A couple gets married with the hope of a joyful future together and the dream of living ‘happily ever after.’

At times though, for one reason or another, things do not work out in a relationship and a married couple decides that it is in their best interest to opt for a divorce. It is never an easy decision, and divorce is often a messy situation with both partners dealing with emotional upheaval while going through the divorce proceedings.

Amidst the many tasks that come with a divorce, life insurance is often overlooked. However, this could lead to messy and uncomfortable situations in the future at the time of one partner’s demise or upon maturity of the policy. Hence, it is important that both partners look into their life insurance policies and make the necessary decisions at the time of the divorce.

Inclusion in the list of assets

The first step is to include all life insurance policies owned by the couple in the list of assets. Just like a property, fixed deposits, mutual funds and other financial investments, life insurance is also a financial asset and the couple needs to decide what to do with their existing policies.

Update nominees

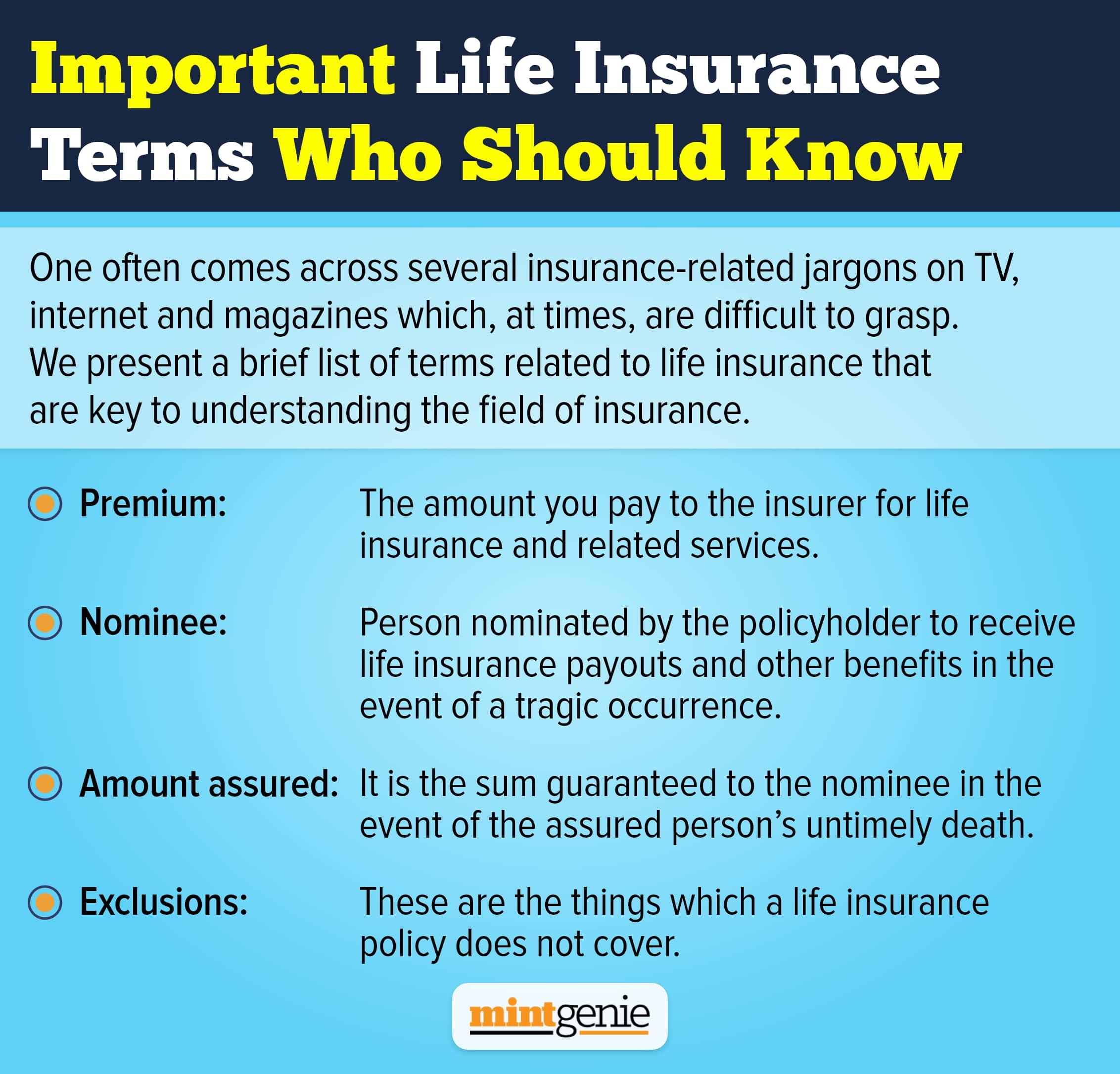

An individual purchases life insurance to financially secure his family in the event of his untimely demise. Hence, most married couples usually name their spouses as the primary nominee on their life insurance policy.

In the case of a divorce, the partners are unlikely to want their ex-spouse to benefit from their death. It is thus advisable to update the nominee of one’s life insurance policy to another person who would have an ‘insurable interest’ such as one’s parents or children. If not updated, the ex-spouse will continue to benefit from the life insured’s untimely demise.

If minor children are kept as nominees, then the parent needs to designate an ‘appointee’ who will act as a caretaker of the children’s interests till they attain a majority.

Married women’s property act (MWPA), 1874

The MWPA protects the rights of married women and entitles them to the benefits of their spouse’s life insurance policy. If a life insurance policy is purchased by a married man under the MWPA, and the wife is named as the nominee, then the benefits of the policy will continue to go to the wife even in the case of a divorce.

Division of policies

Term policies are generally considered as separate assets, and hence can be split between the spouses at the time of the divorce.

If a husband has assigned a policy to his wife but is continuing to pay the premiums, then he can request for the policy to be reassigned to him during the divorce.

For policies with a cash value, the couple will need to speak to their legal advisors and the life insurance company to understand what needs to be done on a case-by-case basis. If one partner is required to pay alimony and/or child support, then they can opt to continue with the policy for the purpose of alimony and child support payments.

In case there is no such requirement, then the couple can decide to surrender and exit the policy. The cash value of the policy can then be divided between the separating couple as per mutual agreement.

When it comes to joint-life policies, their purpose ceases to exist in the event of a couple divorcing. It is thus likely that the couple will have to let their policy lapse. It is advisable for the couple to seek legal advice to understand what exactly to do in such a case.

If the couple has bought a property together for which they are still paying the home loan, then it is likely that they would have an MRTA (Mortgage Reducing Term Assurance) policy, which is a life insurance product specifically designed to cover home loans. If the couple were co-borrowers of the loan, then the MRTA would be a joint-life policy covering both spouses. At the time of the divorce, the partner who is getting the property would continue to service the loan.

However, as the policy is joint, in the unfortunate event of the other partner’s demise, the sum assured would still go to the bank towards settling the loan. To avoid such a case, the partners may want to check with both the life insurance company and the bank if there is an exit clause.

Conclusion

While divorce is a difficult time for both the spouses, it is important to keep a clear and cool head when dividing the financial assets. Consulting legal and financial advisors as well as the life insurance company for complete information and sound advice during the divorce proceedings will help to financially protect and secure the individuals and their dependents in the future.

Karthik Raman, Chief Marketing Officer and Head - Products, Ageas Federal Life Insurance