Home loan interest rates have gone up following the Reserve Bank of India’s announcement of hiking the key policy rates by 0.40 per cent in May 2022. An increase in the key policy rates translates to more interest that we have to pay on loans including those taken to buy a home, vehicle or for personal reasons. Repaying a home loan at a higher interest rate means that the borrower has to shell out more money in terms of equated monthly instalments (EMIs). This money outgo can cost you a lot if you have taken a big amount of loan or if your loan is running for 15-20 years.

If you are yet to consider taking a home loan, opt for a bank or financial institution that offers the lowest loan interest rates. This is a critical factor that many do not realize. A 0.5 per cent difference in loan interest that looks irrelevant and innocuous today will result in a higher EMI outgo if you look at its effect on the total interest payable during the entire loan tenure. To start with, new home loan borrowers can do the following to lower their EMI.

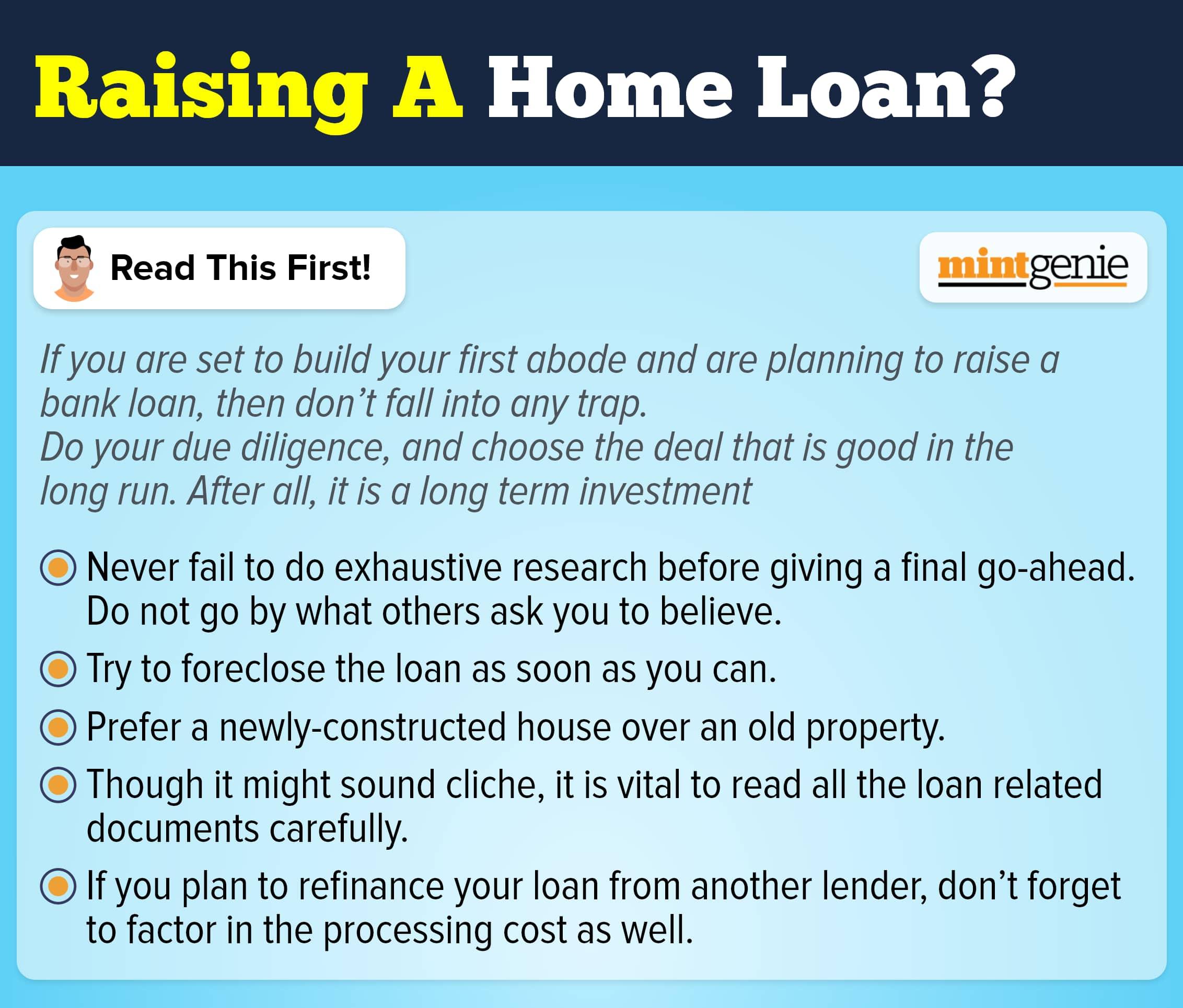

Look for the lowest interest rate

You need not run to multiple banks or financial institutions asking for their loan interest rates. A search online will take you through the myriad interest rates on offer by both banks and non-banking financial companies. Just compare them, and click on the site of the institution that offers the lowest interest rate. However, discounted interest rates come at a price. This means that you must look carefully at the various terms and conditions to avoid getting caught on the wrong foot. To start with, first, make a list of five to seven lenders, check their interest rates and read carefully the terms listed on their websites. Select a suitable lender that lends at lower interest rates, thus, allowing you to avail the benefits of repayments through lower EMIs.

Moreover, some banks offer competitive interest rates to their employees as opposed to customers working with some organizations. This means that borrowers must first try to seek loans from their employer organizations at lower interest rates. Also, a lot depends on the credit scores of the borrowers, which means that they must first check their credit scores before negotiating with the lenders for lower interest rates.

Make more downpayment

