Indian markets declined around half a percent on Thursday even after the Reserve Bank of India (RBI) kept the repo rate unchanged as expected. In a surprise move, RBI Governor Shaktikanta Das, in his policy speech, announced that an incremental Cash Reserve Ratio (CRR) of 10 percent on banks has been put in place effective August 12, 2023.

RBI Policy: How will the CRR measure impact markets? Here's what experts say

TL;DR.

How will the CRR and increase in inflation forecasts impact the markets? Is this a good time to buy? Here's what experts say

This led to a massive correction in banking and finance stocks in intra-day deals today. The Nifty Bank, as well as the Nifty Financial Services index, shed around 0.7 percent each. All, except one (IndusInd Bank), constituents of the Nifty Bank index were in the red after the CRR announcement. AU Bank, Bandhan Bank, Kotak Bank and Axis Bank were the top losers. Meanwhile, in the Nifty Financial Services index, only 4 stocks were in the green, while the remaining 21 gave negative returns.

"The policy is not that hawkish but a couple of factors contributed to the market's decline. Firstly, the decision to maintain an additional 10 percent of the Incremental Cash Reserve Ratio (CRR) for the banks. Additionally, a shift in the inflation forecast from 5.1 percent to 5.4 percent could also be influencing the market sentiment negatively," said Shrey Jain, Founder and CEO, SAS Online.

What is the CRR measure?

The Governor informed that Indian banks have been asked to maintain a 10 percent incremental cash reserve ratio (ICRR) with effect from August 12, due to an increase in their Net Demand and Time Liabilities (NDTL) between May 19 and July 28, 2023.

The measure is intended to absorb the surplus liquidity that has been generated to manage the liquidity overhang, including a greater-than-anticipated quantum of ₹2,000 notes in the banking system.

On May 19, the RBI announced the withdrawal of the ₹2,000 note, allowing citizens to either exchange the note or deposit it in their accounts. The central bank on August 1 said that ₹3.14 lakh crore worth of ₹2,000 banknotes, or 88 percent in circulation, had returned to the banking system by July 31.

Das also clarified that despite the move, there shall remain adequate liquidity in the banking system, and since the move is temporary in nature, the decision will be taken up for a review either on September 8 or earlier. Internal calculations show that the incremental CRR for scheduled banks will affect liquidity by a little above ₹1 lakh crore, the Guv added.

"The incremental CRR was considered necessary in the background of the liquidity overhang. We considered it desirable in the interest of financial and price stability. It will have an impact on inflation also. It is a purely temporary measure," Das said.

However, the Cash Reserve Ratio has been left unchanged at 4.5 percent.

Policy and Inflation

The RBI MPC has left the repo rate unchanged at 6.5 percent, for the third time in a row, while also retaining the ‘Withdrawal of Accommodation’ stance for tackling inflation. The MPC voted unanimously to keep the repo rate unchanged.

This decision is in line with Street expectations, however, the RBI raised the inflation forecast for FY24 to 5.4 percent from 5.1 percent in the June policy. But the GDP growth forecast for FY24 was retained at 6.5 percent.

How will the CRR and increase in inflation forecasts impact the markets? Is this a good time to buy? Will CRR impact be good or bad for banks and financials? Here's what experts say:

Apurva Sheth, Head of Market Perspectives & Research, SAMCO Securities

RBI kept the interest rate unchanged but threw in a twist by asking banks to maintain an incremental cash reserve ratio (I-CRR) of 10 percent. This measure will suck in about ₹95,000 crore from the banking system. Banks were flush with liquidity after the withdrawal of ₹2,000 notes. They had received ₹3.14 lakh crore till 31st July as a result, which is, almost 88 percent of the total ₹2,000 notes in circulation. Banking stocks reacted negatively as they will not earn any interest on the funds kept under ICRR.

Another major reason for the markets to react negatively was that the inflation forecast for FY23-24 increased from 5.1 percent to 5.4 percent. The increased inflationary expectations have led to a hardening of bond yields and pushed ahead the chances of a rate cut any time soon.

We believe that a dip in the market is much needed. The RBI move may pave the way for a healthy correction. If Bank Nifty fails to hold above the 44,500 mark then there is a chance of a fall till 43,500. This is a major support level for Bank Nifty where investors can get it to good quality banking stocks.

Santosh Meena, Head of Research at Swastika Investmart Ltd.

