With markets near their all-time high, Nifty Bank and Nifty FMCG have touched their peaks. While both of these indices have multiple tailwinds and a healthy growth outlook, let's analyse which of these has a better long-term opportunity for investors.

Nifty Bank vs Nifty FMCG: Which index is likely to give better returns in long term?

TL;DR.

Nifty Bank and Nifty FMCG both have already touched their peaks. While both these indices have multiple tailwinds and a healthy growth outlook, let's analyse which of these has a better long-term opportunity for investors.

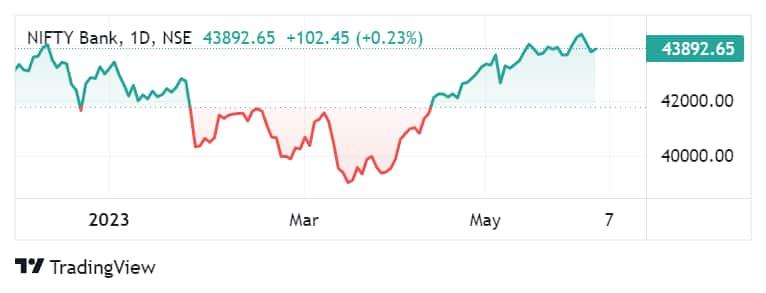

While Nifty FMCG has hit its record high of 51,399.55 in intra-day deals today (June 2, 2023); Nifty Bank also touched its all-time high of 44,498.60 on May 30, 2023.

Looking at 2023 YTD, Nifty FMCG is the best-performing index. The index has surged 16 percent in 2023 YTD as against a 2.5 percent rise in benchmark Nifty and a 2 percent gain in Nifty Bank in this period.

Nifty FMCG has given positive returns in all 6 months of the calendar year 2023 so far while Nifty Bank has given positive returns in 3.

Meanwhile, in the last one year, both Nifty Bank and Nifty FMCG have outperformed the benchmark, Nifty FMCG still emerged as a better performer between the two. Nifty FMCG surged 33 percent in the last 1 year while Nifty Bank advanced 23.6 percent. In comparison, the benchmark Nifty added 11.6 percent in this period.

However, in the long term, Nifty Bank has given better returns between the two. Nifty Bank has rallied 114 percent in the last 3 years while Nifty FMCG is up 75 percent and Nifty has advanced 86 percent.

The FMCG index, however, has outperformed the banking index during the last five years. The FMCG index gave 76 percent returns, while the bank index gave 63 percent returns for the five-year period.

Nifty FMCG

Constituents

In the Nifty FMCG, 10 constituents are in the green in 2023 YTD while the remaining 5 are in the red, whereas among the 12 constituents in the Nifty Bank index, 7 are positive while 5 are negative.

ITC has gained the most in the FMCG index, up over 33 percent followed by Varun Beverages and Godrej Consumer, up over 20 percent each. Meanwhile, Radico Khaitan and Nestle also added over 10 percent in this time.

United Breweries was the top loser in the FMCG space, down almost 15 percent followed by Emami, down over 7.5 percent.

On the other hand, IDFC First Bank was the top performer in Nifty Bank, up 23.5 percent followed by AU Small Finance Bank and Bandhan Bank, up over 10 percent each.

Meanwhile, Federal Bank was the top loser, down 9 percent followed by PNB, down 7.5 percent.

Looking at the last 1 year, only 3 stocks in the Nifty FMCG index were in the red - Emami, United Breweries and P&G, down between 2.5 percent and 8.6 percent. Meanwhile, Varun Beverages is the top gainer, up 130 percent in 1 year followed by ITC and Radico Khaitan, up 62 percent and 51 percent, respectively.

In Nifty Bank, only 1 stock - Bandhan Bank - gave negative returns (down around 17 percent) in the last 1 year. IDFC First was the top performer, up 105 percent followed by Bank of Baroda and PNB, up 82 percent and 65 percent, respectively.

