Imagine losing a chunk of your life’s savings on your dream home that you could not shift to! A common reason that many people investing in real estate face is buying an apartment in a stalled project. One such couple in Mumbai invested roughly ₹2 crores in an apartment in 2017 only to get stuck in unwanted legal proceedings when seeking possession of their property.

How to be financially prepared before buying your dream home? Here are 4 ways

TL;DR.

Renting versus buying property is an inconclusive debate. Apart, your dream of having your own home getting stalled in a project raises questions on factors that go into home buying.

To add to their worries, this couple had paid for the new property by selling their own flat and are forced to live in rented accommodation. They pay ₹90,000 rent every month, which is fairly high by today’s living standards.

This incident is not uncommon. You will find many instances like these that prompt many people to live on rent rather than buy their own homes. The renting versus buying debate will continue till people realize the right way to sort out their finances.

Personal finance is a personal affair, which means that all rules do not hold true for everyone. Aside from that, you can’t ignore the emotional aspect of buying a home. It is one thing to have a roof on your head that you call your own though many people buy property purely for investment reasons.

Carrying forward the experience that this couple shared online, it becomes pertinent to check what went wrong in their case. Also, how do you buy a house without ruining your finances?

Since the couple already owned a home, let us assume how much would have earned or lost had they invested their rental expense in equities instead of planning to buy a new home.

Investing the current rental amount in the market

This couple pays ₹90,000 rent as of now. What if the same amount had been invested in an index fund or any mutual fund (large cap, mid cap or small cap) for five years to earn returns from the market? The following table shows data on how investment in various funds helps to earn returns over a period, say five years. The power of compounding is the premise of all earnings from investments, so continued investments over a prolonged period help earn high returns over a period.

| Name of the fund | Type of fund | Monthly investment (in Rs) | Investment tenure (in years) | Five-year returns (in %) | Accumulated corpus (in Rs) |

| HDFC Index Fund - S&P BSE Sensex Plan | Index Fund | 90,000 | 5 | 13.62 | 77,65,204 |

| ICICI Prudential Nifty 50 Index Fund | Index Fund | 90,000 | 5 | 12.40 | 75,06,331 |

| Kotak Bluechip Fund | Large-cap Fund | 90,000 | 5 | 13.07 | 76,47,162 |

| Nippon India Large Cap Fund | Large-cap Fund | 90,000 | 5 | 12.86 | 76,02,674 |

| Quant Mid Cap Fund | Mid-cap Fund | 90,000 | 5 | 21.18 | 96,36,114 |

| Invesco India Mid Cap Fund | Mid-cap Fund | 90,000 | 5 | 15.54 | 81,95,152 |

| Axis Small Cap Fund | Small-cap Fund | 90,000 | 5 | 20.67 | 94,93,903 |

| IDBI Small Cap Fund | Small-cap Fund | 90,000 | 5 | 14.23 | 78,98,746 |

| Source: Moneycontrol | |||||

Had the couple not sold their house so early, they could have easily invested the current rental amount and earned high returns that beat inflation.

The right way to buy a house

Buying your own house has an emotional connection. The couple wanted the “Kalpataru” feel, and hence, their decision to put their money in one. However, the current situation indicates how they wrecked their finances are were forced to live on rent in an attempt to buy a new house.

Agreed that property rates are high and that your choice of property may not always be available. However, it still makes sense to take possession of your new house before disposing of your current home. This saves the hassle of living on rent or shifting from one rented accommodation to another till you shift to your new abode.

With interest rates rising, the demand for property has taken a hit, thus, suggesting that investing your life savings in a property does not make any sense. Instead, check if you can use your equities to finance your new purchase.

For example, you can seek a loan against your mutual fund investments. If you have no other outstanding loans and have been making regular contributions to your funds through systematic investment plans (SIPs), you are likely to have a good credit score and be eligible for a low-interest home loan.

Apart, you can seek a loan against the property you are buying after having made the down payment from your savings.

Let us explain this with the help of some simple calculations. Assume that the couple had made a down payment of ₹60,00,000 towards the property worth ₹2 crores. This means that they can now seek a loan of up to ₹1.40 crores against the property or their mutual fund investments. The current interest rates are between 7.5 and 8.6 per cent depending on their choice of lending institution.