The RBI governor's decision to maintain unchanged policy rates, as widely anticipated, was overshadowed by a notable upward revision in the inflation forecast. Additionally, the implementation of a 10 percent incremental Cash Reserve Ratio (CRR) for banks added to the market's unease.

The short-term market structure seems to lean towards a sell-on-rise pattern. This is partly due to the global market's nervousness, exacerbated by the jump in crude oil and other commodity prices, posing notable challenges for the Indian market. Looking ahead, the focal point of market attention is expected to shift toward the impending US inflation figures scheduled for release this evening. There's a discernible risk that the Nifty index might experience a decline toward levels around 19,191 and 18,888 unless it manages to surpass the 20-Day Moving Average (20-DMA) threshold of 19,650.

Divam Sharma, Founder & Fund Manager at Green Portfolio PMS

We have seen a dream run over the last 5 months post RBI holding rate hikes. We are seeing a continuity of the stance of withdrawal of accommodation, focus on growth and being vigilant of global macro developments.

However, recent developments around markets factoring in the positives on RBI holding rate hikes, recent developments around enhanced macro uncertainties, rise in food inflation and crude price and uncertainties around growth across developed and emerging nations can create short-term volatility in the markets.

India is comparatively isolated from the rest of the world in terms of economic factors and the long-term prospects look promising while such headwinds can impact the markets over the short term. Stagger your allocation for the next 2-3 months and don’t go aggressive on the markets at the moment.

Anil Rego, Founder & Fund Manager at Right Horizons

The RBI has decided to pause its rate hike cycle for the third time in a row. The rates at 6.5 percent are comfortable and one more hike is expected during the year without a material impact on growth and the expectation of a rate cut in 2024 remains a positive sign.

Markets have touched new highs, especially with earnings for the first quarter coming healthy supporting the trajectory. Investors are bullish as they are favouring rate cuts in 2024 which will unanimously boost the equity markets. The banking sector is the most sensitive to changes in rate cycles and has been a major reason for incremental earnings in FY23 benefitting from the hikes and credit growth being robust and persistent. Prolonged rate cuts will eventually lead to narrowing NIM but we expect rate cuts to begin in the last quarter and hence the trend in the banking sector is likely to continue in FY24. NBFCs will be best positioned to benefit from cuts in rates as credit growth will improve followed by banks. Also, credit-sensitive sectors like auto and real estate will see higher demand.

Sonam Srivastava, Founder & Fund Manager at Wright Research

Today's announcements by the RBI Governor, Shaktikanta Das, affirm the resilient nature of the Indian economy amidst global challenges. The decision to introduce an incremental CRR of 10 percent is a prudent move to manage the surplus liquidity in the banking system, highlighting RBI's commitment to ensuring stability. While the unchanged GDP growth forecast paints a confident picture for the economy, the raised CPI inflation forecasts for the coming quarters signify headwinds and the need for watchfulness.

The market has a weak reaction to today's MPC meeting. The banking sector, in particular, might face short-term pressures due to the incremental CRR announcement, as it implies temporary constraints on deployable funds. However, the assurance of adequate liquidity should allay significant concerns. With inflation forecasts being revised upwards, sectors like FMCG and agri-businesses might witness volatility based on the implications for consumer demand and pricing. The unchanged repo rate and other key rates, combined with clear communication from the RBI about their stance, will likely provide some stability. However, sectors linked closely to consumer spending might be on watch due to concerns about inflationary pressures impacting demand. Investors would be wise to remain vigilant and diversify their portfolios, focusing on sectors and companies with strong fundamentals and resilience to inflationary pressures.

Sujan Hajra, Chief Economist & Executive Director, Anand Rathi Shares and Stock Brokers

The CRR hike would temporarily drain out liquidity close to ₹70,000 crore. The systemic liquidity would still be in surplus. Consequently, the impact would be largely neutral for banks. This in fact would be positive for NBFCs as the short-term interest rate would be lower than what was anticipated earlier.

Akshay Tiwari - Fundamental Analyst, Religare Broking Ltd

The incremental CRR (I-CRR) is intended to absorb the excess liquidity arising from deposits of ₹2,000 notes in the system. In the banking system, the I-CRR may lead to setting aside additional reserves of ~ ₹1 lakh crore. This is a temporary measure and the RBI shall assess the demand/supply of liquidity on September 8th, 2023. This measure is not expected to have much impact on the banks profitability in the long run nor do we foresee any incremental pressure on NIMs of banks due to this move. The estimated incremental reserve stands at around 1% of the bank's total credit outstanding.