Nifty Bank

Which index to choose for long-term investment?

Sunil Damania, Chief Investment Officer, MarketsMojo, has picked Nifty FMCG over Nifty Bank over the long period.

Damania said that it is important to understand that two companies dominate both the Nifty Bank and the Nifty FMCG index. In the Bank Nifty, HDFC Bank and ICICI Bank account for more than 55 percent of the weightage, while in the FMCG index, ITC and HUL account for more than 60 percent of the weightage. Hence, the movement of the indices is dominated by two companies.

Commenting on banks, the expert noted that everything is going right for the banking sector, including credit cost, growth in deposits and advances and the lowest NPA level in many years. In other words, all good things are priced in. That makes outperformance rather tough from this level.

On the other hand, the FMCG industry has had to navigate a tough time due to spiraling input costs and weak rural demand. Both factors are softening, giving much fillip to the FMCG sector, he stated. He also believes that India’s consumption story theme should make a huge comeback, which should help FMCG companies to post better volume growth and bottom-line growth. Hence, FMCG companies should outperform, predicted the expert.

Suman Bannerjee, CIO, Hedonova, also likes FMCG over banks.

"FMCG sector revenue growth is expected to be in the low double digits in FY24, aided by volumes. The sector is currently trading 5 percent above its 5-year average valuation, which is expected to continue in the short term. Considering the long term, the FMCG sector has historically demonstrated steady growth due to increasing consumer demand and a growing middle class. This trend is expected to continue as the Indian economy expands," said Bannerjee.

When comparing the long-term potential returns between these two indices, it's important to consider several factors, noted the expert:

Economic Growth: The banking sector generally benefits from economic growth, as increased lending and investment activities can drive profits. The FMCG sector, on the other hand, tends to be less cyclical and may provide more stable returns during periods of economic downturn.

Interest Rates: Banks' profitability can be influenced by changes in interest rates. In a rising interest rate environment, banks may experience improved net interest margins, which can positively impact their earnings. Conversely, falling interest rates can put pressure on bank profitability. FMCG companies are less directly affected by interest rates.

Regulatory Environment: Changes in banking regulations, such as capital requirements or lending norms, can impact the performance of banks. It's essential to consider regulatory changes and their potential effects on the banking sector.

Consumer Behavior: The FMCG sector's performance depends on consumer spending patterns, preferences, and brand loyalty. Factors like population growth, income levels, and urbanization can influence consumer behavior and demand for FMCG products.

Overall, Bannerjee believes the FMCG space has better long-term investment opportunities.

CONTRARIAN VIEWS

Jatin Gedia, Technical Research Analyst, Capital Market Strategy, Sharekhan by BNP Paribas, believes that Nifty Bank is likely to outperform Nifty FMCG.

"Nifty Bank and Nifty FMCG indices have provided phenomenal returns since March 2020 when all the major indices formed a long-term bottom. In terms of returns, the Nifty has risen 150 percent (From 7500 to 18900), the Bank Nifty has risen 175 percent(from 16100 to 44500) and the Nifty FMCG index has risen 125 percent (from 22700 to 51000) during the period April 2020 to May 2023. So comparing the historical performance, we can conclude that Nifty Bank has outperformed the Nifty FMCG index. Going forward we are likely to see this trend continue," he said.

As far as long-term projection is concerned, the expert noted that on the Nifty Bank index, he has a price target of 52,800 while on the FMCG Index, he has a target of 55,000, indicating the appreciation from current levels in Nifty Bank to 20 percent and 8 percent for the FMCG Index. Thus, going by the historical performance and the future projection Gedia believes that we are likely to witness outperformance from the Nifty Bank Index from Long term perspective.

Vinit Bolinjkar - Head of Research - Ventura Securities, as well, expects Nifty Bank to do well in the long term compared to Nifty FMCG.

