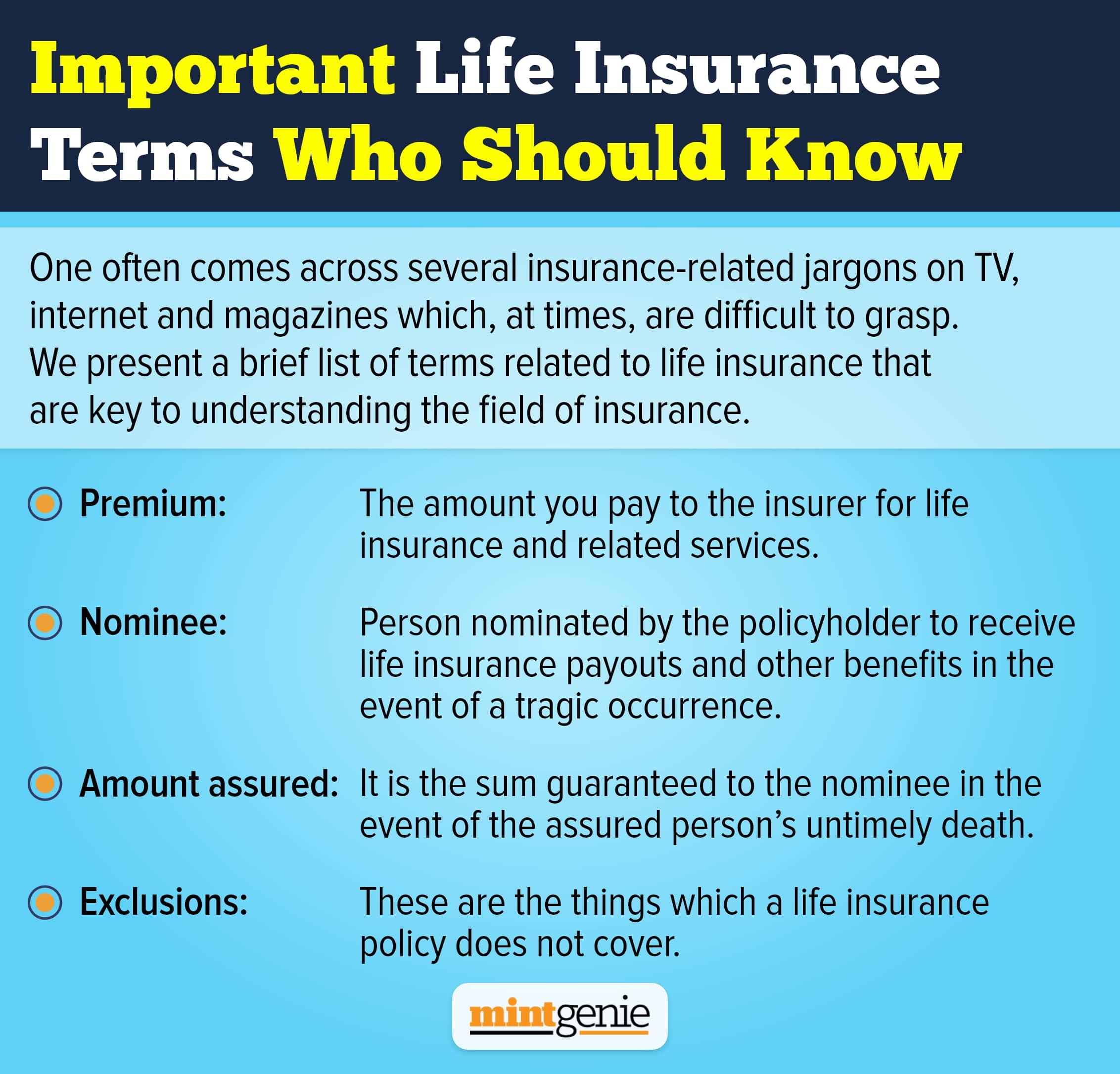

You will often hear many rely on multiple life insurance policies to insure and secure their loved ones. Not many realise how unknowingly they blur the distinction between insurance and investment, thus, putting to risk the financial future of their dependents.

More often, we see young people mulling about possible investment options during the start of their financial journey. In a hurry to amass wealth, what many forget is the need to secure your financial future by putting your money in something that will secure your ability to earn in future or ensure that the money keeps coming in even in your absence. Insurance is a must, though many are not sure how much to take and to what extent.

Ignorance of essentially personal finance concepts like life insurance has caused many people to make unwarranted mistakes. Ironically, more than the insured, it is their dependents suffer who they had set out to protect in the first place. These include:

Buying too many policies

It is a common misconception that buying too many policies translates to enough insurance and adequate protection. Roughly, one out of 10 people gloats about the number of insurance policies they have bought without assessing if they serve the purpose for which they were bought nor are they sure if the total sum assured from all these policies would be enough to pay off their existing liabilities apart from catering to their loved ones’ financial goals in their absence. This is especially true of many people falling prey to small-ticket policies that are cheap but do not serve the purpose for which they are bought.

Misconstruing investment as insurance

How many times do we hear people confused between investment and insurance? This also explains the rise in the number of people buying unit-linked insurance plans (ULIPs) thinking that they would serve the dual benefits of investment and insurance. This notion has caused more damage than any other personal finance decision. Investors who pay heavy premiums do not realize how only a small percentage of it goes towards insurance, which means that they are paying for investment with only a minor part of it being dedicated toward the insurance component.

The affinity towards endowment policies as they serve as investment cum insurance products is a matter of concern. Investors earn returns that either does not beat inflation or just notch over inflation that they then lose in paying taxes. Today’s endowment policies yield so less that investing in fixed or current deposits or debt funds will ensure better returns in the long run when compared.

Opting for return of premium plans

Many insurance companies realize their customers’ ignorance regarding the insurance concept and how they would jump at the idea of getting their money back with insurance needs not met. This is why they introduced the “Term Return of Premiums” plans wherein the investors got back the premiums they had paid toward insurance. While this may look like a great money-saving measure on the outside, it is actually a gimmick to lure more people into buying plans with low benefits under the guise of returning their premium money after a few years. The insured lose out as the money received a few years later has lost its value owing to inflation. The family of the insured lose out in the event of sudden death as the sum assured is too low to pay off their liabilities or meet their daily expenses.

Postponing insurance purchase

Not many people decide to buy life insurance early in life. Most people scan for various investment options on getting their first paycheque. The idea “I am fine, and have a lot many more years to live. Insurance can wait” has caused many people to delay buying life insurance. One can attribute this tendency to ignorance about prices of insurance premiums that are much lower for those who buy insurance when young. The premium amounts rise substantially as they get older, thus, forcing them to shell out more. Also, life insurance companies issue policies only when they are sure of their customers’ health. Choosing to buy life insurance much later in life makes the insurers apprehensive of their customers’ health, thus, explaining the rejection of insurance claims or sale of insurance at hefty premium charges.

Incorrect disclosures

An insurance policy is essentially a contract between an insurance company and the insured, thus, making both of them equally liable to furnish correct information during the sale and purchase of the plan. Submitting wrong details including health, income or sharing incomplete details of name, address, occupation, etc., can result in rejection of the insurance claim. This is another area wherein many people make mistakes while buying life insurance.