Q1. My father has surgery coming up next month which can cost us up to 5 lakhs. Unfortunately, his health cover does not cover it, and we have to arrange funds in less than two weeks. I have a 5yr FD which I started 3 years ago with a corpus of 7 lakh, should I make a premature withdrawal?

-Amey Paranjape, Mumbai.

Yes, you can consider withdrawal since your deposit amount is close to your fund need. However, let’s not forget that banks also levy penalties on premature withdrawal or could lower the interest rate. Say if you were getting 7.5% interest for 5-year FD, it might lower to 6% now that you held the FD for only 3 years.

There is a better way to use your FD in case of emergencies as security to avail of a loan. Unless you are a 5-year tax-saving FD investor, you are eligible to apply for loans against FD.

The loan limit solely depends on the fixed deposit and can go up to 95% of the deposit amount. In your case, you can expect somewhere up to 6,30,000.

This way you will receive the interest of the remaining amount from the FD even after the sanction of the loan. It gives you the option to maintain your deposit while meeting your immediate cash demands.

The interest rate on loans against the FD varies from bank to bank. Banks and NBFCs usually charge 0.5% to 2% rate of interest above the applicable FD interest rates.

Another option for short-term needs is an overdraft against FD. It allows you to withdraw up to 85% to 95% of the fixed deposit amount. The bank charges interest only on the amount withdrawn from the overdraft, never on the whole overdraft limit.

The interest rates charged on your fixed deposit OD (overdraft) are 1% to 2% above the fixed deposit rates. However, Overdraft against FD is usually considered in case of a temporary cash crunch. You can deposit the outstanding amount whenever it is convenient for you.

Since you are likely to need time to recover your funds, we advise you to compare the interest on the loan-against FD and the penalties on premature withdrawal before you decide between the two.