"Post NPA route, Indian banks are ready with a healthy balance sheet and have fresh capital for business expansion. On the other hand, the performance of the FMCG sector will majorly depend on the monsoon in FY24. A normal monsoon is an essential factor for a meaningful demand recovery in rural areas, and there are reports of the possibility of El Nino in FY24," he stated.

Major trigger points for Nifty Bank, as per the expert, include:

1) Pick up in capex cycle and infrastructure spending is expected to improve project financing and commercial vehicle loans

2) Revival in the real estate market has improved the demand for housing finance. In addition, affordable housing has opened the next leg of growth in the real estate market.

3) Improving demand for utility vehicles increased the average ticket size of loans per vehicle.

Given these factors, the upside potential in Nifty Bank is strong and it could outperform the overall market, he said.

Nirav Karkera, Head of Research at Fisdom, has also picked Nifty Bank.

The expert pointed out that in the past 13 years, both the Nifty Bank and Nifty FMCG indices have demonstrated comparable returns and have outperformed each other almost an equal number of times, however, going forward, the Nifty Bank index is poised to deliver superior long-term returns compared to the Nifty FMCG index.

"It is important to consider that the FMCG sector comprises diverse sub-segments with growth opportunities spread across the value chain, making it challenging for the FMCG index to accurately capture this dispersion and overall growth trajectory. On the other hand, the banking industry has made significant progress. The non-performing assets (NPA) as a percentage of total advances have witnessed a notable decline from 5.6 percent in FY18 to 1.7 percent in FY22, indicating a substantial improvement. Moreover, the banking sector boasts a strong capital adequacy ratio of approximately 16 percent, indicating a robust risk appetite for lending," he explained.

Therefore, although there may be short-term deviations, the expert forecasts that the Nifty Bank index will offer better long-term returns compared to the Nifty FMCG index.

Narendra Solanki, Head Fundamental Research – Investment Services, Anand Rathi, has also chosen Nifty Bank.

If the overall economic growth is expected in the long term as is the case now, then that would be more beneficial to Nifty Bank in comparison to the Nifty FMCG index as it could capture the much larger spectrum of growth including the consumer growth, said Solanki.

"In terms of valuations both these indices are trading currently higher than their long-term 10-year average and on a price basis FMCG has performed better than Nifty Bank on a YTD basis. However, if one looks at a longer range, then price performance seems to be largely at par with spurts of outperformance by each for about 2-3 years in a period range of about 10-15 years. So, one must look at a much more basic level. So from a core economic perspective, the FMCG index represents the basic consumer sector and India is a large consumer market with rising per capita and increasing disposable income presents positive tailwinds for the FMCG sector with a long runway of growth," explained the expert.

Now coming to the Nifty Bank, he noted that historically and even now it is true that the Indian economy is underrepresented in the capital market with a lot of sectors and companies especially MSME and SMEs which are not listed along with large companies. However, he added that many such companies are key drivers of growth in the overall banking space and hence Nifty Bank also acts as a proxy for these unrepresented large segments.

Apurva Sheth, Head of Market Perspectives and Research, SAMCO Securities, as well, like banks over FMCG space.

According to Sheth, Nifty Bank has generally outperformed the Nifty FMCG index over most of the medium and long-term time frames. In the table below, you can see banking sector has delivered better returns than the FMCG sector in all except the 5-year time frame.

Source: Samco

"There are several factors that can be attributed to the banks outperforming FMCG companies in the long run. Banks benefit from economic growth and the expansion of the financial system, as increased demand for credit and banking services leads to higher loan volumes and profitability. India is historically underpenetrated in terms of banking and financial services. Thus, there has been immense scope for prudent private sector players to grow their market share at the cost of PSU banks," she said.

