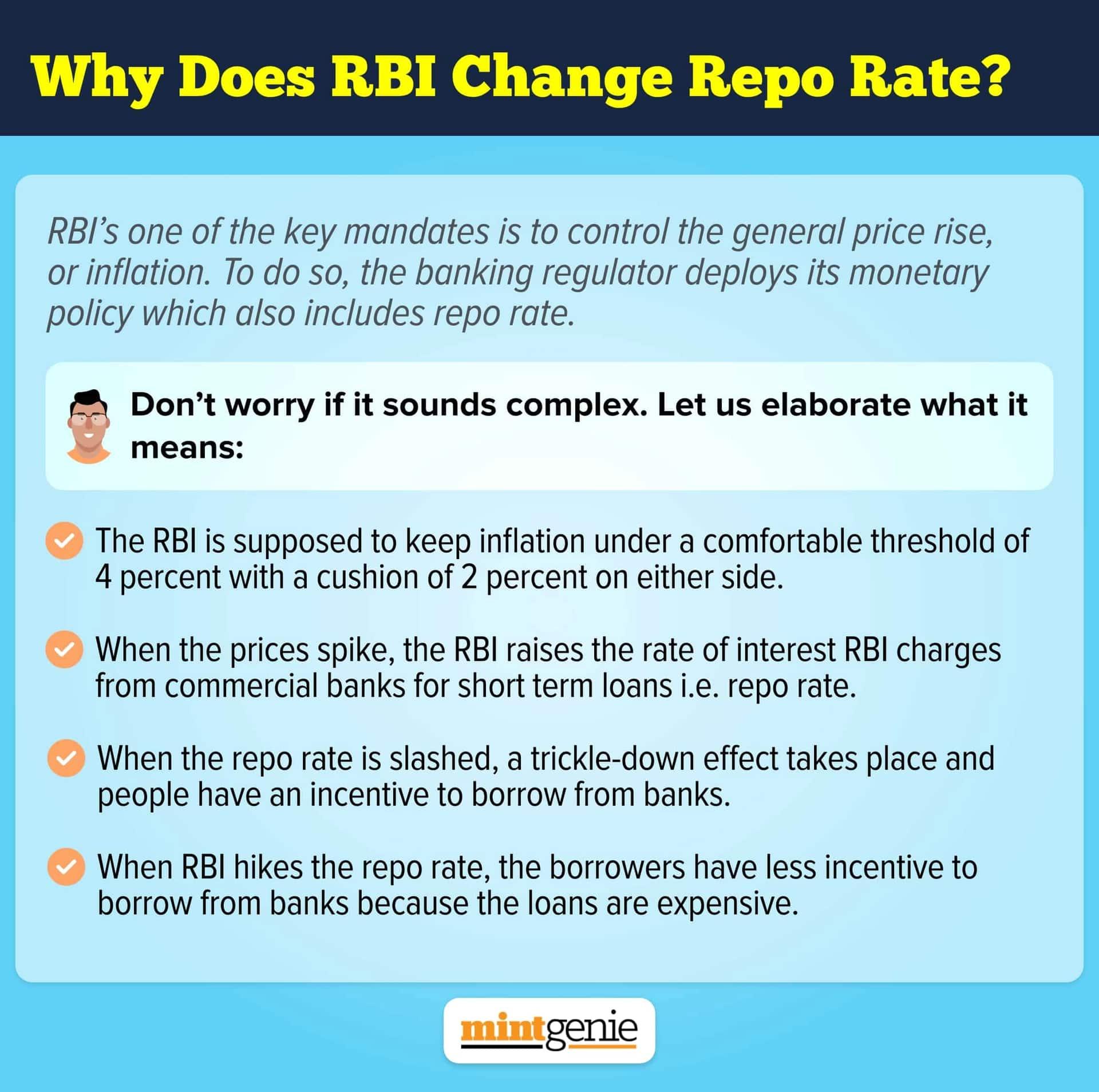

In April 2022, the Reserve Bank of India (RBI) launched the standing deposit facility (SDF) as a mechanism to curb inflation by absorbing liquidity.

The "Expert Committee to Revise and Strengthen the Monetary Policy Framework" advocated the SDF as a liquidity management tool in January 2014. However, Section 17 of the RBI Act of 1934 was modified in 2018 to allow the RBI to introduce this instrument, which was now brought into action in 2022.

The central bank's decision to deploy SDF raises a significant dilemma, though, as the reverse repo rate can also be used to absorb liquidity.

Let us start this discussion by explaining what is a SDF.

What is standing deposit facility?

The standing deposit facility is a collateral-free liquidity absorption mechanism implemented by the RBI with the intention of transferring liquidity out of the commercial banking sector and into the RBI. It enables the RBI to take liquidity (deposits) from commercial banks without having to compensate them with government securities.

The SDF is significant because it was created to give the Reserve Bank the ability to handle unusual circumstances when it must absorb large quantities of liquidity. In the past, the RBI has experienced issues with liquidity absorption due to events like the global financial crisis and demonetization.

The SDF allows banks to deposit money with the RBI on an overnight basis. But the RBI has the option, should the need arise, to absorb liquidity for longer tenors under the SDF with proper pricing. The SDF scheme would be open to all participants in the liquidity adjustment facility (LAF).

How does SDF absorbs liquidity?

SDF provides flexibility for managing excess liquidity since it frees the RBI from the requirement to disclose government securities on the balance sheet. How? Every SDF will have two entries on the balance sheet: one under net claims on banks and one under currency-in-circulation on the liability side. This negated effect on the balance sheet of the RBI offers it greater chance to absorb more liquidity.

At this point, overnight deposits will be subject to the SDF rate, which will be 25 basis points below the policy rate (Repo rate). However, it would continue to have the ability, with the proper pricing, to absorb longer-term liquidity if and when the need arose. The goal of the RBI is to bring the system's liquidity surplus down to a magnitude that is compatible with the current stance of monetary policy.

Coming back to question we raised in the beginning, what was the need to launch a new instrument when we already had reverse repo facility to absorb liquidity?

How is SDF different from reverse repo facility?

The central bank employs reverse repo rate and SDF to remove excess liquidity from the system. In contrast to SDF, reverse repo operations require the RBI to deposit collateral in the form of government assets in order to borrow money from commercial banks.

Under the current liquidity system, the Reserve Bank has discretion over liquidity absorption through reverse repos, open market operations, and the cash reserve ratio. SDF, on the other hand, will allow banks to store surplus liquidity with the Reserve Bank at their discretion.

As a result, the fixed-rate overnight reverse repo is no longer the LAF corridor's floor. The reverse repo, however, remains to be a weapon in the RBI's toolbox for monetary policy, and its use will be at the RBI's discretion for periodically announced objectives.

Since excess liquidity in the market is a key factor in deciding policy rates, the RBI established this instrument to absorb it. You must be aware that the rates on your savings and loans will vary as a result of the change in policy rates. One must thus pay close attention to the SDF rate in addition to the other rates.