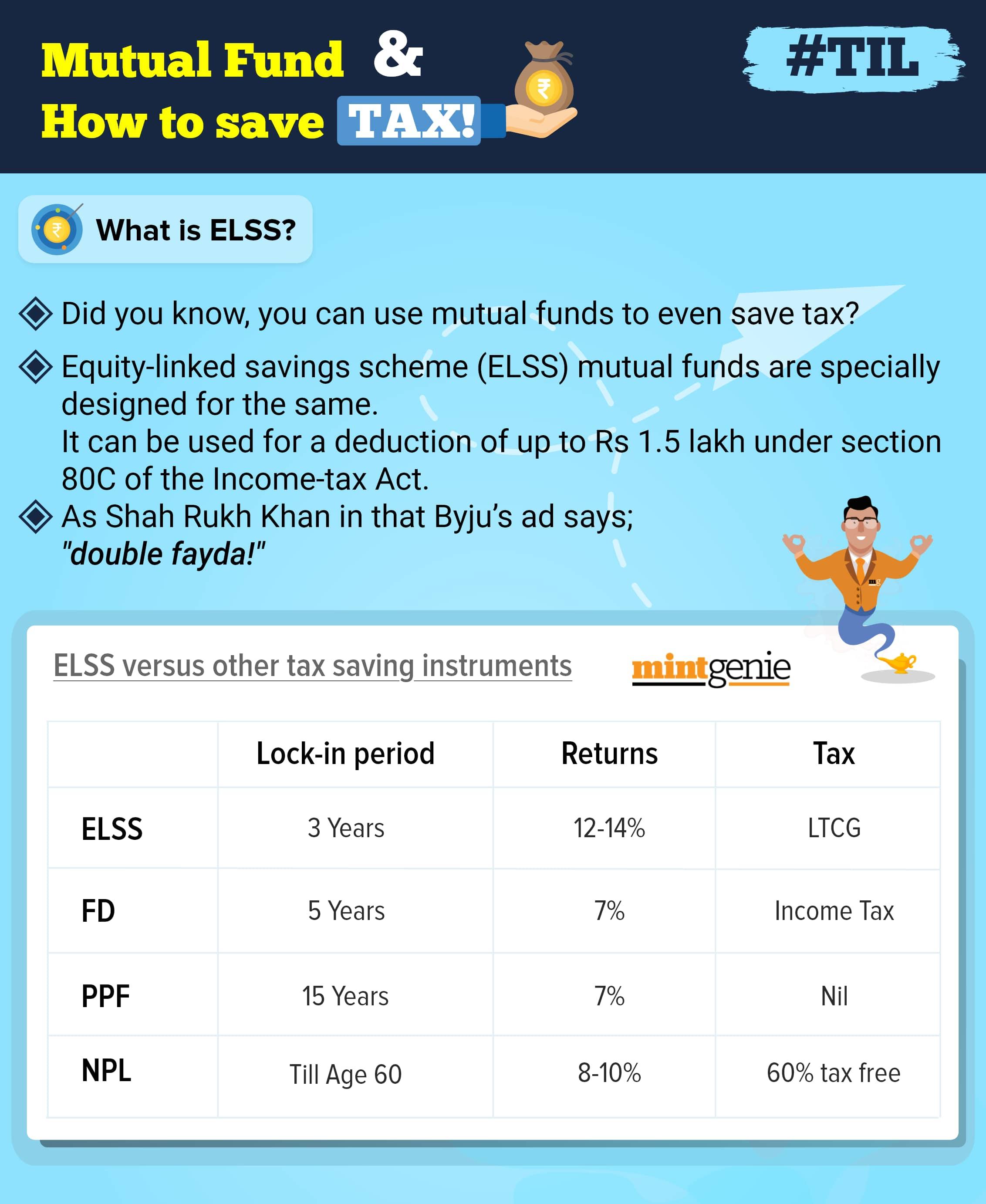

Q2. I’m thinking of expanding my portfolio. I have SIPs in Nifty 50, ICICI Prudential Tech, Quant Tax Plan, and S & P 500. I also have a PPF and insurance for tax-saving. Should I invest some more in ELSS?

-Anchal Mehta, Shimla

When it comes to tax-saving, ELSS is an excellent investment. But if you have already exhausted the Rs. 1.5 lakh limit u/s 80C, investing in ELSS might not be as rewarding as other equity mutual fund schemes.

You may ask, what’s the maximum amount you should invest in ELSS?

Say your total taxable income for the year is greater than 4 lakhs and you are not a senior citizen, follow this formula:

ELSS investment for the year = 1,50,000 Less Total Employee Provident Fund contribution for the year Less Other 80 C deductions* available to you.

If your goal is to expand your portfolio, we’d suggest investing the surpluses in more suitable mutual fund schemes that can offer better returns than ELSS Schemes.

Let’s take an example. From your salary, there is a deduction of ₹6,000 every month (or 72,000 for the year). Additionally, you have an Insurance Policy for which you pay ₹24,000 per year. And you have no other qualifying deductions from the list below.

Now using the above method, the amount that you should invest in ELSS is ₹54,000 (150,000- 72,000 – 24,000) during the year. You can invest this entire amount in one go or invest ₹4,500 monthly (SIP) or ₹13500 quarterly or any other combination at your discretion.

By restricting the amount you invest up to ₹54,000/- in ELSS and you have the option to invest any surplus in equity mutual fund schemes without a 3-year lock-in. More importantly, these equity mutual fund schemes may have a better risk-reward payoff than a Tax Saving Fund.

And if tax-saving is your primary goal, consider these deductions available under Section 80C:

PPF (Public Provident Fund)

EPF (Employees’ Provident Fund)

Five year Bank or Post office Tax Saving Deposits

NSC (National Savings Certificates)

ELSS Mutual Funds (Equity Linked Saving Schemes)

Kid’s Tuition Fees

Principal repayment of Home Loan

NPS (National Pension System) [An additional Rs50k of a tax-exempt investment is allowed over and above the Rs. 1.5 lakh allowed under 80C]

Life or Term Insurance Premiums

Sukanya Samriddhi Account Deposit Scheme

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

Kuvera is a free direct mutual fund investing platform.