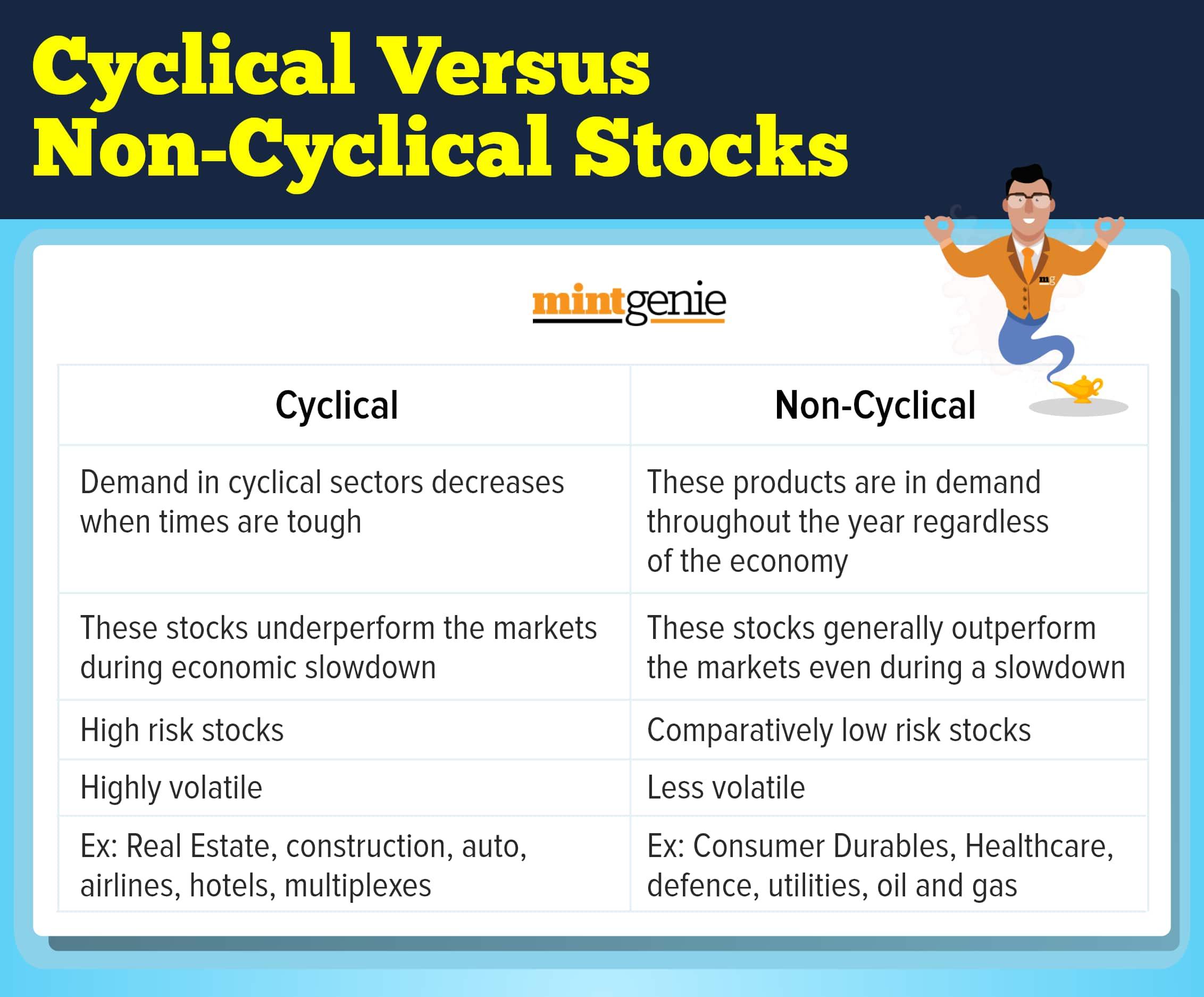

Cyclical vs non-cyclical

First Published: 02 Jun 2023, 05:02 PM IST

Topics to follow

Related Stories

Explain Like I am 5

markets

Growth vs Value investing: Which is the better approach to follow?

Prabhat Ranjan,Vijay Chauhan