Assuming that the couple had taken a loan of ₹1.4 crores at 7.6 per cent interest for 15 years, the monthly EMI would amount to ₹1,30,579. The couple is already paying rent of ₹90,000 and has a steady income flow, thus, indicating that the ₹40,579 additional payment every month would not have hurt their pockets.

Also, once they shifted to their new house, they could have sold their old property and prepaid the loan amount to get rid of the liability. Alternatively, they could take out some money from their mutual fund earnings to prepay the loan amount.

Most banks and financial institutions allow loan prepayment a year after the loan had been sought. Assuming that the couple prepays to the tune of ₹30,000 every month, this would help them get rid of the loan by 2028 instead of slogging with the liability for 15 years. Also, since the couple had shown zero interest in retaining their old property, they could have used the proceeds of the sale of their earlier house in 2024 and gotten rid of the pending liability well before the due date.

Choosing the right loan amount

It is foolish to spend beyond your means, which is why your home loan EMIs must not exceed 40-50 per cent of your monthly income. However, you must also consider your income from other sources like passive income through freelancing gigs or business or regular dividend income from stocks before deciding to take the loan. This will help you pay off your EMIs without feeling burdened because of the loan.

Do not rely on one income alone as it would refrain from making part payments or loan prepayments. Instead, plan your savings such that your loan is repaid on time with regular or sporadic prepayments without hurting your retirement corpus.

The right value of the house

It is not uncommon or unusual to seek a property with wide spacious rooms or as per the desired specifications. However, a lot depends on your affordability. The inexplicable urge to buy a house beyond your means may not only make a dent in your lifelong savings but hurt your ability to create an adequate retirement corpus. Irrespective of the kind of property you may have in your mind, no purchase must impede your retirement planning.

There are myriad factors before any home-buying decision including the amount that you can afford to pay toward your property. First, you must check the legality of your property, the classic debt-to-income ratio and the regularity of your income. You must also check how much you may have to pay toward your house maintenance and other unforeseen expenses.

Though there is no thumb rule to suggest to assess the value of the house that you must buy, personal finance analysts advise not to spend beyond 2.5-3 times your annual salary. This is because a major part of your income goes into repayment, thus, ensuring that you have enough to pay for your essential expenses even after paying your EMIs regularly.

How to be prepared for interest rate hikes?

The constant rate hikes by the Reserve Bank of India (RBI) to tame inflation mean an added loan burden on the borrowers. There is no way how macro factors such as geopolitical tensions might affect the global economy. You can best be prepared for the same. History is a testament to the fact that banks hike lending rates to control inflation, which means that you must always be prepared to pay more interest in the long run.

Many borrowers seek an extension of the loan tenure, which only results in added interest payments. This means that you must be prepared for future rate hikes by adding to your income sources, saving enough and investing appropriately. Relying on fixed-income products or debt funds will not earn you much, which is why you must start investing in equities early in life.

There is no magic wand to tell you how much more you have to pay in case your lender decides to hike its loan interest rates. Loan consolidation to repay at lower interest rates may help but not to the extent you anticipate. This itself underscores the need to realize the importance of early investments.

Let us understand the same with the help of an example. Assuming that you start investing from the day you receive your first salary. Say, for example, you put ₹30,000 every month in mutual funds for the next 15 years. Most mutual funds earn a minimum of 12 per cent returns. The maturity amount at the end of 15 years would be roughly ₹1,51,37,280.

If you had considered stepping up your investments by 10 per cent each year, the maturity amount would be somewhere around ₹2,45,34,733.

Assuming that you start investing when you are 25 years old and continue with your regular SIPs relentlessly for the next 15 years, what you have is a decent corpus to pay in part or full for your choice of house. This way, you not only save enough money to make the loan down payment but also have the choice to opt for a lower loan amount, thus, easing off the unwanted liability.

While staying on rent and investing the remaining amount enables you to create a huge corpus, such virtue signalling in favour of living on rent does not go down with many people, especially, those who yearn to buy or build at least one home during their lifetime.

Buying your own house is a dream that many people are not able to fulfil. The reason can be anything, though in most cases it is the lack of money that forces many people to continue living in rented accommodations. Making money is not difficult provided you are willing to earn enough and put in enough money for investments. It’s okay if you do not earn much, but you must ensure that you save and invest.