A higher loan amount begets more interest. This means that the borrowers may try to opt for a lesser loan amount to pay less interest. Also, lenders reward borrowers who keep the loan-to-value ratio low by offering them loans at lower interest rates. Try making at least 20-25 per cent of the price of the property as a downpayment. Borrowers can then negotiate for better loan rates and conditions with the lender. Apart, a higher downpayment means that the size of the EMIs is then considerably reduced for the borrowers owing to the lower value of the outstanding loan amount. Also, a lower interest rate on the loan drags down the value of the EMIs to be paid.

Selection of property

Lenders are apprehensive to dole out loans for unauthorized properties. Choosing properties in localities listed by the lenders in the non-preferred list can affect the chances of getting the loan amount approved. First check with the lender regarding the legitimacy and legality of the property to be bought. Borrowers may also select properties listed by the banks or financial institutions to ensure quick availability of the loan amount. Either change the lender or finetune your choice of the property to be bought in a way that it meets the conditions of the lender offering the lowest interest rates.

A longer loan tenure

This is an option that borrowers must consider only as the last resort available. The reason is that though a longer loan tenure avails the benefits of lower loan EMIs, the total interest outgo over the period is much more. Some borrowers also complain of having had to repay an amount almost double the price of the property for which the loan was sought. Borrowers must always strive to pay higher EMIs instead of choosing a long loan tenure to save on the total repayment amount.

Opt for home saver loans

Salaried income can opt for a structured loan owing to the regularity of their income levels. However, freelancers, often at the mercy of their clients, receive sporadic income. Fluctuating income levels also mean that borrowers may be able to repay their loan EMIs regularly for a period post which they may have to skip some payments. This difficulty in loan repayment often leads many borrowers to look for more flexibility in addition to lower interest rates. Borrowers looking to pay a lower EMI amount can choose home saver loan options. This facility is similar to an overdraft facility wherein the borrowers would be required to pay only the interest portion of the loan for some time. Since the minimum obligation expected of borrowers is to pay the monthly interest only, it eases off the financial burden off their shoulders.

Borrowers may consider the home saver loan option to pay just the interest amount. They can start repaying a higher amount when they have enough money to pay both the interest and principal components of the loan, thus, relieving them of the liability to repay the loan in the long run.