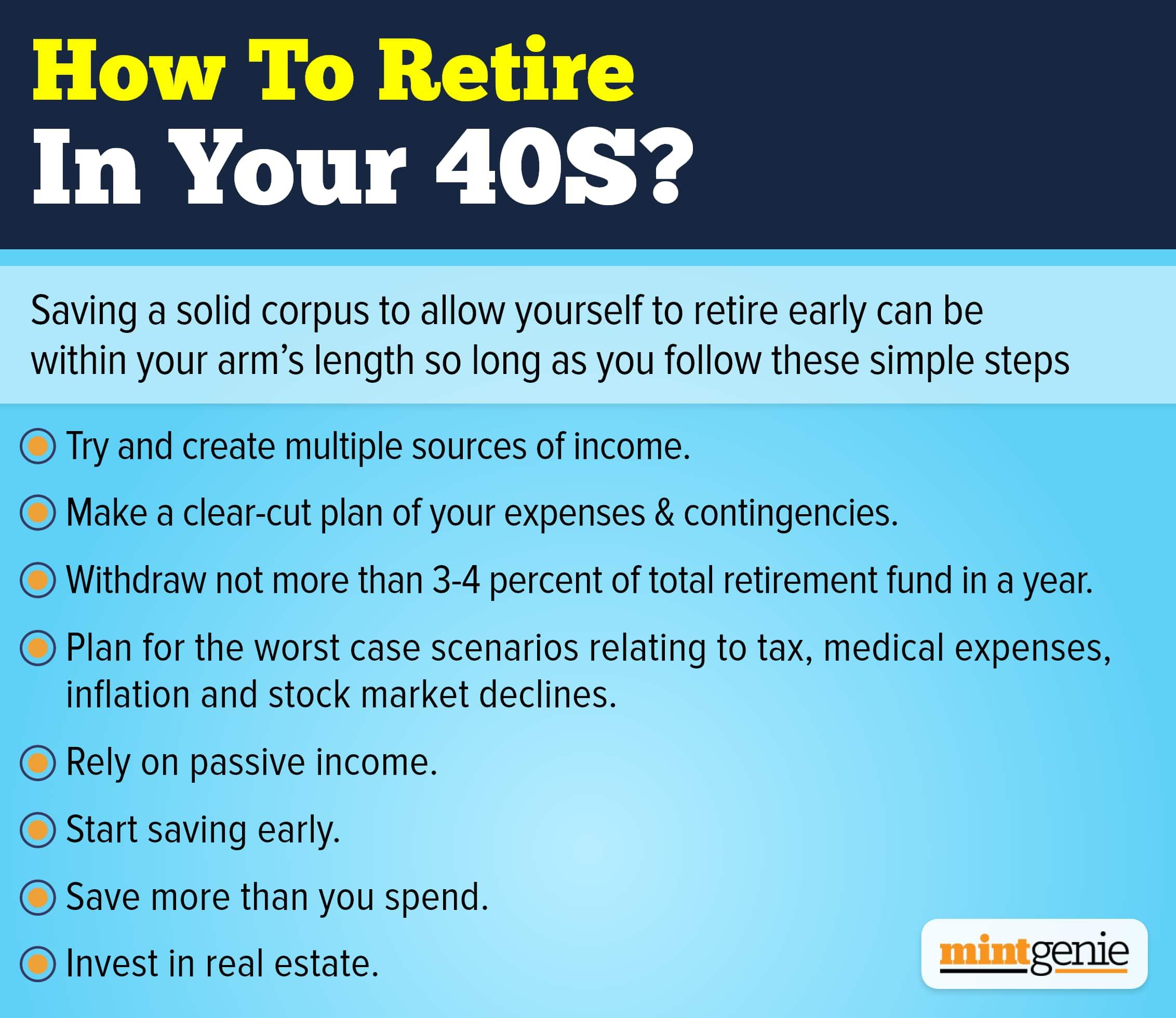

Except for the fortunate few who have enough wealth, no one is unconcerned about what happens when you stop earning. The fear of the unknown is always present.

We've all known elderly people who struggle to meet all of their financial obligations. When one does not have enough money, life becomes difficult.

Relying on traditional deposits for interest income

Many retirees go through a cycle of overspending and underspending. When a salaried individual retires, he or she receives this sum of money, which could range between ₹50 and ₹60 lakh. It appears to be a sizable sum. It's almost certainly more than the retiree has ever received in one lump sum in his or her life. They believe they have unlimited spending power. Many investors assume ₹50 lakh to be a large sum and, therefore, withdraw an equal amount every month without realizing that the money would sustain them for a limited period. An alternate way would be to set aside ₹15 lakhs and put the remaining ₹35 lakhs in a fixed deposit for five years. This way, they can pay themselves ₹25000 every month for five years at the end of which they would have a bit more than ₹48 lakh. They can then again set aside ₹15 lakh to earn a monthly pension income of ₹25,000 while keeping the remaining ₹33 lakh in a fixed deposit. This way, the cycle continues though it is marred by the disadvantage of having only ₹25000 every month to pay for the expenses, thus, not accounting for the continued devaluation of money.

Some may put their money in Senior Citizen Savings Scheme (SCSS) to earn quarterly interest at eight percent per annum. However, considering the effect of inflation on the prices of everyday living, would these investment methods suffice to pay for a retired lifespan extending 30 years or more?

The aforementioned assumptions are just hypotheses drawn to draw one’s attention to inadequate retirement planning. To start with, a retirement corpus up to ₹60 lakh is just not enough to sustain the remaining years of one’s life, especially, when there is no income and increased susceptibility to hospitalization and medical treatment. The tendency to stick to traditional investment options post retirement lies in the firmly grounded belief that the retirement corpus should be invested in 100 percent safe options. That “safety net” is all that most seek and it is this mindset that has caused many retired people to rely on their relatives for money or for necessary finances during emergencies.

Deciding monthly withdrawals

Apart, the concept of “safety net” is a misnomer and can be labelled as nothing short of “delusion”. Realizing how inflation can hit our savings and take a toll on our earnings in the long run, it makes sense to not only choose the right investment options after retirement but also decide on the amount of corpus that one must withdraw without losing the entire amount to expenses and inflation. At the current inflation rate, one would need four times more money to pay for our daily living expenses, thus, necessitating the need to not only churn the accumulated corpus to earn more money but also enable greater withdrawals during the golden years of one’s life. Evaluating how much you would need can be taxing as evaluating how much you should withdraw every month to live comfortably throughout.

How much money should you withdraw every month?

It is not rocket science to decide how much to save, invest and withdraw to avoid draining your retirement corpus. Common sense determines how we must decide our withdrawals based on interest rate income on our savings and the corresponding inflation rate. Only withdraw what your savings earn above and beyond the inflation rate to support an inflation-adjusted withdrawal rate. Think about it carefully. You only need to withdraw not more than one percent of the corpus every year if your savings earn eight percent and inflation is seven percent. This will ensure that your savings grow at least in line with inflation, preventing you from losing all your money in old age.

Eight percent returns from debt funds or other investment opportunities may not be enough, thus, highlighting the need to put some money in equities too. However, equity investments must be continued for at least five to seven years to meet medium-term financial goals and more than a decade or so to accomplish long-term financial goals.

Personal finance is not just about numbers alone. It has more to do with the psychology of money.