Focus on your savings and investments if you are looking to stabilize your financial future which includes planning to have your own house someday. Money creates money; wealth attracts wealth. This is why continued investments are an essential element of your financial goals.

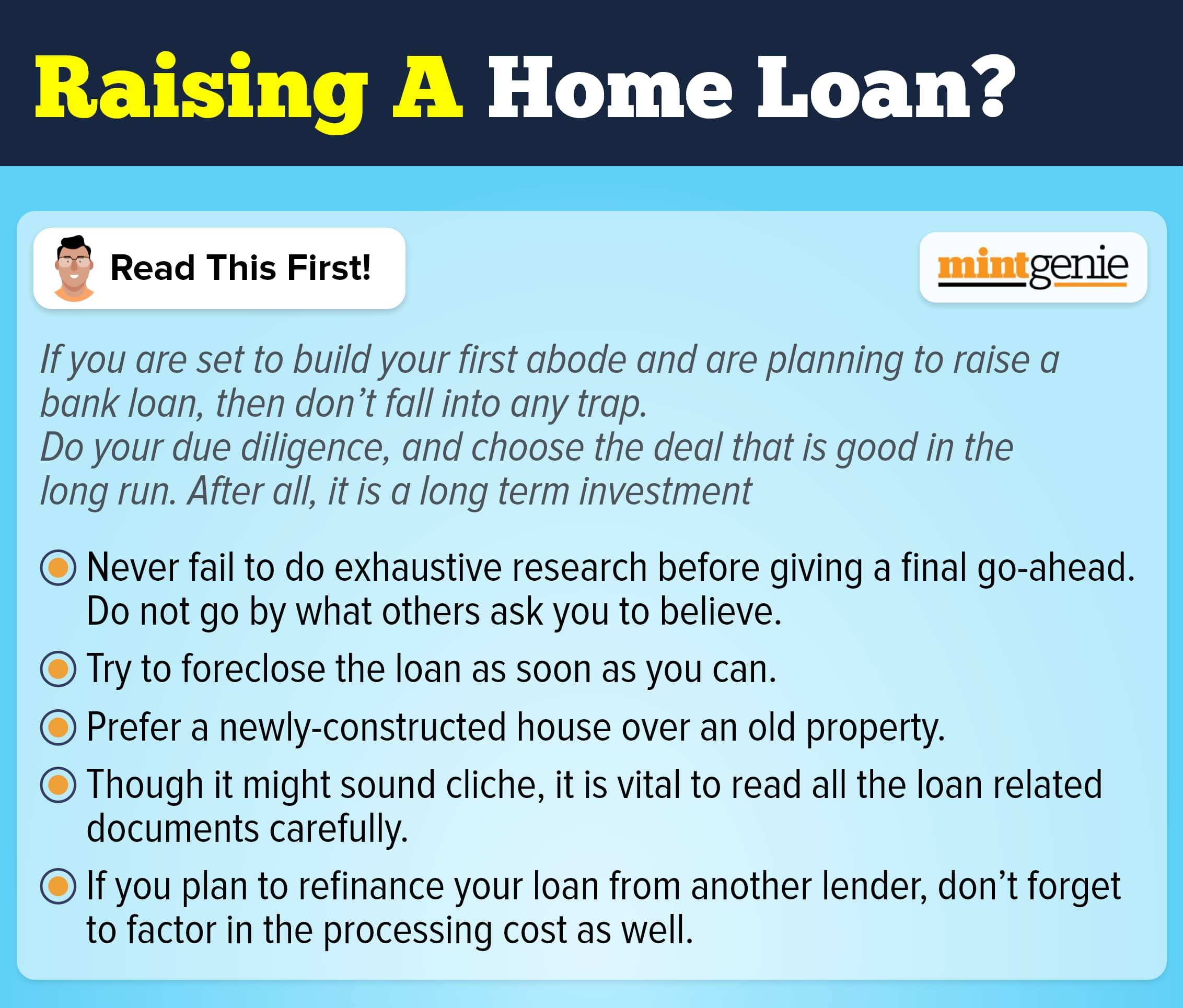

If you are planning to take a home loan, prefer a newly-constructed house over an old property.

First Published: 01 Nov 2022, 08:58 AM IST

Related Stories

personal finance

Home Loans: How much money do you stand to save if you prepay your loan? Let's take a look

Kirti Jha