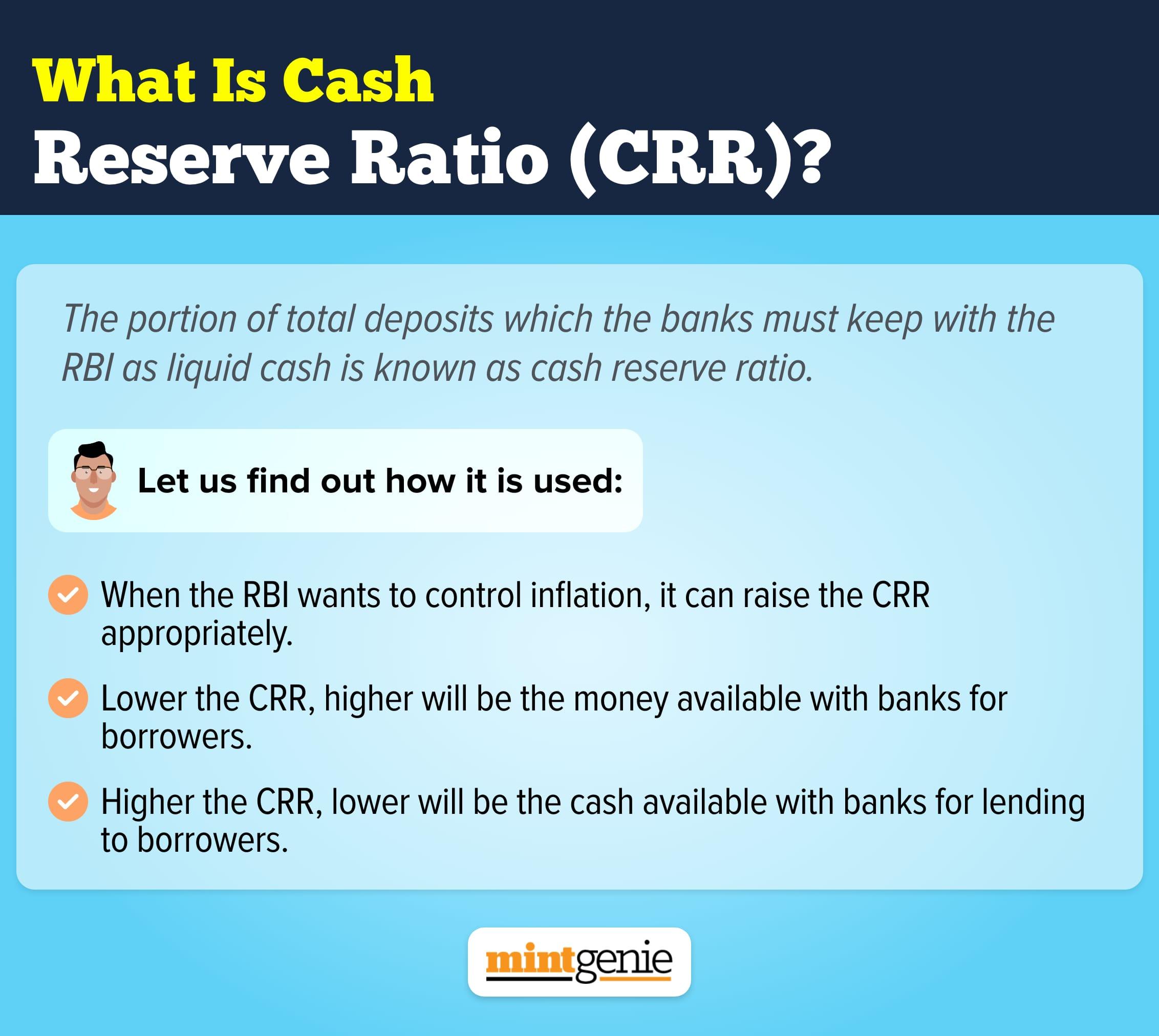

The portion of total deposits which the banks must keep with the RBI as liquid cash is known as cash reserve ratio.

First Published: 10 Aug 2023, 03:52 PM IST