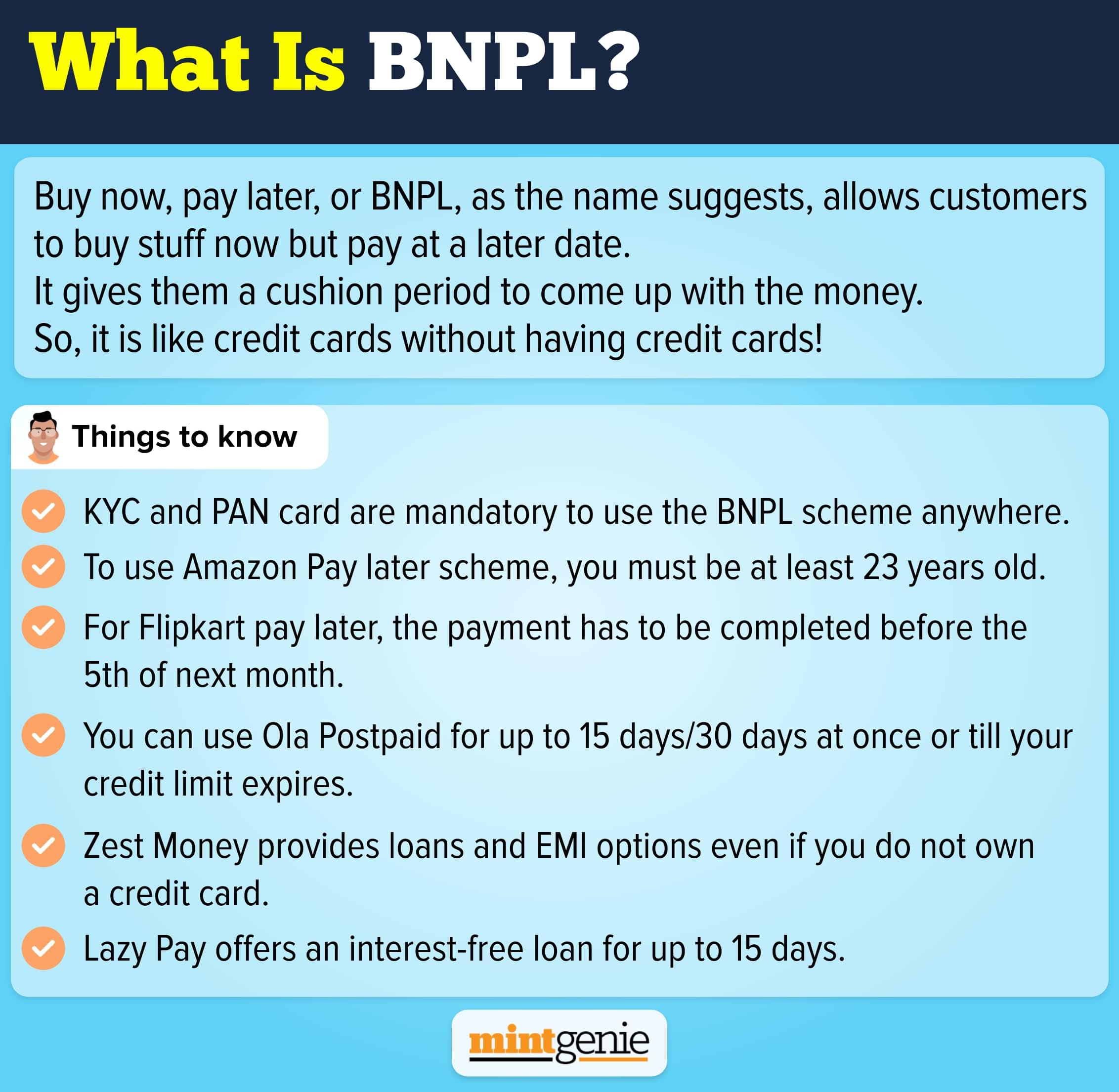

This is the latest buzzword in the lending world. From new-age financial startups (Fintechs) to non-banking financial companies (NBFCs) and even traditional banks, everyone is on the bandwagon of Buy Now, Pay Later (BNPL).

Now, BNPL is nothing but a credit line minus a credit card. Why is it such a hit, then?

Well, for one, the ticket size of things you can buy can be as low as ₹100 (or even lower if you can find a product), and second, the ease of the product. You do not have to fill forms and wait for banks to approve your credit card and send one to you.

BNPL is instant, like coffee and noodles (debatable, we know!).

And for these reasons, millennials are loving Buy Now, Pay Later. Big ticket purchases can be made with a single click without any approval from any credit agency or a bank! What's not to love?

Time to Dig Deep

They say if its too good to be true, it isn't really true (or something like that).

The BNPL scheme is actually a short-term financing mechanism that allows people to buy things upfront and pay for them later in future, often in three to four equal instalments. Currently, this tech-enabled credit is extended to the borrowers at the point of sale kiosks as a payment option. At present, these BNPL cards are being looked as the best alternative to credit cards that charge high-interest rates and are available under stringent conditions.

The rate of interest Demon

Compared to credit cards that charge nearly 36-42 per cent interest on the outstanding balance, BNPL cardholders are required to shell out somewhere between 16-40 per cent depending on the amount due and the user’s repayment behaviour. Also, Uni cards offer a flat one per cent cashback if the total amount due is paid back by the end of the month. For example, if a user has repaid ₹1.5 lakh of slice money within a month, he or she would be entitled to a cashback equivalent to ₹1500 (1% of ₹1.5 lakh). In comparison, credit cardholders have to accumulate rewards on every transaction that can be redeemed only after a certain number of points are collected.

Wait, did I just take a personal loan from a bank?

Customers have been slowly waking up to their messed up credit scores and personal loans they never applied for.

The matter came to light when many BNPL customers found how their credit scores taking a hit following incidents of personal loans being taken in their names.

The recent incident of Mumbai-based Jinal Shah (name changed) who was appalled to find two active loans worth ₹1500 and ₹6500 from an NBFC anda bank, respectively, in her name. This is not the first and lone incident of people finding out credits in their names despite never having borrowed from any financial institution.

A similar incident was shared by a Reddit user who frequently buys products on ecommerce platforms and has availed BNPL services. He, too, saw loans from a bank and an NBFC in his name during a routine CIBIL score check.

PS: This also brings us to the important point of checking your CIBIL report every three months.

What's the story Morning Glory?

An assessment of many such similar incidents revealed how BNPL companies had been selling personal loans to their customers without even mentioning them the same.

Ironically, such fraudulent instances continue as even financially literate people ignore reading the fine print before signing the documents. While these Fintech players are not banks who can provide credit cards but are associated with NBFCs that can give personal loans in their customers’ names.

BNPL companies issuing these cards have always maintained how relaxed conditions had prompted their use and expedited their ubiquity among people unable to pay for things at one go.

However, frequent incidents of cardholders being defrauded into buying personal loan products are gradually causing many people to refrain from their use.

So, the next time you use that pre-filled wallet by your cab aggregator, or buy food using an app and paying later, remember, more than BNPL, it could be a fresh line of personal loan in your name. Scary, right? We know.