Q. I am a 21-year-old college student. I wish to invest in a Public Provident Fund, but I am uncertain about the eligibility, lock-in period, tax implications, minimum investment threshold, etc.

-Saksham Dhariwal, Pilani

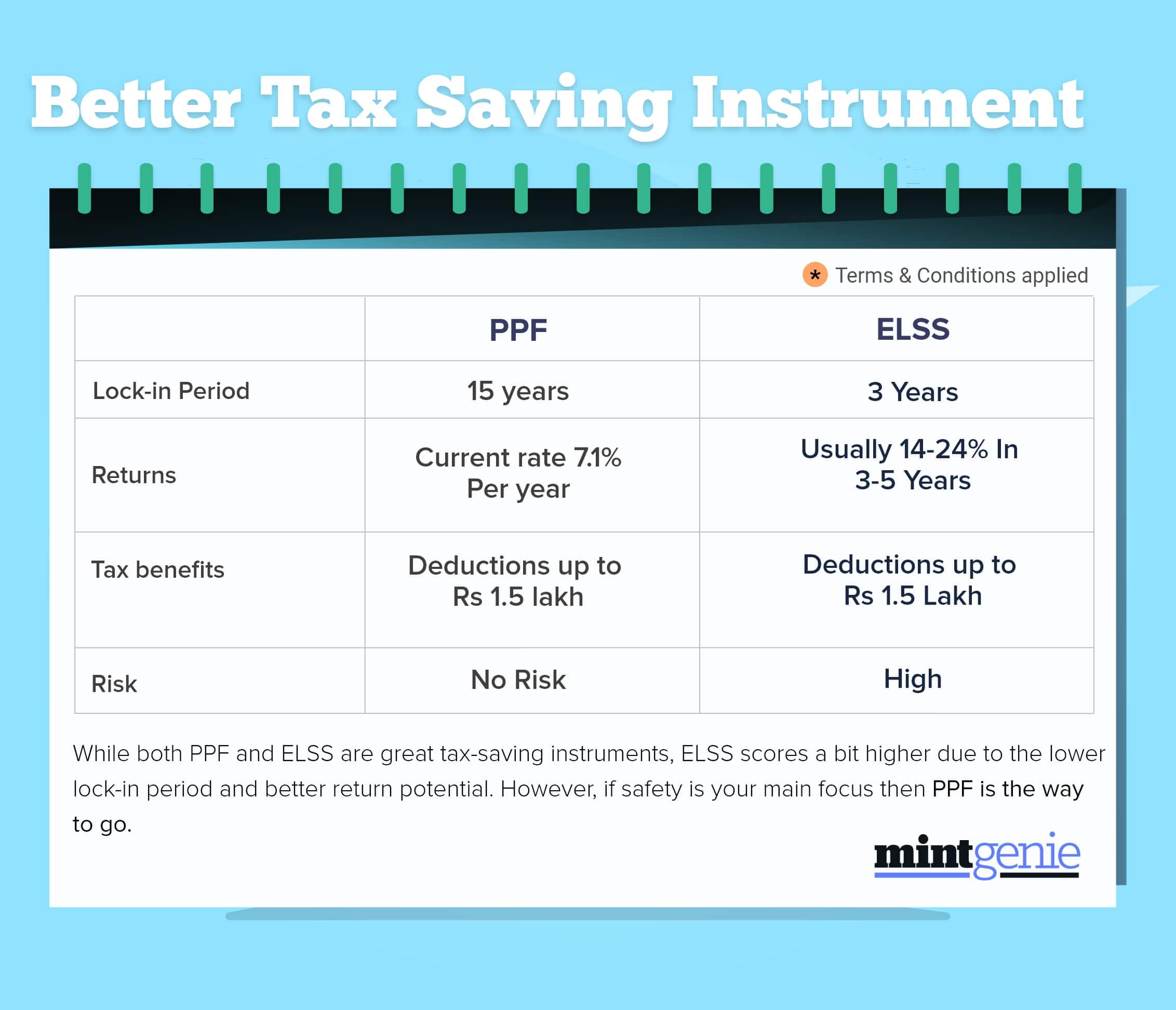

The Public Provident Fund scheme is one of the most well-liked long-term saving schemes launched by the government of India. This is mostly attributable to the fact that it offers a favourable combination of guaranteed returns, and tax savings.

The Public Provident Fund (PPF) scheme was introduced by the government in 1968. Under the scheme fixed interest is offered to the account holder. Interest is compounded on an annual basis. After account opening one can invest in it at any point of time, the minimum investment threshold is INR 500.

Since 1968, PPF has consistently built wealth for the investors by providing one of the highest interest rates amongst fixed income saving schemes. Investors can use PPF as a mechanism to build up a corpus for their retirement or as a tool to achieve their long-term saving goals. We have elaborated on the key features of PPF scheme below:

Key Features

Interest rate

Before every quarter, the central government sets the interest rate at which the interest will accrue on savings invested in PPF. As on 29 July, 2022 an interest rate of 7.1 percent has been set for the second quarter of FY 2022-23, spanning from July 1 to September 30. Every month interest is calculated at the applicable interest rate on the lowest balance in your account between the 5th of the month and the end of the month. Therefore, it is imperative that as soon as you get your salary you deposit a certain portion of it in your PPF account before the 5th of every month. Interest is compounded on a yearly basis in PPF.

Lock-in period

The PPF comes with a relatively long lock-in period of 15 years. After the completion of 15 years, you have the option to extend your account for another block of 5 years. You can repeatedly extend your PPF account in blocks of 5 years, indefinitely.

Premature withdrawal

Any time after the expiry of five years from the end of the year in which your PPF account was opened, you may, avail premature withdrawal, from the balance to your credit, an amount not exceeding 50% of the amount that stood to your credit at the end of the fourth year immediately preceding the year of withdrawal or at the end of the preceding year, whichever is lower.

Premature closure

You can close your PPF account only on certain grounds, which are mentioned below after the expiry of a minimum of 5 years:

- Treatment of life-threatening disease of the account holder, his spouse or dependent children or parents.

- Higher education of the account holder, or dependent children on production of documents and fee bills in confirmation of admission in a recognised institute of higher education in India or abroad.

- On change in residency status of the account holder.

Taxation on PPF

Investing in PPF up to INR 1,50,000 qualifies for a tax deduction under Section 80C of the Income Tax Act. 1961.

The investments made through the PPF fall under the category known as Exempt-Exempt-Exempt (EEE). This indicates that:

- Contributions to the PPF are exempt from taxation.

- Interest earned on the PPF account is exempt from taxation.

- At the time of withdrawal, the final corpus is likewise exempt from taxation.

If you are looking for guaranteed returns along with a reduction in your tax liability PPF is one of the best investment options available to you.

Eligibility

- A PPF account can only be opened by a citizen of India.

- For minors, parents/guardians can also open a PPF account.

- Multiple accounts and joint account opening are prohibited.

Minimum & maximum investment amount

- A minimum annual investment of Rs. 500 must be made by the account holder.

- A maximum of Rs. 1.5 lakh can be invested in a PPF account in a single financial year.

Options after PPF account’s maturity

Let's say you started a PPF account in 2007 and it matured in April 2022, but you wish to continue instead of closing it. An account holder has two options if their PPF account has matured.

- Close the PPF account & withdraw the amount: An individual has the option to close their PPF account once it reaches maturity. They must keep in mind, nevertheless, that the maturity date will not be based on the day the PPF account was opened. According to the PPF Scheme, 2019, the maturity date for PPF accounts is 15 years from the conclusion of the fiscal year in which the initial contribution was made.

- Extension of the account: You can add an extra five years to the maturity of your account with this option. At the end of the extension period, you can again extend your PPF account for another block of 5 years. You can keep on extending your PPF account indefinitely.

Note: This story is for informational purposes. Please speak to a financial advisor for detailed solutions to your questions.

Kuvera is a free direct mutual fund investing platform.